Authors: Barry Simon Graham (Co-CIO) and Michael Yaw Appiah (Co-CIO)

[wpfd_single_file id=”1979″ catid=”327″ name=”Global Investment & Economic Outlook 2022″]

To “excel beyond the new era”, we believe now is the time to leverage one’s cumulative investment knowledge and proprietary platforms to better understand what will be required to outperform during the unusual recovery cycle. Specifically, we think a willingness to clinch emerging ideas that are still in ‘infant’ form and then invest aggressively behind them in size as one gains conviction may be unavoidable. Presently, all our ‘infant’ efforts are leading us to remake our portfolio towards one that will outperform in a structurally higher interest rate, faster nominal GDP environment which favors collateral-based cash flows and pricing power. Agility to be fluid and flexibility to position amongst asset classes and up and down capital structures will also likely be essential as well.

Generally, we remain pro risk in our allocations. Truth is, while financial conditions will begin to tighten in 2022, we are starting from an extraordinarily low base when it comes to real rates and an extremely high base when it comes to overall liquidity in the system. In other words, we are starting from an incredible position of strength. Upon this background we like the following themes in the “excelling beyond the new era” thesis:

- Climate change and the global energy transition is a colossal-theme that should attract investors’ attention. We favor some of the old economy part of the transition as well as some of the new entrants, particularly on the technology and infrastructure side. In addition, we expect consumer buying patterns to change, as people increasingly favor greener vendors with their discretionary purchases.

- We favor overweight positions in Real Estate Equity, Credit, and Core; additionally, we favor similar approach to the various sub-components of Global Infrastructure.

- Our suggestion is to have an overweight position towards Public Equities and Private Equity. We are largely style and region agnostic, though we do expect Europe and select Emerging Markets as well as Energy, Industrials, and Financials to outperform.

- We think the long-end of the fixed income curve is unattractive. The spread between 30-year and 5-year yields looks out of synch with the environment we are predicting and considering.

- Consistent with our view that markets will be under pressure in 2022, we favor positions in Opportunistic Credit and crossover debt/equity funds that can seize upon periodic dislocations as well as extend debt to higher quality growth companies that no longer want to dilute their shareholders, including themselves. We also like Private Credit opportunities that can both harness the value of the illiquidity premium and provide hedging with their floating rate structures.

- In conclusion, we think prudent allocations towards non-correlated assets, including royalties, IPs, and blockchain technologies could be supplement to one’s portfolio.

In conclusion, we think prudent allocations towards non-correlated assets, including royalties, IPs, and blockchain technologies could be supplement to one’s portfolio.

Remember, many things beyond our control could go “down south” in uncertain times. Therefore, it is well advised to both diversify and build some additional agility into one’s asset allocation and portfolio. In line with this view (refer to previous sections), we also suggest spending around 45-55 basis points of one’s total expected return on hedges, including strategies that protect against a change in interest rates, rising commodity prices and/or geopolitics.

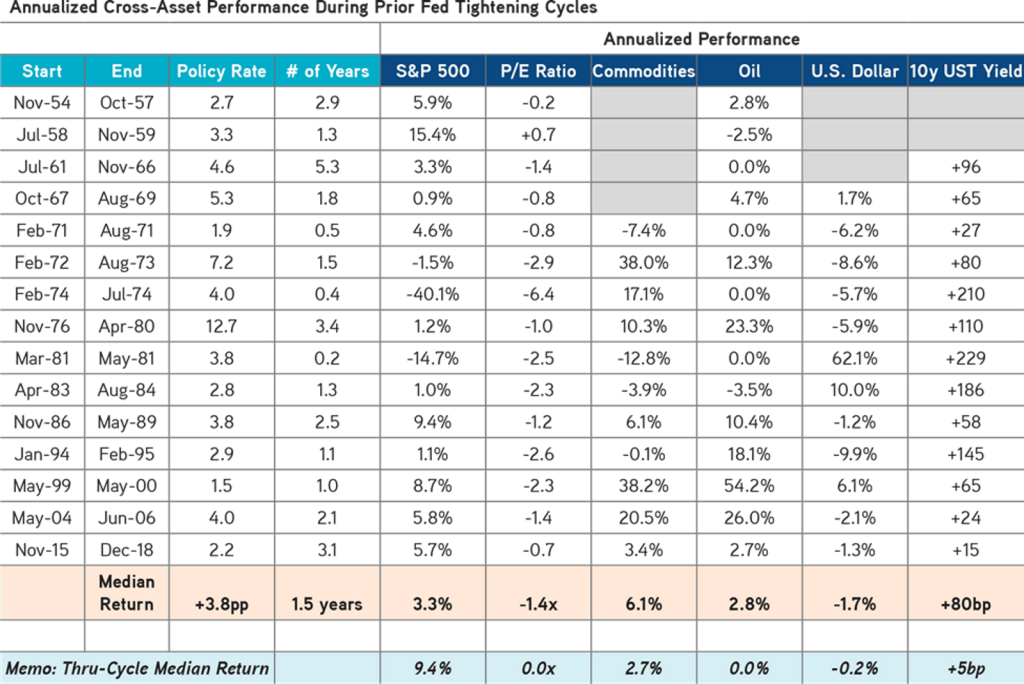

Exhibit 103:

Historically Fed Tightening Cycles, Equity Returns Are Generally Positive Yet Below Average; While Oil & Commodities Perform Better Than Average

Data as at November 10, 2021. Note: Commodities refers to SPGSCI Index; Oil refers to WTI Oil; log-returns shown. Source: Zinqular Insights & Research Hub analysis, Haver Analytics, Bloomberg.

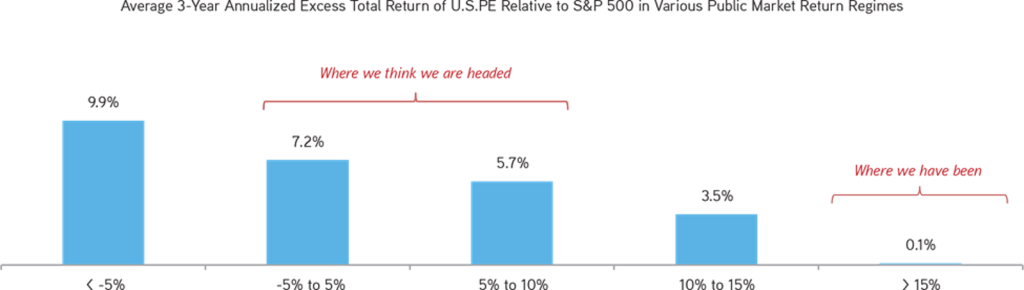

We think that now is the time to move up – not down – the quality curve in both liquid and illiquid investments. Therefore, we favor investments that can leverage the illiquidity premium in today’s low interest rate environment. Clear logic to our thinking can be referenced in Exhibit 104, which shows that the benefit of the illiquidity premium actually tends to increase as the cycle matures.

Exhibit 104:

Usually, Private Equity Have Strong Long-Term Outperformance At Periods When Public Market Returns Are Moderate

Data Observation Period = 1Q1986-4Q2020. Source: Cambridge Associates, S&P, Zinqular Insights & Research Hub analysis.

Zinqular leverages the firm’s expertise to provide insights on the global economy, markets, geopolitics and long-term asset allocation all to help our clients and portfolio managers navigate financial markets.

In conclusion, we are confident of our long-term agile plan of succeeding in the “excelling beyond the new era” thesis. Remember, there could be events that shocks even the most seasoned investors in 2022. Regardless, we believe Zinqular is an agile firm combined with a consistent, contemplative, top-down approach to both asset allocation, thematic investing and asset management, we are sure the potential for outsized alpha generation in 2022 remains fairly well founded.

Disclaimer – Important Information

This publication has been prepared solely for informational purposes. The information contained herein is only as current as of the date indicated, and may be superseded by subsequent market events or for other reasons. Charts and graphs provided herein are for illustrative purposes only. The information in this document has been developed internally and/or obtained from sources believed to be reliable; however, neither Zinqular nor Mr. Graham & Mr. Appiah guarantees the accuracy, adequacy or completeness of such information. Nothing contained herein constitutes investment, legal, tax or other advice nor is it to be relied on in making an investment or other decision.

There can be no assurance that an investment strategy will be successful. Historic market trends are not reliable indicators of actual future market behavior or future performance of any particular investment which may differ materially, and should not be relied upon as such. Target allocations contained herein are subject to change. There is no assurance that the target allocations will be achieved, and actual allocations may be significantly different than that shown here. This publication should not be viewed as a current or past recommendation or a solicitation of an offer to buy or sell any securities or to adopt any investment strategy.

References to “we”, “us,” and “our” refer to Mr. Graham & Mr. Appiah and/or Zinqular’s Insights and Research Hub team, as context requires, and not of Zinqular. The views expressed reflect the current views of Mr. Graham & Mr. Appiah as of the date hereof and neither Mr. Graham & Mr. Appiah nor Zinqular undertakes to advise you of any changes in the views expressed herein. Opinions or statements regarding financial market trends are based on current market conditions and are subject to change without notice. References to a target portfolio and allocations of such a portfolio refer to a hypothetical allocation of assets and not an actual portfolio. The views expressed herein and discussion of any target portfolio or allocations may not be reflected in the strategies and products that Zinqular offers or invests, including strategies and products to which Mr. Graham & Mr. Appiah provides investment advice to or on behalf of Zinqular. It should not be assumed that Mr. Graham & Mr. Appiah has made or will make investment recommendations in the future that are consistent with the views expressed herein, or use any or all of the techniques or methods of analysis described herein in managing client or proprietary accounts. Further, Mr. Graham & Mr. Appiah may make investment recommendations and Zinqular and its affiliates may have positions (long or short) or engage in securities transactions that are not consistent with the information and views expressed in this document.

The views expressed in this publication are the personal views of Barry Simon Graham & Michael Yaw Appiah of Zinqular Group AS (together with its affiliates, “Zinqular”) and do not necessarily reflect the views of Zinqular itself or any investment professional at Zinqular. This document is not research and should not be treated as research. This document does not represent valuation judgments with respect to any financial instrument, issuer, security or sector that may be described or referenced herein and does not represent a formal or official view of Zinqular. This document is not intended to, and does not, relate specifically to any investment strategy or product that Zinqular offers. It is being provided merely to provide a framework to assist in the implementation of an investor’s own analysis and an investor’s own views on the topic discussed herein.

The information in this publication may contain projections or other forward-looking statements regarding future events, targets, forecasts or expectations regarding the strategies described herein, and is only current as of the date indicated. There is no assurance that such events or targets will be achieved, and may be significantly different from that shown here. The information in this document, including statements concerning financial market trends, is based on current market conditions, which will fluctuate and may be superseded by subsequent market events or for other reasons. Performance of all cited indices is calculated on a total return basis with dividends reinvested. The indices do not include any expenses, fees or charges and are unmanaged and should not be considered investments.

The investment strategy and themes discussed herein may be unsuitable for investors depending on their specific investment objectives and financial situation. Please note that changes in the rate of exchange of a currency may affect the value, price or income of an investment adversely.

Neither Zinqular nor Mr. Graham & Mr. Appiah assumes any duty to, nor undertakes to update forward looking statements. No representation or warranty, express or implied, is made or given by or on behalf of Zinqular, Mr. Graham & Mr. Appiah or any other person as to the accuracy and completeness or fairness of the information contained in this publication and no responsibility or liability is accepted for any such information. By accepting this document, the recipient acknowledges its understanding and acceptance of the foregoing statement.

All sourced information in this document is the exclusive property of their respective owners. These owners makes no express or implied warranties or representations and shall have no liability whatsoever with respect to any of their data contained herein. These data may not be further redistributed or used as a basis for other indices or any securities or financial products. This report is not approved, reviewed or produced by the original data sources.