Authors: Barry Simon Graham (Co-CIO) and Michael Yaw Appiah (Co-CIO)

[wpfd_single_file id=”1979″ catid=”327″ name=”Global Investment & Economic Outlook 2022″]

Real / Nominal Rate Risks

Worry #1: An Unusual, Unexpected Move in Real and/or Nominal Rates. Does the world’s economy face greater risks from Fire (i.e., the risk that growth was too hot), or Ice (i.e., the possibility that growth undershot expectations)? In our humble opinion at Zinqular, we believe that “Fire”, not “Ice”, is the bigger risk. However, given occasional long COVID shutdowns, the uncertainty surrounding new variants, and rising geopolitical tensions, our strong view is that a Fire environment will not be too drastic. It is key to why we believe real rates will stay long at a time when nominal GDP stays strong.

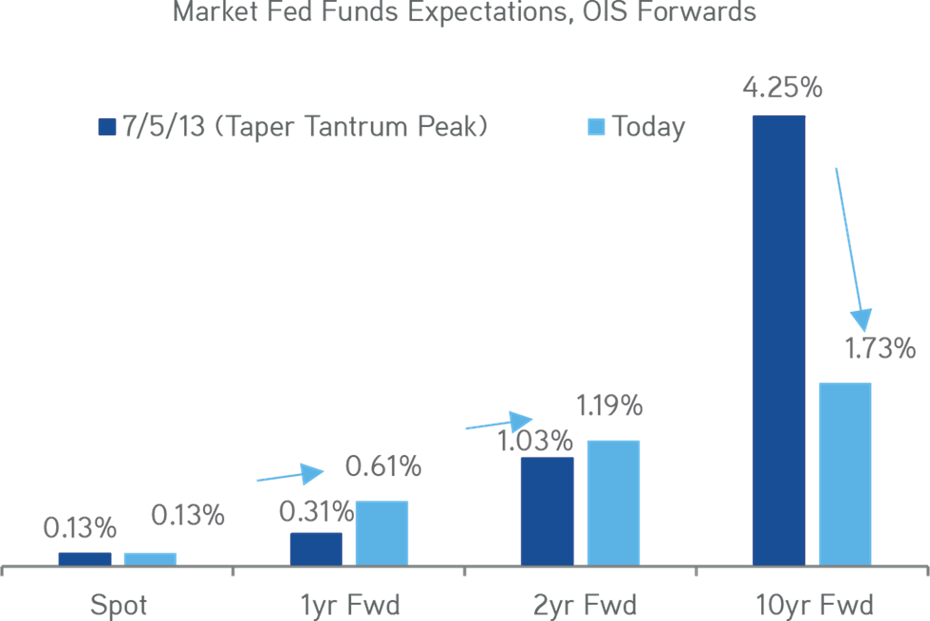

Exhibit 97:

The Risk We See Are At The Long-End Of The Curve…

Data as at December 11, 2021. Source: Bloomberg.

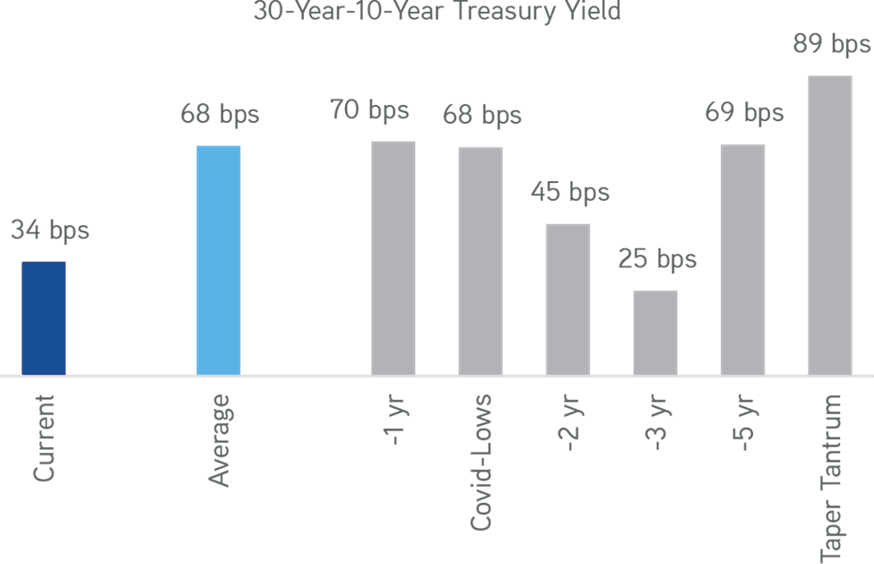

Exhibit 98:

Specifically, As We Move Further Out the Curve

Data as at November 23, 2021. Source: Bloomberg.

Supposing, we are wrong and central bankers did have to withdraw liquidity much faster than anticipated, then this outcome certainly depicts greater risk to investors. It could turn up one of two ways. One, real rates could rise as growth and inflation expectations are falling; or real rates could stay negative, but permanent, sticky inflation pushes nominal rates towards uncomfortable levels that lower valuations and credit spreads. Regardless, these types of events would certainly signal that we are much farther on cycle than anticipates.

Remember, an overly aggressive central banking community is not our base case, but we do accept that the winds of fortune are starting to change. Here is how we want to hedge against these types of outcomes:

If you think growth will potentially undershoot or the ICE scenario, we suggest remaining long 5-7 year duration via either outright receiver fixed swaps or 6-month receiver swaptions in the United States. This part of the curve is attractive, particularly given the divergence between U.S. and European rates in these tenors. Additionally, we believe this part of the curve is where U.S. rates would be most impacted in an ICE scenario.

For those who think in the risk of a FIRE scenario (which we believe is more likely), we suggest 6-month payer swaptions on the 5-year swap rate. These instruments will do well if growth and inflation overshoot and the Fed hikes rates at a faster than anticipated pace over the next several years.

Geopolitical Risks

Worry #2: Geopolitics Risks. We think that there is consensus in Washington for being tough on China as an emergent/emerged competitor capable of threatening United States’ status as a superpower. Our view is the Biden Administration is building a global “coalition of the willing” to tackle and/or balance China’s influence. In short, the US-China bilateral relationship is that the U.S. will compete where needed, confront when necessary, and cooperate where possible. Other countries and regions including Australia, Japan, India and the European Union are reexamining political and economic partnerships/cooperation as well as regulatory and data privacy issues as they try to navigate and balance the shifting world order.

Examples of couple of issues are as follows: One, rule of law and data concerns have become increasingly tense across a wide swath of countries. Two, we expect supply chains to splinter further, particularly in key areas such as 6G/5G, data, semiconductors, and healthcare. However, there are still trade-offs, including low-cost production, that must be considered before moving aggressively. Remember that the AmCham China 2021 white paper found almost 85% of members are actually not considering relocating manufacturing or sourcing away from the China market.

Regarding capital flows, we do want to emphasize that our base view still is that capital will continue to flow freely across borders, albeit with greater scrutiny, oversight and approval conditions. The fact is that China needs foreign inflows into its capital account to sustain its growing consumption economy as its current account balance moves into deficit. In contrast, many countries not only rely on China’s exports but also want access to its large consumer market.

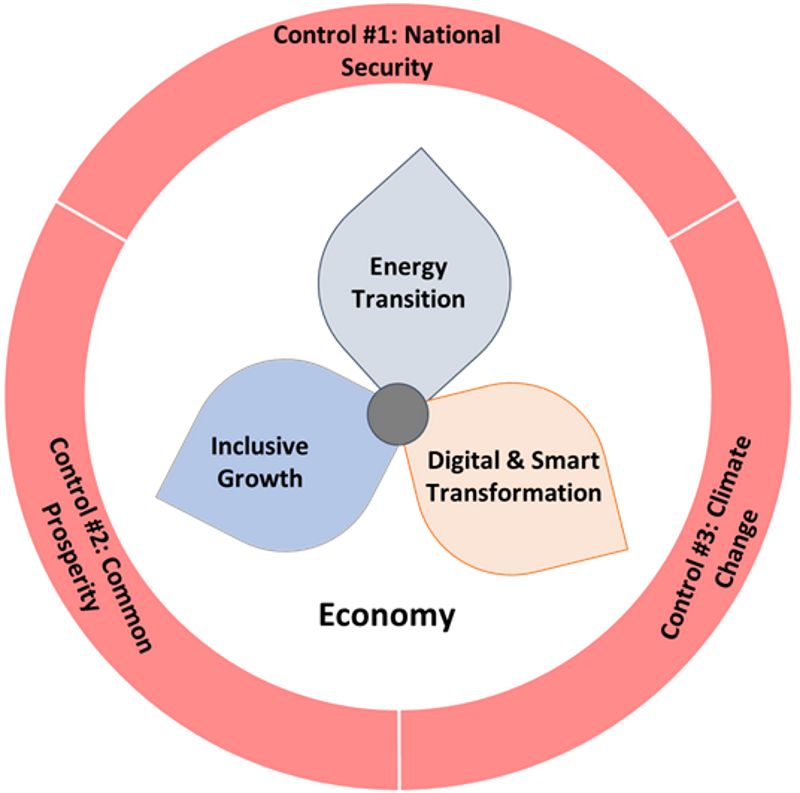

Exhibit 99:

In China Today, Investors Need Agile Framework to Succeed

Data as at December 3, 2021. Source: Zinqular Insights & Research Hub analysis.

The question goes like this: how do we hedge rising geopolitical risks? We start with the base premise that global investors should not hastily be over-committed to China — or any country for that matter. In tune with this view, we have noticed an increasing number of advisory boards encouraging CIOs to agree to a more diversified Asia-Pacific portfolio, including deploying capital in ‘new’ markets such as the Philippines, Vietnam and Indonesia. Additionally, within allocations to more complicated markets like China, we may consider investing with local players that understand the nuances of Exhibit 99 and that can align themselves with China policy.

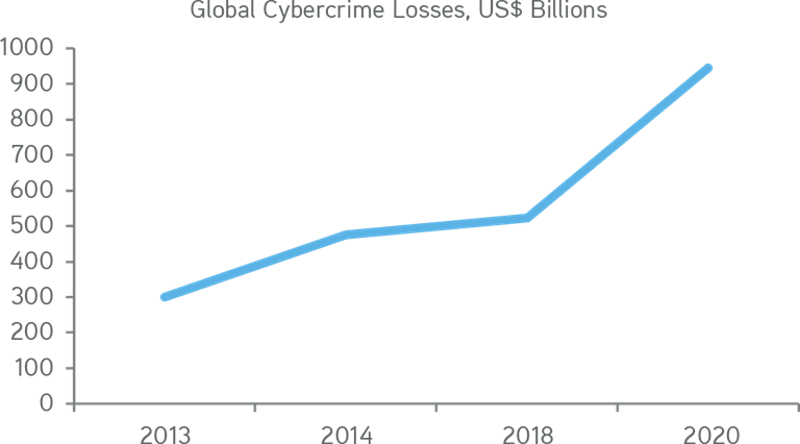

Exhibit 100:

Since 2018 Cybercrime Cost has Increased Over 50%

Data as at December 2, 2020. Source: The Hidden Costs of Cybercrime, McAfee and CSIS.

Commodities Price Risks

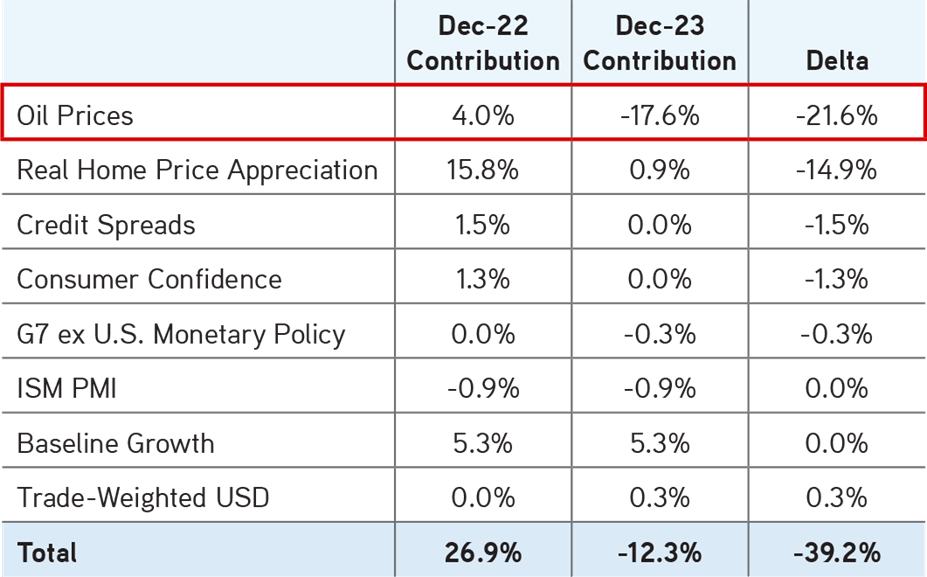

Worry #3: Commodity Prices Spikes. You may recall, our base case is that consumer demand and strong capital expenditures outweigh the ‘squeeze’ from rising input costs. Even so, given how tight supplies are on a global basis, there is a high degree of risk that we have a further commodity spike in 2022. Demand will be dented when this occurs, puncture corporate margins, and tighten financial conditions. Referencing Exhibit 102, our proprietary earnings (EPS) lead indicator is already being negatively impacted by higher energy costs. Supposing input costs rise further from here, it would certainly pull forward and intensify the slowdown we are already forecasting for 2023.

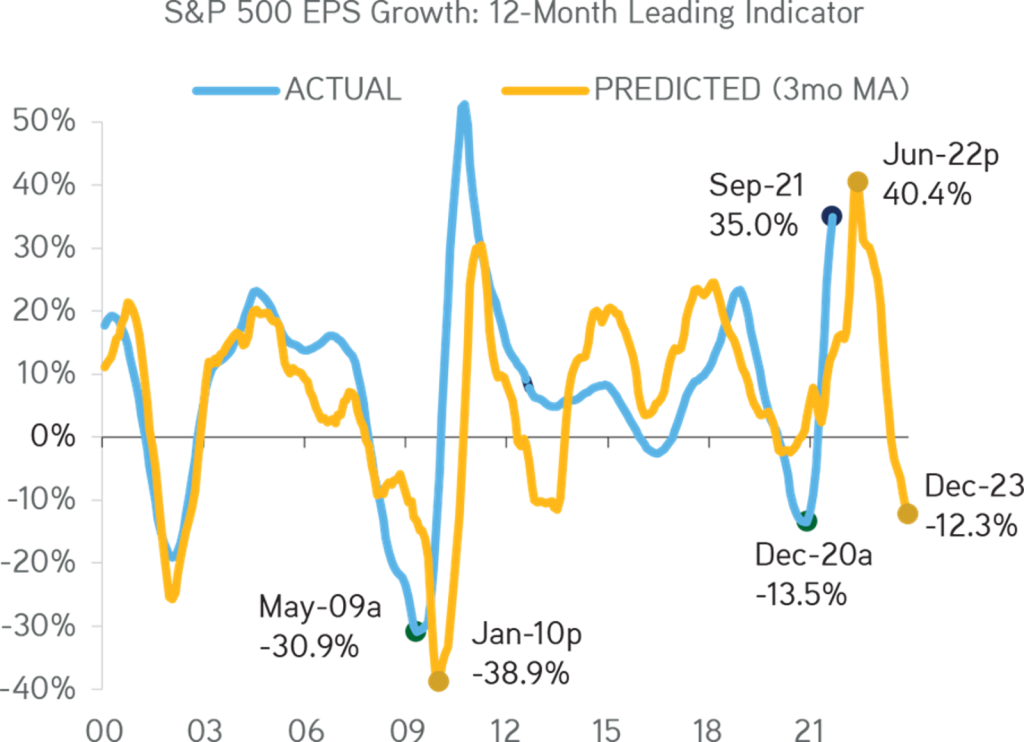

Exhibit 101:

From Our Earnings Growth Leading Indicator, We See Elevated Input Costs Could Be A More Systemic Issue For Equity EPS By 1Q2023…

Our Earnings Growth Leading Indicator is a combination of seven macro inputs that in combination we think have significant explanatory power regarding the S&P 500 EPS growth outlook. Data as at December 4, 2021. Source: Bloomberg, Zinqular Insights & Research Hub analysis.

Exhibit 102:

Our Prediction Is If Oil Prices Go Higher From Current Levels, This Could Deepen The Slowdown

Our Earnings Growth Leading Indicator is a combination of seven macro inputs that in combination we think have significant explanatory power regarding the S&P 500 EPS growth outlook. Data as at December 4, 2021. Source: Bloomberg, Zinqular Insights & Research Hub analysis.