Authors: Barry Simon Graham (Group Co-CIO) and Michael Yaw Appiah (Group Co-CIO)

Introduction

Rarely has the global economic landscape shifted so dramatically within a single quarter as it has in 2025. The interplay of dynamic factors – geopolitical risks, an escalating trade war marked by tariffs, and extreme market volatility – validates and bolsters the tenets of our Investment Outlook 2025.

These powerful forces serve to substantiate and deepen the relevance of our “New Economics Era” framework. This updated perspective for private markets is structured into two sections: Part A examines the evolving implications of trade tariffs and ESG strategies, followed by Part B, which details our recalibrated investment convictions for both near-term tactical opportunities and long-term strategic allocations..

Part A: Some Q&As

##1: Current U.S. Administration Blanket Tariffs: A Bold Gamble or a Risky Overreach?

How do we interpret Trump administration recent decision to impose blanket tariffs on all countries—including allies, rivals, and adversaries? What are the broader implications?

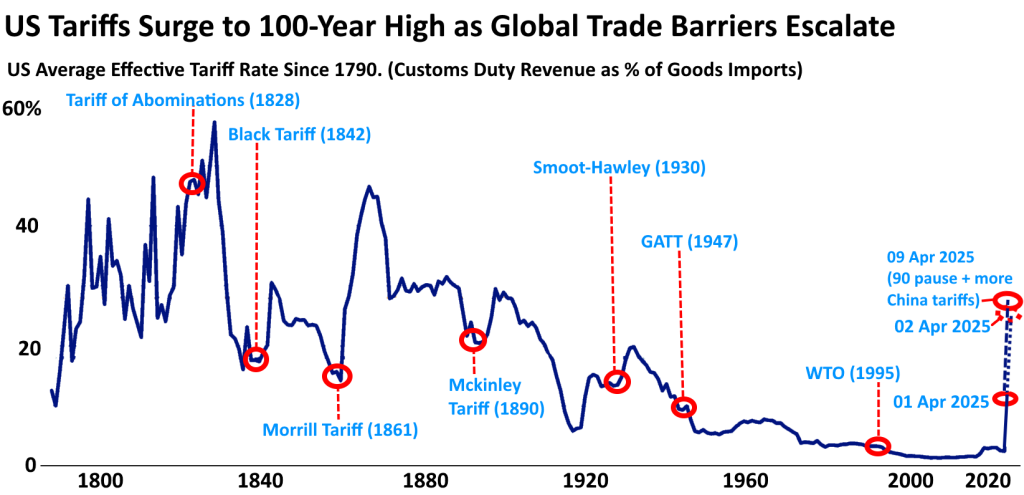

We believe this could go down as one of the biggest self-inflicted wounds in U.S. economic history. Trump’s April 2, 2025, decision to impose sweeping tariffs may damage not only American consumers and businesses but also shake the very global trade system the U.S. once championed, helped build and from which it has long benefited.

In recent weeks, U.S. importers faced a new era of protectionism (albeit with some exceptions and 90-day reprieve pending negotiations): a universal 10% tariff on all goods entering the country, complemented by aggressive, country-specific duties aimed at major trade deficit partners. These actions, building on prior tariffs affecting China, Mexico, Canada, and the auto sector, will propel America’s average tariff rate to levels unseen since the early 20th century or in over 100 years.

Trump’s argument rests on a flawed premise—that trade deficits are economic failures, akin to business losses—when in reality, they reflect intricate global supply networks. His nostalgic fixation on factory jobs ignores the transformative impact of free trade, which has empowered the U.S. to evolve into a high-value economy built on technology, services, and cutting-edge innovation.

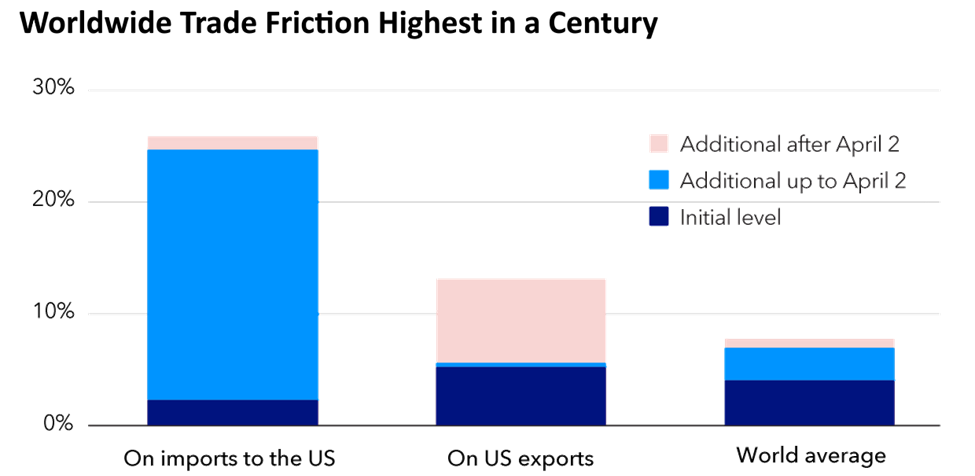

Exhibit 1: Century-High Global Trade Friction Presents Evolving Risk-Reward Landscape For Institutional Allocations

The proposed “reciprocal” tariffs are crude, back-of-the-napkin formula: take the U.S. trade deficit with a given country, convert it into a percentage of imports, and divide by two. It ignores the real dynamics of trade barriers and dismisses the complex architecture of global commerce. More than that, it recklessly disregards U.S. commitments under existing trade agreements and offers no credible path to boosting U.S. competitiveness or investment appeal.

The immediate impact of Trump’s tariff measures on the U.S. economy is likely to be higher inflation and weaker growth. Our analysts project that annual inflation could climb above 4% by the end of the year, intensifying pressure on American households already strained by a 20% increase in prices since the onset of COVID-19. As a result, the prospect of interest rates remaining higher for longer becomes more likely.

Exhibit 2: Heightened Global Trade Barriers: A Generational Shift Reshaping Investment Strategies Of Asset Managers & Alternatives

In addition, we think the alarm bells are ringing for American businesses. Forced to rethink their supply chains and invest in costlier domestic sourcing, they also face a volatile trade climate marked by erratic policymaking and looming retaliatory tariffs. Investor confidence is slipping fast— recent market plunge in both the S&P 500 and the dollar is a clear sign that the belief in U.S. economic dominance or exceptionalism is wearing thin.

The imposition of tariffs by the Trump administration is expected to have profound economic repercussions for export-reliant nations, especially those in Southeast Asia. The hard-won gains in poverty alleviation across the region could be reversed. Meanwhile, the broader global outlook remains dim, with slow growth persisting in key economies including the European Union, Japan, and China.

Retaliation is a natural reflex in the face of protectionism, but this juncture demands prudence over provocation. The administration has made it clear it intends to respond in kind, yet measured decision-making should guide the global response. Excluded trade partners would be better served accelerating intra-regional free and multilateral trade frameworks. After all, the United States comprises merely 13% of global goods imports, and belief in the principles of comparative advantage endures across much of the international community—despite the current U.S. administration’s stance.

There was nothing liberating about this moment for America. Should Trump prevail, the U.S. will turn inward—cutting itself off from the very global system that fueled its rise. The fallout will be global, but the rest of the world can choose a different path.

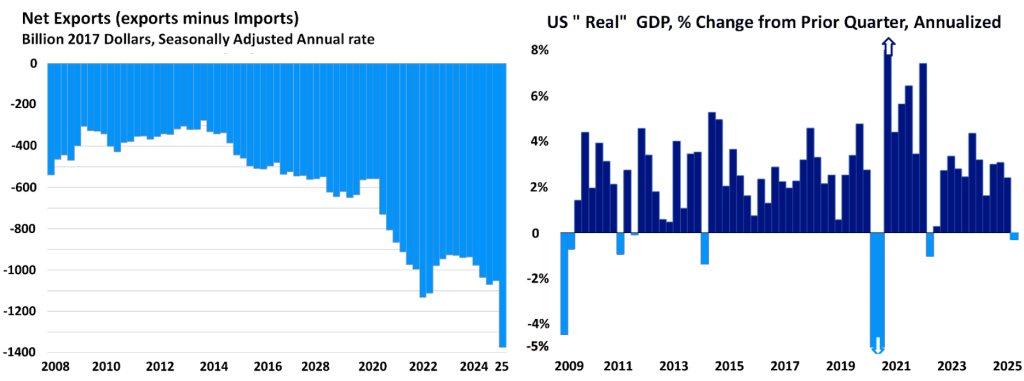

In the immediate term, America’s GDP will take a hit, dragged down by a temporary surge in imports as businesses raced to front-load shipments ahead of new tariffs.

Exhibit 3a: US GDP Shrank By 0.3% As Two Forces Converged – A Historic Surge In Imports (Firms Front-Loading Ahead of Tariffs)

As amplified by Q1 2025 BEA data, America’s GDP shrank by 0.3% as two forces converged: a historic surge in imports (companies front-loading ahead of tariffs) slashed 5.0 percentage points from real GDP, and government spending cuts subtracted another 0.25 points. This contraction occurred even as consumer spending grew 1.8% and private domestic investment skyrocketed 21.9%, including a 22.5% jump in equipment purchases as businesses expanded U.S. production to avoid tariffs.

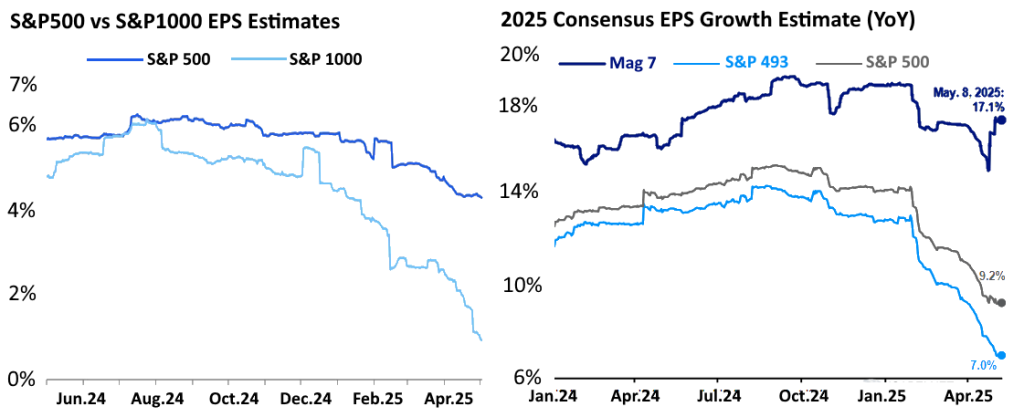

Exhibit 3b: Even Without The Added Pressure Of Tariffs, The Foundation Of U.S. Corporate Profitability Is Eroding

Even without the pressure of new tariffs, one might assume corporate America is on steady ground. There’s a quiet earnings erosion underway in corporate America—and it’s not where the headlines are looking. Beneath the surface of a rising stock market, profits at small- and mid-sized companies are rapidly deteriorating, validating the core themes in our Investment Outlook 2025. First-quarter earnings reports have shattered earlier optimism for these firms. The S&P 1000 index, which spans companies worth between $1 billion and $20 billion, has seen its expected 2025 earnings growth fall sharply—from 5% at the year’s start to just 1% today.

While large-cap margins appear to be holding up, this stability is an illusion propped up by just a few tech titans. The “Magnificent 7” (Alphabet, Apple, Meta, Microsoft, Nvidia, Tesla, and Amazon); continue to buoy the S&P 500, masking broader weakness across the remaining 493 names—whose margin trends are closely mirroring the slump seen in smaller caps. The result is a market with narrow leadership and deteriorating breadth—a setup that calls for caution, selectivity, and tactical positioning.

##2: The Tariff Trap: Why Protectionism Fails to Revive Outsourced Manufacturing Jobs in Developed Economies

Tariffs are often promoted as a tool to protect domestic industries and revive manufacturing jobs in developed economies such as the U.S., Europe and so forth. However, the reality is more complex. While tariffs may offer short-term protection for certain industries, they fail to generate sustainable job growth in wealthy nations. This pattern reflects what we call the “Tariff Trap” — a set of economic realities that undermine the very goals tariffs claim to achieve.

First, tariffs tend to backfire by raising production costs and shrinking demand. Picture a scenario where tariffs succeed in making foreign imports prohibitively expensive, forcing reliance on domestic production. In theory, this sounds like a victory. But in practice, it leads to unaffordable goods for consumers. Higher prices erode purchasing power at home while retaliatory tariffs abroad shrink export markets. For example, when the U.S. imposed tariffs on Chinese goods between 2018–2019, American manufacturers faced rising input costs. Iconic companies like Harley-Davidson responded by relocating production overseas to avoid the inflated price of steel, illustrating that tariffs can push jobs offshore rather than protect them.

Second, tariffs cannot reverse the tide of automation and technological disruption. Even if tariffs successfully limit foreign competition, they do nothing to prevent automation from replacing human labor. In fact, reshored factories in developed economies often embrace robotics and AI to remain competitive—leading to higher output but fewer jobs. The U.S. steel industry is a case in point. After tariffs were imposed on steel and aluminum in 2018, companies like U.S. Steel and Nucor expanded capacity but invested heavily in automation, undermining hopes of large-scale job creation.

Third, retaliation from trade partners damages export-driven industries. When wealthy nations impose tariffs, they invite countermeasures that hurt domestic exporters. Jobs tied to exports—whether in aerospace, agriculture, or high-tech sectors—face declining demand abroad. In many cases, these job losses outstrip the employment gains in protected industries, leaving the broader economy worse off.

Finally, rather than bringing jobs home, tariffs often incentivize companies to offshore production to third-party countries outside the tariff regime. Instead of reshoring, businesses adjust their supply chains to bypass tariff barriers, shifting jobs to nations unaffected by the trade dispute. The net result is not a revival of domestic employment but a geographic redistribution of global manufacturing.

In summary, while tariffs offer symbolic appeal as a defense of domestic industry, they fall short as a sustainable strategy for job creation in advanced economies.

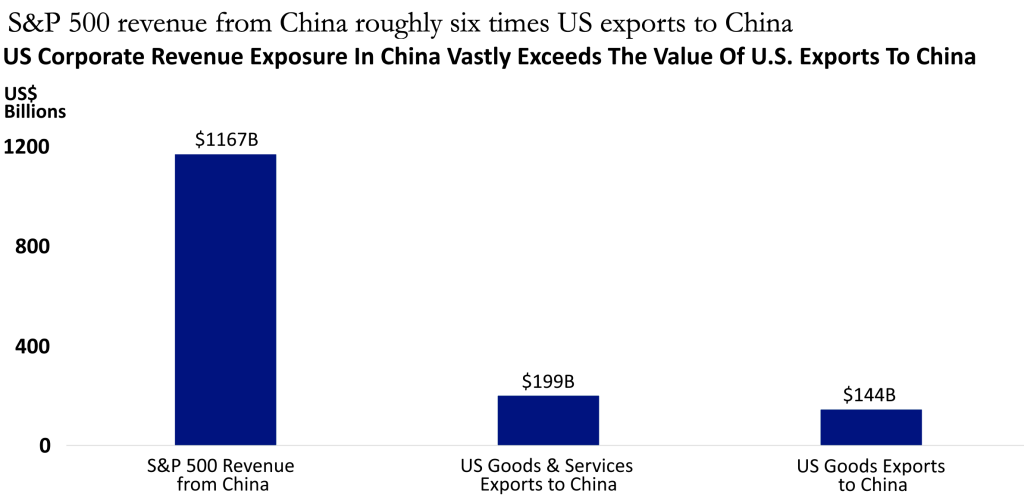

Recent data underscores a critical yet often overlooked dynamic in U.S.-China economic relations: the economic stake of U.S. corporations operating within China far exceeds the traditional export relationship. In fact, S&P 500 companies generate an estimated $1.2 trillion in annual revenue from their operations in China—a figure that dwarfs the total value of U.S. exports to China, which stands at only $199 billion for goods and services combined, and $144 billion for goods alone. This disparity reveals a profound reality: America’s economic exposure to China is driven far more by the in-country activities of multinational corporations than by exports crossing borders.

This distinction has major implications for trade policy. While tariffs target U.S. exports or imports, the revenue streams most critical to U.S. corporate performance are embedded within the Chinese domestic market. The fact that 6.7% of S&P 500 revenues are derived from China points to a business model rooted in foreign direct investment, local operations, and on-the-ground sales to Chinese consumers—not simply exporting American-made goods into China. Consequently, policy measures that disrupt the bilateral relationship risk damaging the revenue base of major U.S. corporations far beyond the narrow channel of trade balances.

Exhibit 4: S&P 500 Revenues From The Chinese Market Are Much Greater Than Total U.S. Exports To China, Signaling Deeper Corporate Integration In The Chinese Economy

In short, blanket tariffs may be counterproductive, failing to account for the deeper integration of U.S. firms within China’s economy. The greater vulnerability lies not in restricted exports, but in potential curtailment of local operations, lost market access, and declining revenues within China itself. Any serious discussion of economic decoupling or trade conflict must grapple with this embedded corporate presence and its strategic importance to American business.

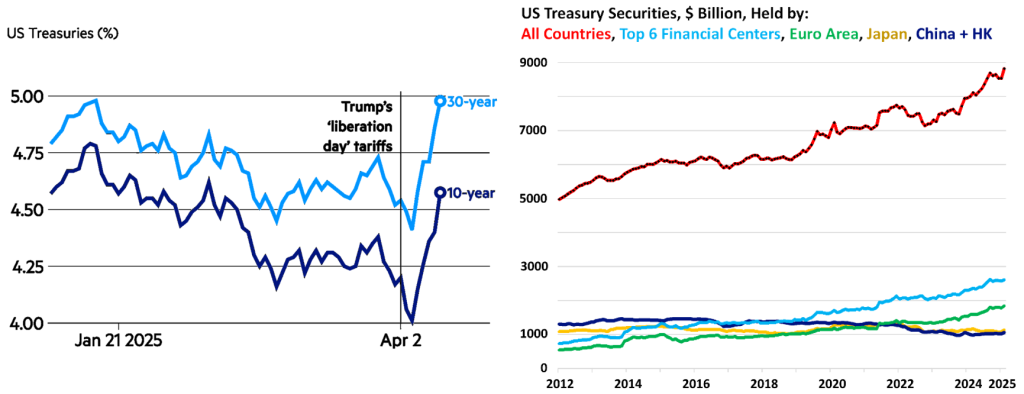

##3: Tariffs Implications – U.S. Dollar Exorbitant Privilege & US Treasuries

In light of the Trump-era tariff policies, how do we perceive the long-term geopolitical and economic implications for the U.S. dollar’s ‘exorbitant privilege’? What observable shifts in global financial dynamics are we witnessing and the future role of the dollar in the international monetary system?

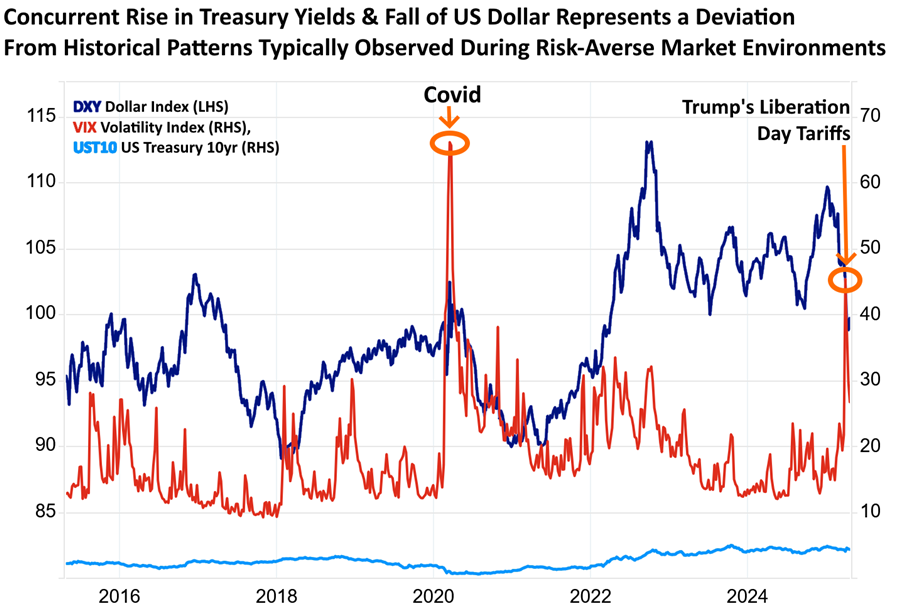

In the global financial theater, 2nd April 2025 – stood out as a day of unexpected dissonance; marked more than just a market jolt. Trump administration’s aggressive tariff announcement and strategy sent tremors through the markets—stocks sank, volatility surged, and Treasury yields climbed.

The 10% market drop over two consecutive days—April 3rd and 4th—has happened just four times since 1952, underscoring the rarity of this turmoil. Such chaos has traditionally steered global investors toward the U.S. dollar, the relative world’s go-to safe-haven currency. Yet beneath the surface; in a striking departure from the norm, something more ominous unfolded in the currency markets; the dollar fell. The fall wasn’t marginal—it was, by statistical measures or model forecasts, the most pronounced in 4 years. This unusual move hinted at something deeper: perhaps the start of a broader reassessment of the U.S.’s role in the global economic order. It suggests investors were not merely reacting to noise, but reevaluating the credibility of U.S. economic management and the long-held assumption that the dollar will always be a default refuge. It was a signal that confidence was faltering.

The DXY dollar index has recovered slightly, but there’s a growing, almost tangible unease about where the dollar is heading. Respected market analysts are sounding the alarm, warning of a potential “confidence crisis” in the dollar. The U.S. currency has long been propped up by massive foreign inflows over many decades — now, that money might be preparing to “leave”.

Exhibit 5: U.S. Financial Landscape Is Exhibiting A Rare Phenomenon: Rising Treasury Yields Coupled With A Declining Dollar

At the end of 2024, the Bureau of Economic Analysis (BEA) estimated the U.S. net international investment position at a deficit of $26.2 trillion, with total cross-border assets and liabilities reaching $88 trillion. This enormous imbalance means that any factor deterring foreign investment in U.S. assets—such as policy instability—could have a more profound impact on the dollar than changes in trade flows alone. Our Leading FX strategists now forecast a prolonged and deeper decline in the U.S. dollar. Their view is not driven merely by Trump’s aggressive tariff regime, which was already priced in, but by a broader reassessment of what his economic strategy means for America’s currency standing.

Unlike the prevailing view among many analysts who believe tariffs will boost the dollar, Zinqular sees a different outcome emerging. Our reasoning is twofold. First, the escalating trade tensions—many of which we view as avoidable—along with an array of policies that fuel uncertainty, are dampening both consumer and business sentiment. This weakening confidence is undermining any potential dollar -positive effects by dragging down expectations for future growth. Second, deteriorating trends in U.S. governance and institutional integrity are beginning to chip away at the “exorbitant privilege” that has long supported the strength of U.S. assets. As this foundation weakens, so too does the attractiveness of U.S. asset return and the dollar’s long-term prospects—unless a meaningful policy reversal is undertaken.

The third issue, which closely relates to the others, lies in how the tariffs are being implemented. Investors are finding it increasingly difficult to accurately price these trade measures. While exchange rates—especially the strength of the U.S. dollar—have traditionally acted as shock absorbers during tariff impositions, as seen in both the earlier U.S.-China trade war and the initial Canada/Mexico tariff phase in early 2025, the unpredictable shifts in implementation timelines and crude tariff modeling are heightening uncertainty. This uncertainty, in turn, is feeding into growing concerns about a potential recession. Unlike well-targeted tariffs that enable structured negotiations, the current broad and unilateral approach discourages flexibility from foreign producers. As a result, U.S. businesses and consumers are left bearing the cost burden, while the dollar must weaken further to restore equilibrium—especially if supply chains and consumption patterns can’t adjust quickly.

The aftershocks of US dollar (USD) weakness and surge in UST yields is reverberating in FX markets globally. For instance, the Taiwanese dollar (TWD) surged the most in nearly four decades. Its currently trading at 3% higher against the USD at 31.06 at time of this publication. Our analysis suggests the TWD’s sudden surge is caused by local life insurance firms belatedly scrambling to hedge their dollar exposures; triggering outsized demands for TWD. This is already causing some contagion in places like South Korea, where the Korean won (KRW) has also suddenly jumped. We believe most Korean insurers are using the KRW as a substitute hedge for dollar exposure, due to the rising costs of directly hedging in USD —intensifying the FX market’s volatility.

On a macro level; this signals a pivotal turning point amplifying our “New Economic Era” framework: the U.S. dollar’s era of unparalleled dominance, sustained over the past decades, may now be approaching a gradual decline—though this transition is likely to unfold over several decades. In this evolving scenario, the euro and Japanese yen stand to gain the most. Mid-term projections now place the EUR/USD exchange rate at 1.12, 1.15, and 1.20 over the next three quarters—up from previous estimates of 1.07, 1.05, and 1.02. This is an average increase of approx. 11%.

Likewise, USD/JPY is expected to fall to 138, 136, and 135, compared to prior projections of 150, 151, and 152. This is an average depreciation rate of 14.7% over the next three quarters. It’s a bold stance, but we’re willing to say it: the era of America’s “exorbitant privilege” might be fading. While this could still prove early, the real alarm will come if we witness sustained days of rising U.S. Treasury yields and a weakening dollar. That would signal a more decisive retreat of foreign capital from the $26 trillion net international investment position.

The picture is not encouraging. The concurrent spike in Treasury yields and depreciation of the U.S. dollar signals deeper unease. Typically, periods of rising market volatility—as reflected in the surging VIX—drive capital toward safe assets like Treasury bonds. But in this instance, a rush by highly leveraged hedge funds to raise cash has led to a broad Treasury sell-off, reversing the usual safe-haven behavior and pushing yields upward. This counterintuitive dynamic mirrors what we witnessed during the early COVID-19 market panic, where rising yields and volatility created a feedback loop of instability. Back then, the Fed’s decisive intervention was necessary to restore order—a scenario policymakers may need to prepare for again.

##4: Spotlight on U.S. Exceptionalism & U.S. Treasuries Dynamics

What are the potential consequences for the $26 trillion U.S. net international investment position if foreign investors begin offloading Treasuries in response to trade tensions?

The U.S. financial landscape is exhibiting a rare phenomenon: rising Treasury yields coupled with a declining dollar. Such conditions, typically associated with markets facing economic challenges, indicate a possible change in market sentiment.

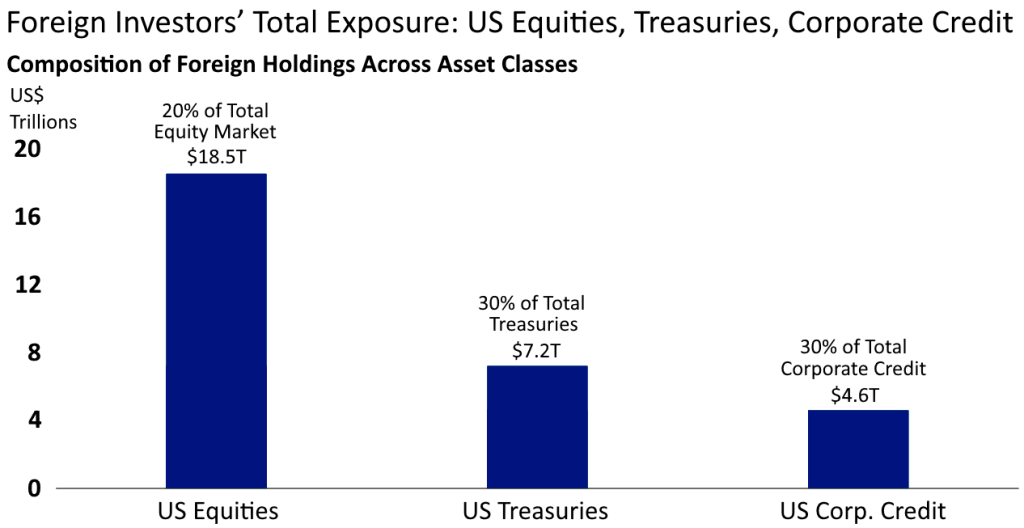

What began as a U.S. tariff dispute has morphed into something far more consequential—raising serious concerns among experts about whether the United States can continue to hold its dominant position in global finance. For decades, the U.S. has enjoyed massive and consistent inflows into its financial markets: bonds, equities, credit instruments, and the dollar itself have all reaped the benefits.

Exhibit 6: US Financial Markets Have Enjoyed Sustained, Large-Scale Capital Inflows — Spanning Bonds, Equities, Credit Instruments, & The USD — Reflecting Their Enduring Global Appeal

By early 2025, the U.S. still represented roughly 25% of global GDP and a striking 65% of total global equity market capitalization. But perhaps it was inevitable that some of this dominance would begin to wane. Meanwhile, the world is changing. China has made rapid advances in technology—beyond just Deepseek, companies like Huawei and BYD are breaking new ground—while Europe is finally embracing large-scale fiscal stimulus. For global investors heavily concentrated in U.S. assets, credible alternatives are starting to emerge.

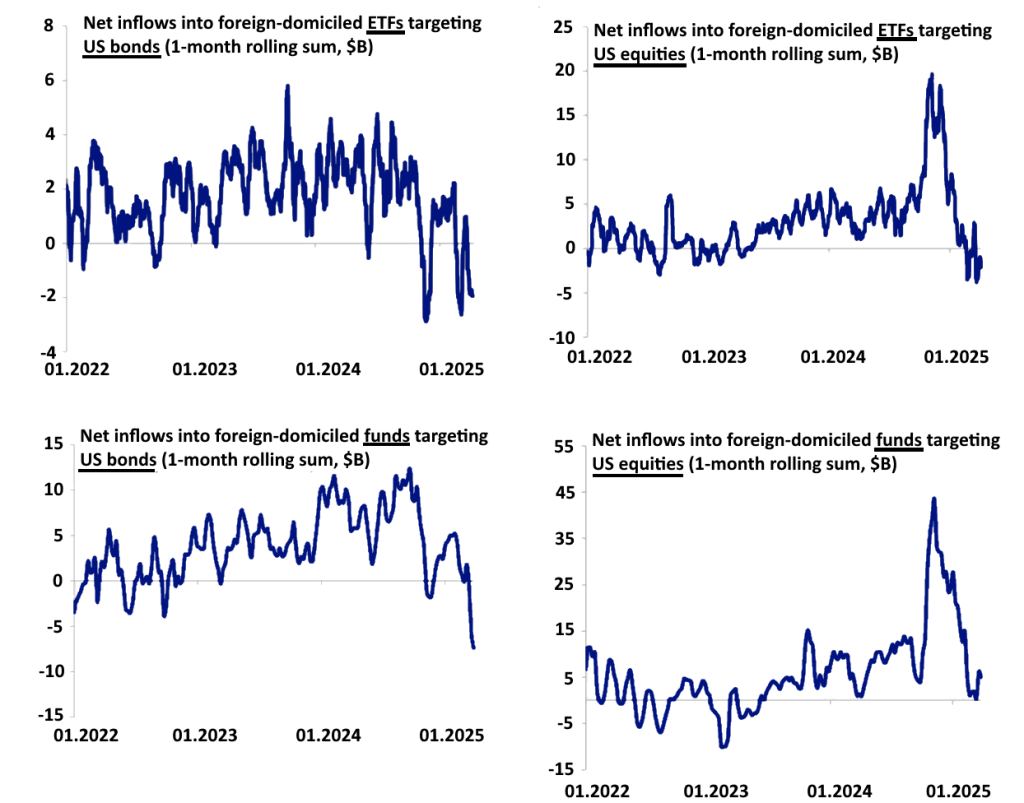

U.S. financial markets still enjoy unmatched size and liquidity (i.e., remains the deepest, most liquid, and most sophisticated globally). However, for investors already uneasy about concentrated exposure to the United States, viable alternatives are beginning to emerge. Recent months of policy unpredictability—especially following blanket tariffs and rising restrictions—have prompted international investors to explore other markets more seriously. The looming possibility of capital controls has added another layer of risk, leading some to ask whether expressing duration through Bunds might now be safer than Treasuries, due to escalating ‘country risk.’ Though definitive conclusions remain premature, emerging data suggests a slow but visible redirection of capital flows—one that couldn’t have come at a worse time for U.S. markets.

Exhibit 7: Foreign Capital Inflows Into US Bonds & Equities Slowing; Which Suggests Slowdown In Pace Of US Investment Inflows

The level of chaos and uncertainty triggered by the Trump administration in its few months has been so profound that even a complete reversal of its trade policies may not fully restore confidence or undo the damage. It’s akin to attempting to undo a process that has already set irreversible dynamics in motion. The deeper issue is not just the policies themselves, but the lasting impact of unpredictability—from persistent volatility in U.S. Treasury market to growing skepticism about the stability and credibility of U.S. economic governance, American institutions and asset markets.

In our assessment, dismantling the dollar-based global financial system would require more than just rhetoric; i.e., would demand a combination of bold and unprecedented actions. Two critical developments would need to occur. First, there would have to be a serious disruption or political interference with the Federal Reserve’s independence. Second, capital inflows into the U.S. would need to be deliberately obstructed—perhaps through an aggressive new policy agenda, which some are informally referring to as a “Mar-a-Lago doctrine.” Though we cautious to label it an “doctrine” at this stage.

Exhibit 8: U.S. Treasury Market Volatility Due To Skepticism In The Stability & Credibility Of U.S. Economic Governance

One of the key conditions we’ve been monitoring is now taking shape, and recent rhetoric has only strengthened our belief that the second is gaining serious traction. Our baseline scenario still assumes that China and the U.S. will ultimately strike a deal that reduces tariffs to around between 15-25%.

Exhibit 9: On Average, The Lifecycle Of A Trade Deal Involves An 18-Month Negotiation And Signing Period, Followed By A Significantly Longer 45-Month Implementation Phase.

However, the 90-day Trump administration tariff truce highlights the mismatch between political timelines and trade realities. This makes meaningful structural agreements nearly impossible in such a short timeframe (three-month window). Why? This is because trade negotiations are lengthy process and implementation is much slower than signing. On average, it takes more than 2.5 times longer to implement (45 months) a trade deal than to sign it (18 months), highlighting the substantial bureaucratic, legal, regulatory, and political hurdles involved in putting a signed agreement into effect.

Some investors may still find opportunities for quick gains if policy reversals occur or if institutional guardrails reassert themselves. However, for the vast majority who lack the agility or appetite for extreme risk, it appears the Trump administration has already crossed the halfway mark on a path of no return. Should it proceed further, the consequences could be catastrophic. The sheer volume of capital embedded in the U.S. dollar system has no parallel elsewhere—it simply cannot be absorbed overnight by any other market. If Trump were to reverse course, the dollar might stage a temporary recovery, but ironically, that rebound could serve as the perfect window for investors to exit on strength before deeper instability unfolds.

We believe the global economy has already entered the early stages of a profound shift—a long, deliberate process of de-dollarization; in conformity to our “New Economic Era” framework. The implications for the United States, and for the rest of the world, are nothing short of seismic. The era of an unchallenged U.S. dollar may be drawing to a close, and we expect significant weakening ahead. The signs are already unfolding:

Point #1: We think America is fast approaching the limits of its fiscal flexibility. For years, we’ve maintained that a country’s true fiscal space isn’t best measured by its debt-to-GDP ratio (i.e., debt sustainability), but by its external position—especially how reliant it is on foreign capital. Historically, the U.S. has been a rare outlier. Thanks to the dollar’s reserve currency status, it could run large current account and fiscal deficits—its “twin deficits”—without major funding issues. But that dynamic is shifting. As the dollar’s exceptional standing weakens, so too does America’s ability to sustain expansive fiscal policies. Much like the UK and France, Washington is now facing stricter limits. The implication is sobering: U.S. policymakers will have far less room to stimulate growth through fiscal means, posing long-term challenges to its economic outlook.

Point #2: U.S. foreign policy is increasingly shaping the trajectory or the evolving landscape of financial markets. It’s no longer just about de-dollarization—America’s twin deficits mean the country depends heavily on foreign capital to finance its obligations. As such, investor sentiment abroad becomes a cornerstone of bond and currency market stability. The U.S. is now in a position where it, too, must rely on the “help from unlikeliest hands”—a phrase once reserved for emerging markets with similar imbalances. This makes it imperative for the U.S. to avoid antagonizing its global partners. Even offhand remarks—such as the previous administration’s musings about purchasing Greenland—can rattle confidence in the dollar. Moving forward, Washington may need to pursue a more diplomatic, conciliatory, less confrontational and measured foreign policy approach if it hopes to maintain stable access to global capital and ensure the resilience of U.S. financial markets.

Point #3: At the heart of the matter lies one key factor: valuations. While recent U.S. market movements—where both bond and currency markets are falling—have drawn comparisons to emerging market behavior, such parallels only go so far. The U.S. stands apart in a critical way: it does not hold substantial foreign-currency-denominated debt, which means it avoids the structural kind of runaway debt spiral that plagues many emerging markets during crises. Instead, the ongoing market weakness may serve a different function. Falling prices in bonds and the dollar could eventually create more attractive valuations—paving the way for a new, more sustainable pricing equilibrium. However, the real challenge is the high starting point: U.S. assets are still expensive, with significant foreign ownership and a policy stance that many see as increasingly confrontational. Together, these factors suggest that a much deeper valuation reset is needed before global investors return in force.

##5: The Great ESG Rethink: Fundamental Shifts In Sustainability Strategies

ESG Strategies Are Undergoing Profound Change; What are the key drivers behind this “Great ESG Rethink” and what fundamental shifts are occurring in sustainability strategies?

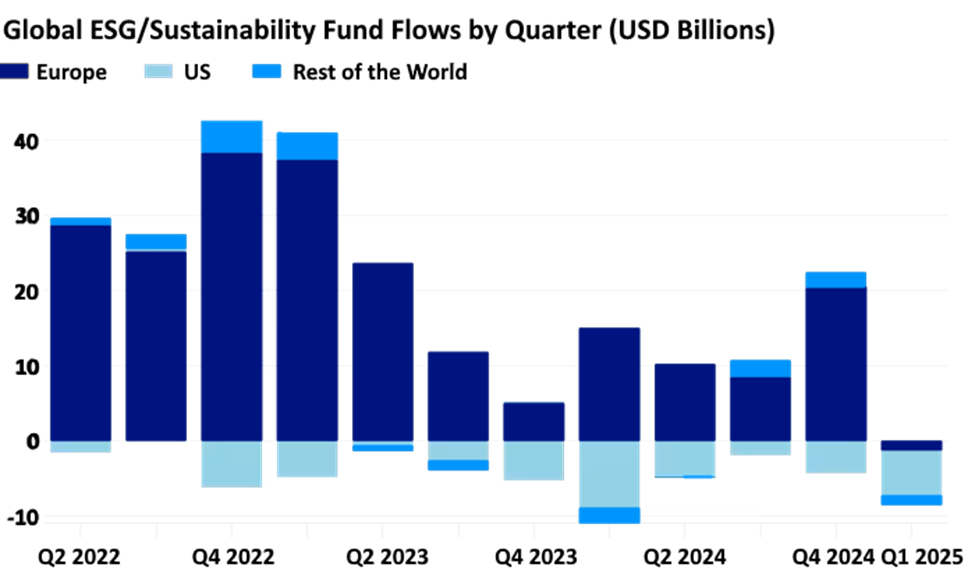

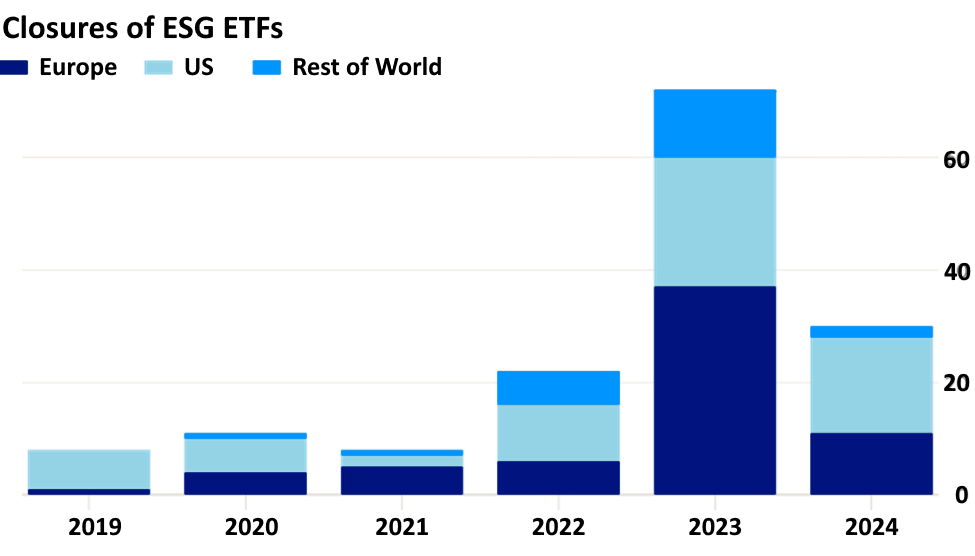

Recent data indicates a significant shift away from ESG investments, with record capital outflows observed globally over the past three years. Contrary to the “woke capitalism” narrative, this trend appears largely driven by a lower profitability of ESG assets, including growing ESG backlash originating in the US, which is making asset managers worldwide more cautious in their product strategies. This caution is further amplified by the EU’s impending stricter anti-greenwashing regulations for investment fund names. Zinqular data reveals a substantial response in Europe during the first quarter, with 340 sustainable products undergoing name changes (including 116 dropping ESG terminology) and an additional 96 funds being liquidated or merged. Simultaneously, the US experienced a record quarterly high of 20 fund closures.

Exhibit 10: Challenging Conviction: Record Outflows Signal Institutional Scrutiny Of ESG Fund Performance

Reviewing the data, this shift isn’t a tale of investors suddenly abandoning their concern for future generations or social responsibilities, nor is it a simple echo of US political debates or other global right wing political views. The underlying reason for the changing landscape of ESG investment is arguably more straightforward: in its present iteration, ESG has consistently fallen short of its promised financial performance or returns. The earlier narrative of ESG funds outshining traditional ones held true for a period, fueled by easily captured efficiencies and the market appeal of green initiatives. However, once these initial, low-hanging opportunities were exploited, the financial advantage began to erode.

Despite global widespread declarations of commitment to ethical consumption, consumers wallets tell another story—they still prefer “dirt-cheap” goods from digital retailers like Temu and Shein over sustainable, pricier alternatives. This disconnect didn’t go unnoticed by investors; ESG strategies, for all their marketing appeal, didn’t unlock new revenue streams but did pile on significant costs; worst there is no end in sight to these costs.

Exhibit 11: Institutional Investors Question “Sustainable” Fund Resilience Amid Performance Concerns

The core problem stems from a misdirected implementation of ESG principles. Rather than focusing on long-term business resilience, the emphasis shifted towards optimizing for favorable ratings and positive investor optics. The central inquiry became about superficial reporting improvements rather than the creation of genuine, enduring value for the future. Consequently, after initial easy wins in efficiency, the majority of ESG-led actions no longer offered meaningful improvements to underlying business fundamentals.

It’s unfair to fault investors for moving their money when market conditions shift and for pursuing financial returns or redirecting capital allocation to proven profitable strategies. Their mandate is not to prop up businesses solely for their noble ideals and ethical stances; that duty lies with policymakers and regulators. Investors have always had one mandate: to seek strong, risk-adjusted returns, whether short- or long-term horizon.

That said, sustainable investing is evolving, not disappearing. Impact-focused sectors—like food innovation, renewable energy, water infrastructure solutions, healthcare access, femtech, and edtech—are flourishing. Today’s sustainable investments must be concrete, data-driven, and aligned with real outcomes—not box-checking exercises; not symbolic gestures.

Zinqular’s private markets platform delivers risk adjusted alpha by focusing on sectors and strategies that thrive through economic cycles; investment philosophy grounded in fundamentals — not ideology. In a market full of slogans, we go where the cash flows are. From infrastructure with inflation-linked revenues to growth-stage companies with tangible upside, our funds deliver consistent outperformance without compromising on clarity or conviction. No distractions — just disciplined investing.

Part B: Ins & Outs – Updated Thesis of Themes We Favor

Here’s an updated scope of the investment thesis within alternatives and private markets under current macro environment of U.S. trade friction and blanket tariffs.

↑↑ Shifting to Capital-Light Business Models Re-inforced

This investment thesis remains valid—and is even reinforced—despite the implementation of U.S. blanket tariffs on other nations. While tariffs typically introduce uncertainty and cost pressures into global supply chains, they also tend to accelerate structural corporate behaviors that this thesis captures: streamlining operations, reducing capital intensity, and turning to private markets for strategic capital.

Exhibit 12: Capital-Light Business Models Have Consistently Demonstrated Superior Performance Compared To Capital-Intensive Industries, Driven By Lower Operational Costs & Greater Scalability

Our thesis is strengthened by the following:

- Continued Focus on Efficiency and Resilience: The trend towards capital-light business models remains highly relevant as companies navigate a global environment that will likely be shaped by several years of US trade friction and tariff policies; regardless of what American political party is in power. The emphasis on enhanced capital allocation, sustainability, and reduced cyclicality is even more critical for businesses seeking resilience in potentially volatile trade conditions.

- Ongoing Divestiture Activity: Public companies will adapt to the tariff landscape and likely to continue optimizing their portfolios. Divesting non-core, capital-intensive segments remain a strategic move to improve focus and financial metrics, creating a consistent flow of acquisition opportunities for private market players.

- Persistent Demand for Asset-Based Finance: The need for flexible financing solutions is likely to persist and even increase in the years following US trade friction or tariffs policies. Companies navigating altered supply chains, potentially higher input costs, and evolving trade relationships would continue to rely on asset-based finance to manage working capital and fund growth. The expansion of this market into new sectors like insurance liabilities further broadens the investment opportunity.

- Sharp Rise in “Going Private” Opportunities: Public companies finding themselves disadvantaged by tariff regimes or seeking strategic repositioning might find going private as a more attractive option to implement significant changes away from public market scrutiny.

We are particularly focused on the following themes within “capital-light business” framework:

- Asset-Based Finance Offers Attractive Risk-Adjusted Returns: The demand for diverse asset-based financing solutions is likely to grow, making this segment an attractive area for alternative credit investors seeking potentially higher yields than traditional fixed income.

- Businesses Actively Transitioning: We still favor investing in firms actively transitioning to capital-light models, whether through direct investment or acquiring divested assets, continues to be a compelling strategy in the current global economic context.

- Private Market GPs – Catalyst for Transformation: Niche PE firms specialized in turnarounds and operational expertise are well-positioned to capitalize on the need for strategic adjustments in response to trade policies, driving value creation in portfolio companies through capital efficiency and business model optimization.

- Focus on Domestic and Regional Value Chains: The context of US tariffs or trade friction might also incentivize a focus on investments that strengthen domestic or regional value chains, reducing reliance on complex, tariff-exposed international trade routes.

Alternative and private market investors who can identify and capitalize on these trends remain well-positioned for potentially attractive returns.

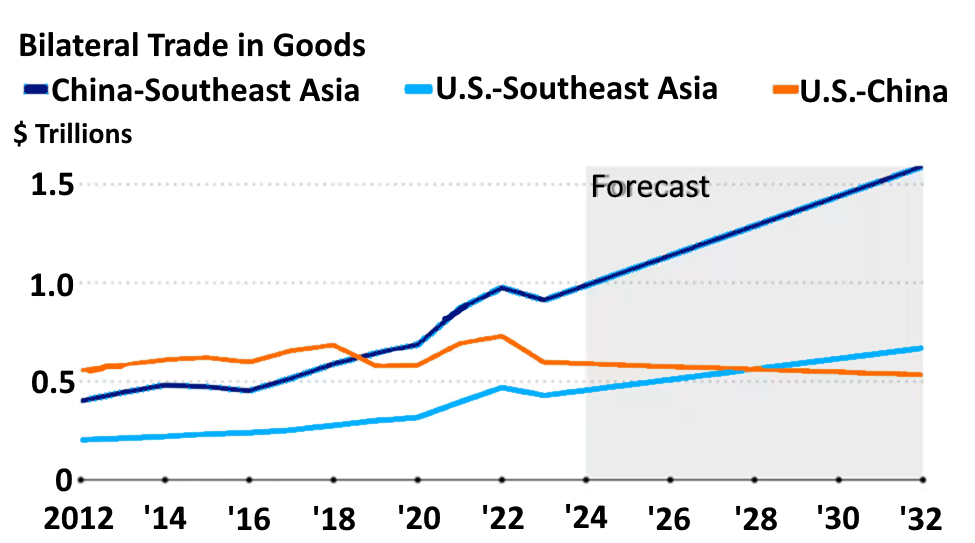

↑↑ The Rise Of Intra-Asia Trade Thesis Still Strong

Without a doubt, the investment premise on the growth of intra-Asian trade and regional integration remains compelling, even amidst broad U.S. tariffs, especially for alternative and private market investors. Indeed, these tariffs could strengthen and expedite key aspects of this thesis. Our conviction is that:

- Reinforced Intra-Regional Focus: Asia is a market of ~5.8 billion population – offering unparalleled growth opportunities. US tariffs on other nations (not just the US on Asia) can further incentivize Asian economies to deepen their intra-regional trade relationships. If trade with other major global blocs becomes less predictable or more expensive due to tariffs, the logic for investing in the infrastructure and financial mechanisms supporting intra-Asian trade becomes even stronger.

- Accelerated Supply Chain Diversification & Resilience Enablers: US tariffs on various countries can accelerate the trend of multinational companies diversifying their supply chains away from reliance on any single nation or trade bloc, including potential over-reliance on the US market. This benefits India and Southeast Asia as alternative manufacturing and logistics hubs, directly supporting the investment thesis in these regions’ data centers, logistics infrastructure, lower-cost manufacturing and advanced manufacturing capabilities.

- Increased Demand for Regional Financing: As intra-Asian trade and investment grow, the need for robust regional financial institutions and credit markets will also increase. US tariffs could make reliance on Western financial firms more complex or costly for some Asian entities, further fueling the growth of local Asian banks and non-bank lenders, creating opportunities in Asian liquid and private credit.

- Relative Stability and Growth in Asia: If US tariffs lead to economic slowdown or instability in other parts of the world, the relatively strong growth prospects and increasing internal demand within Asia could make it an even more attractive destination for alternative and private market investments seeking stable and high returns.

Exhibit 13: Intra-Asia Trade Poised To Exceed $1 Trillion By 2032, Fueling Regional Economic Growth

However, we are not oblivious to note potential risks: A) Indirect Impact of Global Slowdown: While Asia’s internal dynamics are strong, a significant global economic slowdown triggered by widespread tariffs could still negatively impact Asian growth. B) Specific Tariff Impacts: The specific nature and targets of US tariffs could still have unintended negative consequences for certain Asian industries or supply chains.

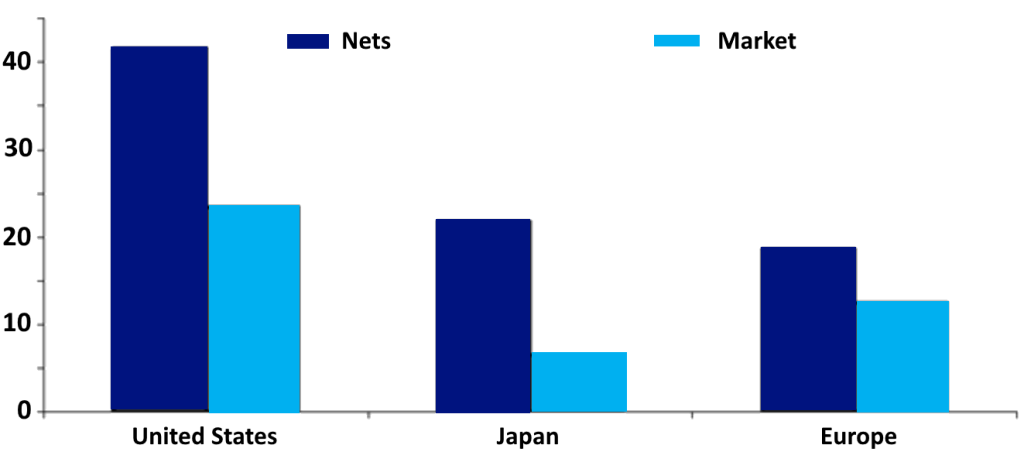

↑↑ Japan “Net-Nets” Outperformance In The Next Decade – Strengthened

Japanese “Net-Nets” thesis remains robust—even in the context of rising U.S. tariffs on other nations, including Japan. In fact, the core drivers of this strategy are largely insulated from trade policy shocks and may even benefit from them under certain conditions.

Exhibit 14: Japan’s “Net-Nets” Assets Poised To Outshine Global Competitors In The Coming Years.

Reviewing the data, we can deduce that:

- “Net-Nets” Are Inherently Defensive in a Protectionist Environment: The core of the “Net-Nets” strategy is identifying undervalued domestic Japanese companies trading below their net current asset value; with high cash balances, minimal debt, and low valuations. This suggest that U.S. tariffs that affect Japan’s export-heavy giants (e.g., autos, electronics) may not materially impact smaller domestic-focused or cash-rich “Net-Nets.”

- Corporate Reform Momentum Offers Structural Tailwinds: Japan’s continued push for governance reforms (driven by the Tokyo Stock Exchange and activist pressure) aimed at improving capital allocation, reducing cross-shareholdings, and enhancing shareholder value; supports re-rating potential for undervalued stocks. US tariffs on other nations do not directly impede these internal reforms. Tariffs could actually accelerate reform by encouraging companies to unlock balance sheet inefficiencies in order to boost shareholder returns and maintain competitiveness.

- Historical Outperformance: The strong historical track record of “Net-Nets” outperforming in Japan across various economic cycles suggests that this strategy has a degree of resilience to broader global economic headwinds, including those potentially arising from tariff disputes. The undervaluation inherent in these companies can provide a buffer against market volatility.

Private & Alternatives investors benefit from public-to-private transitions under this theme. Deep discounts to net asset value and stagnant share prices despite strong balance sheets make many “Net-Nets” ideal targets for: Activist engagements, Corporate carve-outs, Take-private transactions, Event-driven value realizations, Special situations or value-focused PE funds. For alternative investors, these inefficiencies represent buyout or strategic control opportunities, with built-in downside protection.

Exhibit 15: Amidst Continued Corporate Reform, Japanese Assets Present A Compelling Value Compared To Global Peers.

Even in a tariff-constrained world where Japanese “Net-Nets” offer a compelling, value-driven strategy with limited downside and growing upside catalysts, it’s important to consider potential indirect risks: A) Global Economic Contagion: A significant global economic downturn triggered by widespread tariffs could still negatively impact Japanese market sentiment and potentially even the valuations of “Net-Net” companies. B) Unforeseen Policy Shifts: Unexpected policy changes in Japan or the US could still have unintended consequences for Japanese equities.

↑↑ Biotechnology: A Sector Undervalued Amidst Market Volatility Remains Attractive

Overall, the investment thesis for biotechnology as an undervalued sector with strong long-term growth drivers appears robust and largely resilient to the direct negative impacts of US tariffs on other nations. The fundamental drivers within the sector, coupled with attractive valuations and its defensive characteristics, make it a compelling area for alternative and private market investors. Why is biotech resilient amid tariffs? We think:

- Biotech Is Largely Domestic & IP-Based: Unlike heavy manufacturing or energy, biotech firms—especially those in drug discovery, gene therapy, and personalized medicine—are not heavily dependent on global trade flows or import/export dynamics. Most value lies in intellectual property, R&D, and regulatory approvals, not physical goods. Additionally, core drivers of the biotech investment thesis – increased technological investment, aging demographics, and industry consolidation – are largely independent of US tariff policies on other nations. These are long-term secular trends that will continue to fuel innovation and demand within the healthcare sector globally.

- “Reshoring” Strengthens the Thesis: The growing emphasis on “reshoring” biotech production and its recognition as critical for national security. US tariffs on other sectors could inadvertently strengthen this trend, as governments prioritize domestic production of essential goods like pharmaceuticals and related technologies, potentially benefiting national/regional focused biotech companies.

- Private Markets Can Exploit Dislocation: The ongoing underperformance of public biotech (e.g., Nasdaq Biotech Index) presents a valuation gap that can be exploited in private markets through: Take-privates of undervalued firms, Growth equity investments in clinical-stage startups and Structured credit to biotech ventures squeezed by capital markets.

- We Think Sector Consolidation = Opportunity: Tariffs and macro uncertainty could accelerate industry consolidation, allowing private investors to acquire or back stronger survivors at distressed valuations. In addition, the current undervaluation of biotech stocks, with price-to-book ratios approaching GFC levels, presents a compelling entry point for long-term investors, regardless of the global trade landscape. Market volatility created by tariffs might even exacerbate this undervaluation in the short term, creating opportunities for patient capital in alternatives and privates.

Long term asset allocators should focus on innovation and breakthrough therapeutic themes. Investments in biotech companies focused on cutting-edge technologies and addressing unmet medical needs are likely to remain attractive, as their value proposition is less dependent on broader macroeconomic factors like tariffs. The combination of favorable policy tailwinds, national security imperatives, and valuation resets creates an attractive setup for alternatives investors over the next 5–10 years.

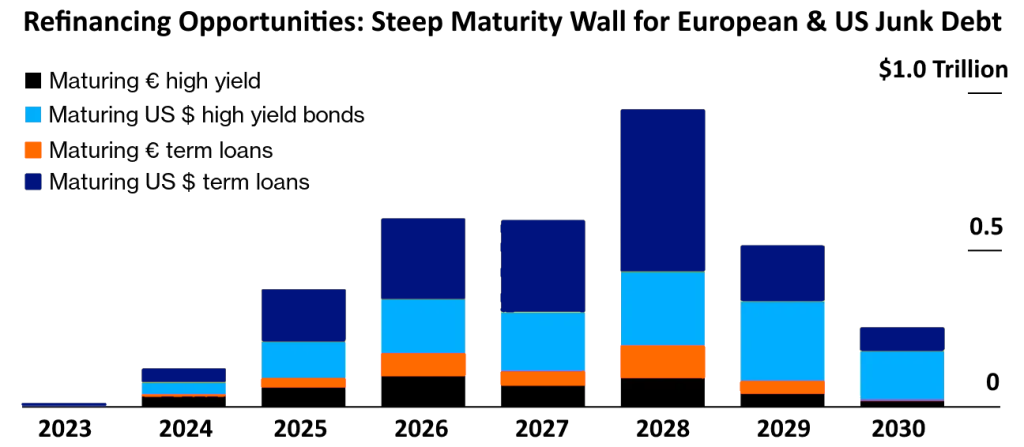

↑↑ Capital Solutions & European Credit: Compelling Near-Term Opportunities

Overall, the investment thesis focusing on near-term European high-yield credit and the demand for capital solutions in Europe appears to be largely resilient to US tariffs on other nations. The key drivers are regional (ECB policy, maturity wall, relative value) and the potential for increased demand for capital solutions in an uncertain global environment.

Exhibit 16: A Large Share Of European High-Yield Bonds Are Set To Mature In The Next 3-5 Years, Offering A Major Refinancing Opportunity

Here is why, along with some underlying reasons:

- Limited Direct Impact from U.S. Tariffs: European HY credit is primarily influenced by regional macro factors, such as ECB policy and local corporate refinancing needs—not U.S. trade dynamics. U.S. tariffs on other nations (including Europe) may have sector-specific consequences (e.g., autos, industrials), but they do not broadly impair the HY credit or capital solutions landscape in Europe. The anticipated ECB rate cuts are part of the drivers of this thesis, making shorter-maturity European HY attractive for potential capital appreciation as yields decline. This monetary policy outlook is largely independent of US tariff policies.

- Near-Term Maturity Wall Creates Opportunity: The significant amount (45%) of European HY maturing by 2026 creates a natural refinancing cycle. Companies will need capital to address these maturities, and the expectation of lower rates could incentivize them to refinance sooner rather than later, benefiting investors in shorter-dated instruments regardless of US tariffs policy. This urgency creates strong deal flow for investors. Consequently, refinancing cycle provides a clear exit strategy for asset manager. The significant near-term maturities in European HY offer a relatively visible exit pathway for investors. In addition,the “bargain” aspect compared to US HY on a spread basis makes European credit attractive on its own merits, irrespective of US trade friction. Investors seeking yield might find European HY more compelling relative to its US counterpart.

- Demand for Capital Solutions: In an environment potentially marked by global economic uncertainty (which US tariffs can contribute to), companies might be hesitant to raise common equity due to valuation concerns or market volatility. This would likely increase the demand for alternative capital solutions, such as private credit, mezzanine financing, and other structured debt. European firms are not immune to such uncertainty.

↑↑ Inflation Protection With Real Assets: Collateral-Based Cash Flows – Still Valid

The investment case for Real Assets and Asset-Based Finance is strengthened, not weakened, by the macro volatility and inflation dynamics that tariffs can trigger. Within the alternatives and private markets space, these strategies offer a resilient hedge and attractive risk-adjusted returns that are largely decoupled from global tariff policy shifts. This investment thesis holds due to:

- Real Assets Are Largely Domestic or Regionally Anchored: Real assets such as infrastructure, energy transmission, and real estate credit are less exposed to global trade flows, making them relatively immune to tariff shocks. Their value is often derived from domestic demand, regulatory frameworks, and local pricing power, not cross-border exports.

- Intrinsic Inflation Hedging Value Is Independent of Tariff Policy: The underlying thesis is driven by inflation protection and yield stability. Since tariffs may themselves exacerbate inflationary pressures (especially in supply-constrained environments), the demand for inflation-hedging instruments like real assets only becomes stronger. The burgeoning energy demands, the need for robust energy transmission networks, advanced data centers, and efficient cooling solutions will persist and likely grow, irrespective of specific trade relationships between the US and other nations

Therefore, the investment thesis advocating for inflation protection through Real Assets and a significant allocation to Asset-Based Finance appears robust and well-positioned to deliver value for alternative and private market investors in the current global economic landscape, even with the presence of US tariffs on other nations

↑↑ Uranium: A Strategic Play On The Nuclear Renaissance – Strengthened

The Uranium investment thesis remains resilient and compelling, even in the face of broad U.S. tariffs. If anything, tariff-induced energy insecurity may reinforce the strategic value of nuclear power, strengthening investor interest in uranium supply chains and nuclear infrastructure. For alternative and private market investors, this theme offers a long-duration, asymmetric opportunity tied to global decarbonization, energy resilience, and geopolitical realignment. A summary of compelling reasons:

- Global Decarbonization Imperative: The fundamental driver for nuclear energy’s growth is the increasing global recognition of its role in energy resilience and mitigating climate change. This imperative transcends specific trade policies between the US and other nations. Countries worldwide are setting ambitious emissions reduction targets, and nuclear power offers a reliable, low-carbon baseload energy source.

- Uranium Market Dynamics Are Largely Geopolitical & Supply-Driven: Unlike consumer or industrial goods, Uranium is not broadly traded on open commodity markets and is often sourced through long-term, bilateral agreements. Tariffs on general goods do not directly impede the structural supply-demand imbalances in Uranium, especially given the growing demand driven by energy security and decarbonization agendas.

- Structural Uranium Supply Deficit: The thesis highlights a growing structural supply deficit in Uranium. This is driven by years of underinvestment in mining and production, coupled with increasing demand from new reactors. US tariffs on other goods are unlikely to significantly alter this fundamental supply-demand imbalance in the Uranium market. China’s massive and sustained investment (USD150 billion) in nuclear power is a key pillar of the Uranium demand story. Their ambitious expansion plans, driven by their own energy security and climate targets, are a significant and independent driver of Uranium demand, irrespective of US trade policies towards other countries.

- Global Nuclear Renaissance: The data on the number of reactors under construction and in planning stages globally (outside of just the US) underscores a worldwide resurgence in nuclear energy. This trend is driven by energy security concerns, the need for stable baseload power, and climate goals, factors largely independent of US tariff policies. U.S. Tariffs Reinforce Domestic and Allied Nuclear Investment. U.S. protectionist policies may accelerate onshoring of clean energy production, including nuclear. This could result in greater federal and private investment in domestic uranium enrichment, fuel-cycle services, and small modular reactor (SMR) technology—providing more upside for private capital and alternative investors.

Reviewing investment landscape, we think private market opportunities in uranium remain robust Private capital can access the uranium story through:

- Direct investments in mining, development-stage projects, or exploration companies.

- Infrastructure finance for nuclear build-outs in emerging markets or SMRs in OECD countries.

- Structured finance and commodity-linked debt, particularly in jurisdictions aligned with U.S. trade policy (e.g., Canada, Australia, Kazakhstan).

Exhibit 17: China Plans For Ambitious Nuclear Energy Expansion

Exhibit 18: China Could Soon Overtake France On Nuclear Power Capacity, With Projects Expected To Come Online In Next Few Years

In conclusion, the investment thesis for Uranium as a strategic play on the nuclear renaissance holds strong, and arguably becomes even more compelling in a world grappling with energy security and climate change, largely independent of US tariff policies towards other nations. China’s massive nuclear buildout and the global push for decarbonization provide powerful tailwinds for Uranium demand, making it an attractive opportunity for alternative and private market investors seeking long-term growth potential.

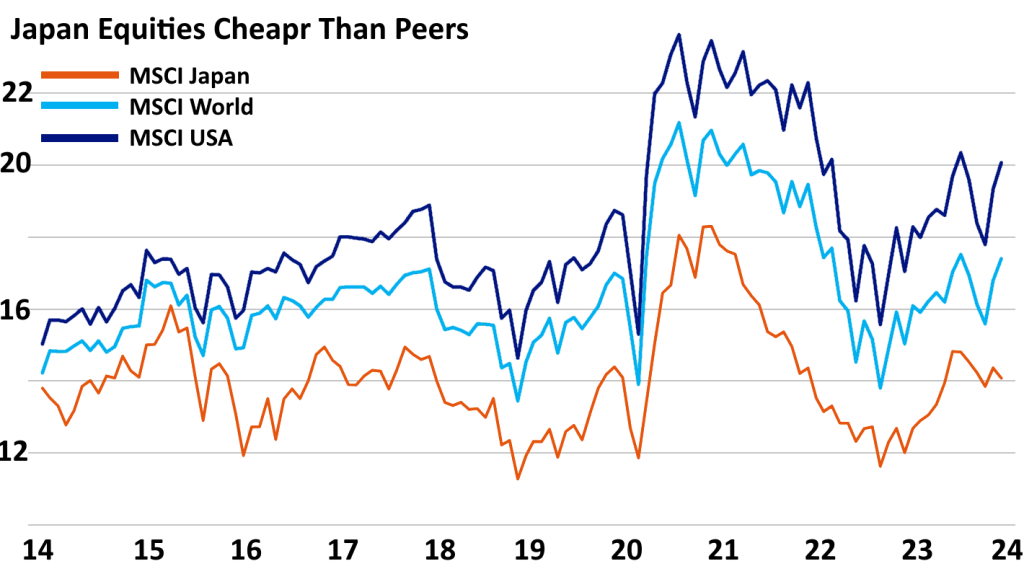

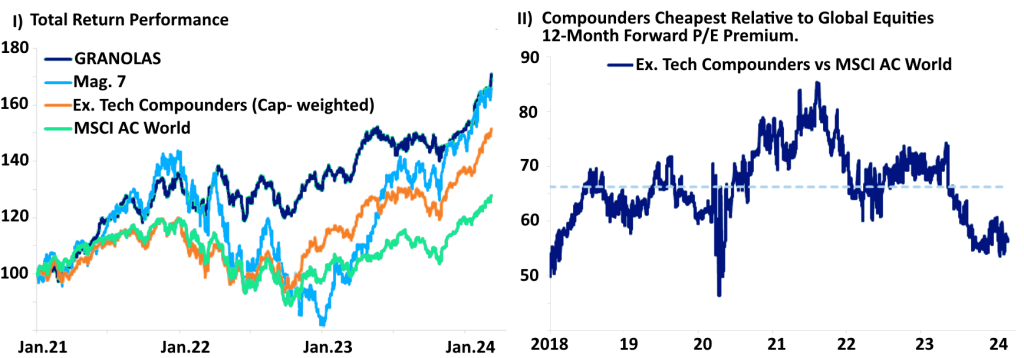

↑↑ Undervalued Gems Beyond The Technology Titans In A Concentrated Market – Largely Robust

Despite ongoing or future U.S. tariffs on global trade partners, the thesis around undervalued, high-quality secular compounders remains robust—and may even be strengthened by the distortion and capital misallocation caused by protectionist policies. For alternative and private market investors, this opens pathways to opportunistic M&A, structured credit, or minority investments in overlooked assets with long-term compounding potential.

Exhibit 19: Secular Ex-Tech Compounder Present Compelling Opportunity In The Near Term

The following summarizes the reasons:

- Secular Compounders Are Often Domestically Anchored & Sectoral Focus: Many of these non-tech secular compounders operate in sectors such as healthcare, consumer goods, industrials, and business services—industries less exposed to cross-border trade frictions than globally integrated tech manufacturers. The core of this thesis is identifying high-growth, non-tech companies with strong fundamentals and durable competitive advantages that are currently undervalued relative to the broader market, particularly the “Magnificent Seven” tech giants. This undervaluation and the companies’ intrinsic strengths are primarily driven by domestic and sector-specific factors, not directly by international trade policies or US tariffs on other nations.

- Value Opportunity: Tariff-Driven Volatility Can Create Entry Points. Tariffs tend to disrupt valuations and create inefficiencies across equity markets—especially for less-followed names. This enhances opportunities for value-driven private capital to accumulate quality businesses at attractive entry multiples, particularly those overlooked due to macro sentiment or sector biases. The significant discount (around 60% on a forward P/E basis) to the broader market, particularly the tech sector, presents a compelling value proposition. This relative undervaluation exists regardless of the specifics of US trade policy. Investors seeking diversification and value beyond the concentrated tech rally are likely to find this thesis attractive.

- Diversification Away from Tech Concentration: In a market heavily concentrated in a few technology names, allocating to undervalued secular compounders in other sectors provides crucial diversification benefits, reducing portfolio risk associated with potential tech sector corrections or specific trade-related impacts on the tech industry.

Alternatives and private market investors can capitalize via take-privates or growth equity strategies. The investment thesis highlighting undervalued secular compounders outside the technology sector remains a compelling opportunity. The domestic focus, strong fundamentals, attractive valuation, and diversification benefits offered by these companies are likely to persist and even become more appealing, irrespective of the specific impacts of cross border trade friction.

↑↑ Comprehensive Security: Resilience Across Industries & Nations – Has Amplified

The “Comprehensive Security” thesis is not only resilient in a world of rising geopolitics but is partially driven by it. For alternatives and private markets, this theme offers a durable, long-horizon opportunity with support from structural trends, public policy, and geopolitical realignment. It is especially well-suited to strategies in infrastructure, private equity (defense-tech, cyber), and private credit (supply chain and storage solutions). Here are few reasons we believe it amplifies this thesis:

- Rising Geopolitics & Tariffs Reinforce the Demand for Resilience and Localization: Rising Geopolitics and U.S. tariffs on imports, especially from strategic rivals, underscore the need for national self-reliance in critical sectors like energy, defense, healthcare, and semiconductors. This creates a tailwind for private investments in: 1) Onshoring manufacturing and R&D; 2) Cybersecurity for financial and defense systems; and 3) Redundant infrastructure and localized supply chains.

- Cybersecurity as a Universal Imperative: The increasing frequency and sophistication of cyber threats, particularly highlighted by post-2023/24 breaches demand continuous and escalating investment in cybersecurity across all sectors and nations. This is a fundamental need that transcends trade policies.

- Government Initiatives Provides Tail Risk Mitigation: Industrial policies supports infrastructure & resilience. Legislation such as the US Inflation Reduction Act (IRA), EU Green Deal, REPowerEU Plan, and increased defense budgets (across China, Japan, NATO, Russia, S. Korea, etc.) create a regulatory and fiscal floor for many sectors aligned with this theme. This reduces downside risk and improves the risk-adjusted returns of projects related to: 1) Clean energy grids; 2) Domestic pharmaceutical production; 3) Advanced transportation networks, and 4) defense infrastructure. Comprehensive security as a secular growth trend is critical and strong. These trends are likely to continue, providing long-term support for security and resilience investments.

- Global Expansion Despite Tariffs: While U.S. tariffs may constrain some cross-border flows, the push for national and regional resilience is global. China, Europe, Japan, ASEAN and India are investing heavily in the same themes—creating co-investment opportunities for global private capital. In particular, non-tariff-affected partners and allies offer parallel deal flow with fewer geopolitical constraints.

The investment thesis centered on Comprehensive Security and Resilience is not only robust in the face of US tariffs on other nations but is likely to be further validated and strengthened by the increased geopolitical risks and supply chain disruptions that such policies can contribute to. The fundamental need for security across cyber, physical, and supply chain domains remains a paramount concern for businesses and governments globally, creating compelling and long-term investment opportunities within alternatives and private markets.

↓ Challenges Ahead For Low-Cost Consumer Discretionary Spending – Gains Urgency

Blanket U.S. tariffs magnify the headwinds already facing low-cost consumer discretionary businesses. Within alternatives and private markets, this calls for disciplined underwriting, selective exposure, and a shift toward recession-resilient or value-oriented consumer investments. Here’s why, along with some thoughts:

- Exacerbated Inflationary Pressures (Tariffs Amplify Input Costs for Low-Margin Products): Many low-cost discretionary goods (e.g., fast fashion, small electronics, home goods) depend heavily on Chinese manufacturing. U.S. blanket tariffs directly raise import costs, compressing already thin margins and limiting profitability. This reduces the investability of these companies from a private equity or growth capital lens unless they have significant supply chain flexibility or pricing power. This would further strain the already tight discretionary budgets of the target demographic (younger and lower-income consumers).

- Reduced Purchasing Power (Lower-Income Consumer Segments Are Disproportionately Impacted): U.S. and European low-income consumers, already constrained by inflation in food, housing, and healthcare, are most sensitive to price increases. As tariffs raise the cost of goods, demand for discretionary items declines faster among these cohorts. This makes the consumer discretionary segment riskier for private credit and equity investors, especially in sub-sectors such as: 1) Fast-casual dining; 2) Discount retail; 3) Low-end electronics and homeware. Higher prices on non-essential goods due to tariffs would lead to a further reduction in the purchasing power of the already financially stretched consumer base. This would likely accelerate the pullback from discretionary purchases.

- Private Market Players Shift Toward Resilience-Focused Consumer Strategies: Investors should shift focus toward resilient consumer business models—those that serve essential needs, offer value-based propositions, or benefit from premiumization. Opportunities may still exist in: 1) Durable goods with U.S. or nearshore supply chains; 2) Brands with strong DTC channels and low-price elasticity; 3) Subscription models offering recurring revenues.

There is an adjustment going on; a shift toward resilience-focused consumer strategies. Investors should shift focus toward resilient consumer business models—those that serve essential needs, offer value-based propositions, or benefit from premiumization. Opportunities may still exist in: 1) Durable goods with U.S. or nearshore supply chains; 2) Brands with strong DTC channels and low-price elasticity; 3) Subscription models offering recurring revenues. Some strategic actions of private market players include:

- Private Equity: Investors may increasingly avoid low-cost discretionary targets unless there’s a clear path to automation, localization, or vertical integration.

- Private Credit: Rising input and operating costs increase default risk for leveraged low-margin consumer businesses.

- Distressed & Turnaround: Tariff-induced margin pressures may create opportunities in restructuring or operational transformation plays.

In summary, the investment thesis centered on low-cost consumer discretionary spending faces significant headwinds due to persistent inflation, competition for resources, limited wage growth, and the direct negative impact of US tariffs on goods from other nations (particularly China). Alternative and private market investors should likely exercise caution and explore investment opportunities in more resilient consumer segments or sectors less directly exposed to these pressures.

↓ Sub-Investment Grade Credit & Non-Controlling Equity Stakes – Higher Risks

The investment asset class is weakened by heightened macro risks—due to calls for even stricter discipline, higher underwriting standards, and preference for control or governance-enhanced structures. The following metrics amplifies this thesis:

- Increased Caution in Sub-Investment Grade Credit: The risks in lower-rated, unsecured high-yield credit are amplified by the potential for tariff-induced economic slowdown and a weaker dollar impacting corporate profitability and debt servicing capacity. A highly selective and quality-focused approach is essential.

- Stronger Preference for Control Equity: The ability to implement strategic and operational changes to mitigate tariff and currency risks makes control-oriented private equity strategies significantly more appealing than non-controlling stakes. Active management becomes a key differentiator.

- Focus on Companies with Pricing Power and Strong Balance Sheets: When considering both credit and equity investments, prioritize companies with strong pricing power to offset potential cost increases from tariffs or a weaker dollar, and those with robust balance sheets to weather economic uncertainty.

- Importance of Currency Hedging and International Expertise: For investments with international exposure, expertise in currency hedging and navigating global trade dynamics will be increasingly valuable for alternative and private market investors.

↓ Uncollateralized Credit – Amplified Headwinds

The US tariffs on other nations acts as a significant headwind to the unsecured credit market, particularly for non-prime borrowers. It amplifies the vulnerabilities highlighted in the investment thesis, making a cautious and selective approach to this segment within alternatives and private markets even more critical. The focus should likely shift towards more secured lending strategies and thorough risk assessment in unsecured portfolios. So why does the vulnerabilities in uncollateralized credit holds and is likely amplified:

- Exacerbated Consumer Financial Strain: Due to increased prices for imported goods thereby intensifying the prioritization of essential spending by non-prime borrowers, leaving even less room for servicing discretionary debts like unsecured loans.

- Increased Risk of Unemployment: While the initial benchmark projected a mild increase in unemployment, the continued presence of US tariffs could create broader economic headwinds, impacting various sectors and potentially leading to a more significant rise in unemployment than initially anticipated. Job losses directly impair borrowers’ ability to repay unsecured debt.

- Heightened Impact of Lax Underwriting: Any lenient underwriting standards adopted during periods preceding the full impact of tariffs would become even more problematic as borrowers face increased financial pressure. The lack of collateral in these loans means higher potential losses for lenders and investors.

Therefore, alternatives and private market investors will:

- Reinforced Caution on Unsecured Credit: The investment thesis advocating for caution regarding uncollateralized consumer credit, especially in the non-prime segment, is strengthened in a landscape influenced by US tariffs. The risks of higher defaults and lower recovery rates are elevated. Next, while rising defaults in unsecured credit might create distressed debt opportunities, investors should proceed cautiously, focusing on robust recovery analysis and understanding the underlying borrower demographics in a potentially weakened economic climate.

- Increased Attractiveness of Secured Lending: The relative safety and downside protection offered by collateralized credit (e.g., asset-based finance, secured real estate lending) become even more appealing compared to unsecured credit in a potentially volatile economic environment shaped by tariffs.

- Focus on Resilient Sectors: Alternative and private credit investors should prioritize sectors and borrower segments that are less directly impacted by international trade and tariff-related price increases.