Authors: Barry Simon Graham (Group Co-CIO) and Michael Yaw Appiah (Group Co-CIO)

For a few years now, we have asserted that we are witnessing the emergence of a new economic order. The period that comes closest to our current macro era within the last 400 years is the late 19th century, roughly from the 1870s to 1914, often referred to as the Second Industrial Revolution or the Gilded Age; and/or the post-World War II era (particularly the period between 1945 and the early 1970s). These periods bear striking similarities to our current economic climate of Rapid technological advancement; Global economic growth & expansion; Coordinated (though less formalized) global monetary policy; Inflationary pressures; Geopolitical tensions & conflicts; and Huge explosion of government debt, deficit & spending.

These eras are marked by transformative technological shifts. Today, it’s the digital revolution, artificial intelligence (AI), biotechnology, and renewable energy. These rapid technological advancements led and/or will lead to significant increases in productivity, new industries emerging, and disruption to existing economic structures.

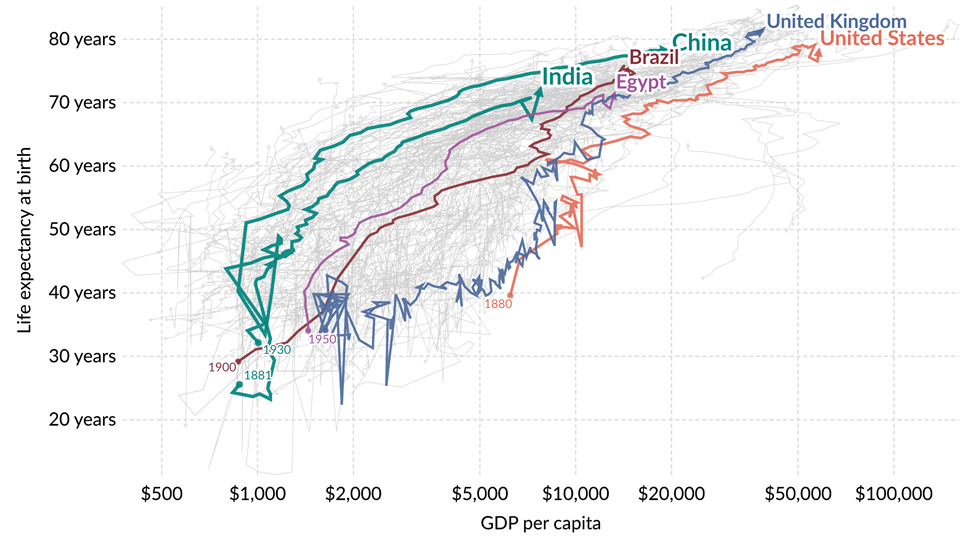

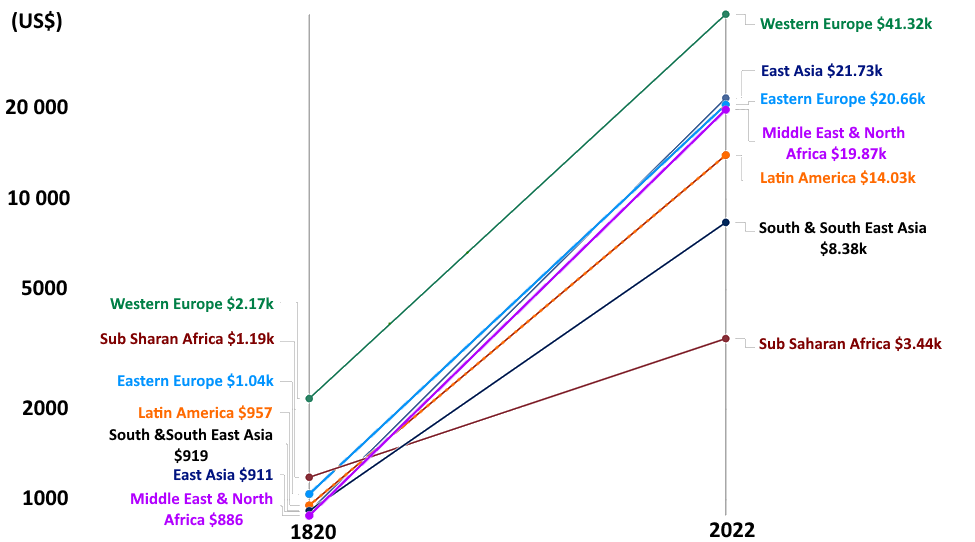

Global healthcare innovations have vastly improved quality of life, and emerging economies are witnessing sharp increases in life expectancy and GDP per capita (Exhibit 1A, 1B).

Across the globe, demographic transformations and rising political dissatisfaction are reshaping societies, with digitally “native” citizens leading a ‘revolt of the public’ against traditional institutions. For individuals outside the equity or housing markets, the chasm between wealth and poverty has reached historic extremes. Concurrently, the lines between economic stability and national security are increasingly blurred, reflecting the shift from a harmonious globalized world to one of escalating geopolitical rivalries.

For a few years now, we have asserted that we are witnessing the emergence of a new economic order. The period that comes closest to our current macro era within the last 400 years is the late 19th century, roughly from the 1870s to 1914, often referred to as the Second Industrial Revolution..

– Barry Simon Graham (Group Co-CIO)

Amidst the challenging economic currents, our investment outlook for 2025 remains resilient; “thriving amidst change – tapping the strength of upward currents”. Echoing the sentiment of our 2024 refrain, ‘the sunny side of shifting currents,‘ we maintain a positive stance. While investors should prepare for lower returns and heightened volatility compared to 2024, key drivers like accommodative financial conditions, slow but steady U.S. productivity, robust earnings growth, limited net supply of securities and steady rise of global liquidity bolster our belief that the cycle is far from over, and opportunities for gains remain viable.

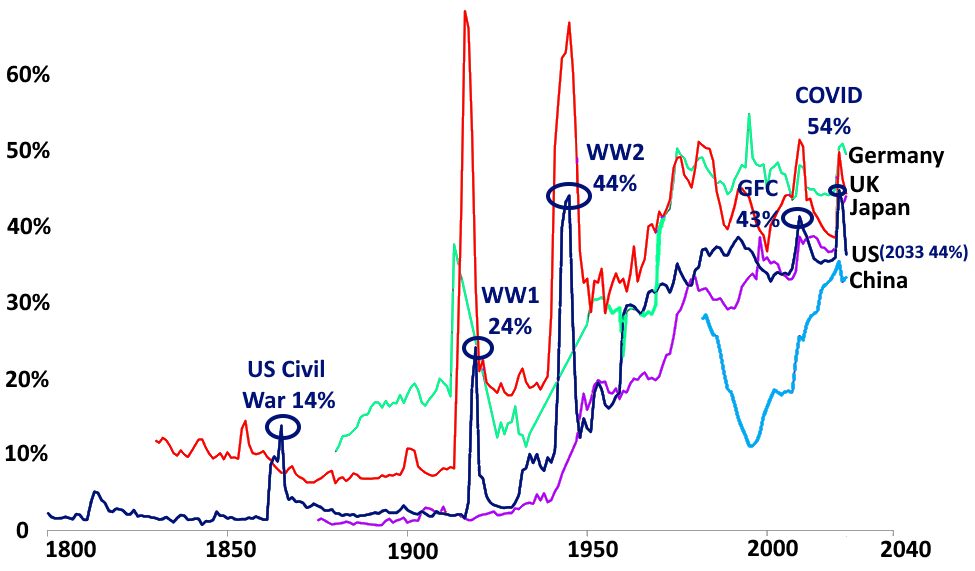

Government spending is an important instrument for reducing inequality. While not on the same scale as today, government spending and debt levels were rising in many countries during the late 19th century, driven by factors like military expenditures, infrastructure development, and social programs. This mirrors the current situation with high government deficits in many nations, driven by factors like bailout for giant global financial institutions in 2008/9, pandemic-related spending, stimulus measures, and ongoing social programs (Exhibit 2).

Exhibit 1A: Life Expectancy vs. GDP per Capita; Adjusted for Inflation & Cost of Living, 1543 to 2022

Exhibit 1B: GDP per Capita; Adjusted for Inflation & Cost of Living 1820 to 2022

Exhibit 2: Government Spending as a Share of GDP Continuous to Rise Unsustainably, 1800 to 2023.

Decoding The Trend & Vital Cornerstones

Historically, economies have followed predictable, long-term trends. Investors could rely on these patterns, focusing mainly on managing short-term fluctuations, with confidence that growth would eventually revert to its baseline. This principle has been a cornerstone of traditional investment strategies.

We see the current environment as fundamentally different. Economic transformation is now reshaping long-term trends, making outcomes more varied and unpredictable. What’s causing this transformation? Vital cornerstones like demographics, localization, AI, energy transition, etc. are rewriting the rules of economic progress.

Geopolitical fragmentation is fundamentally altering trade flows and supply chains. New trading alliances and protectionist measures are disrupting global trade, potentially reducing its efficiency and reshaping the way economies operate. In parallel, the energy transition—closely tied to forces like AI and geopolitical shifts—is driving transformative innovation and investment. The digitization of finance is also revolutionizing economic activity, reshaping how households and businesses handle money, from borrowing to transactions and investments.

Demographic changes, particularly aging populations, are tightening labor supply and could limit economic growth unless Industrial automation and AI-driven productivity gains offset these constraints. While rising immigration has provided some relief in recent years, particularly in the U.S., its impact is likely to be temporary. Consequently, the economic and social advantages the U.S. derives from immigration may further be eroded by the possibility of widespread deportations of immigrants under current political circumstances.

All of this underscores our belief that the data reflects shifting long-term trends rather than typical business cycles. Economic surprises increasingly reveal structural changes that suggest new, enduring trajectories.

Moreover, several vital investment cornerstones requiring tens of trillions of dollars pool of private capital over 3 to 5 decades present compelling avenues for above-average returns under our “New Economic Order – Outlook 2022” macro framework.

We see the current environment as fundamentally different. Economic transformation is now reshaping long-term trends, making outcomes more varied and unpredictable. What’s causing this transformation? Vital cornerstones like demographics, localization, AI, energy transition, etc. are rewriting the rules of economic progress.

– Michael Yaw Appiah (Group Co-CIO)

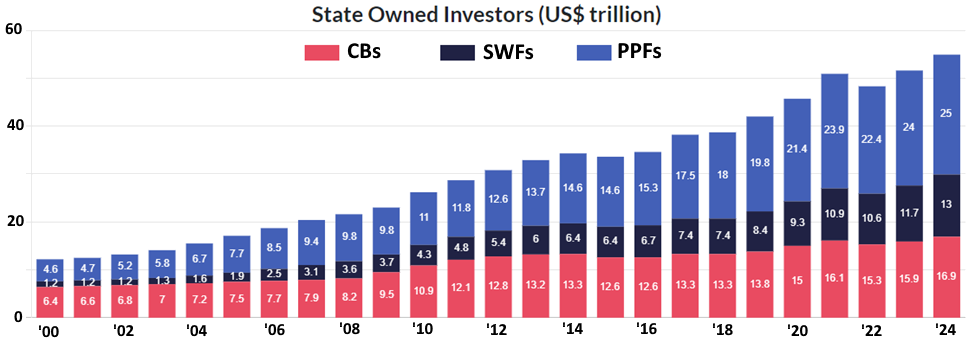

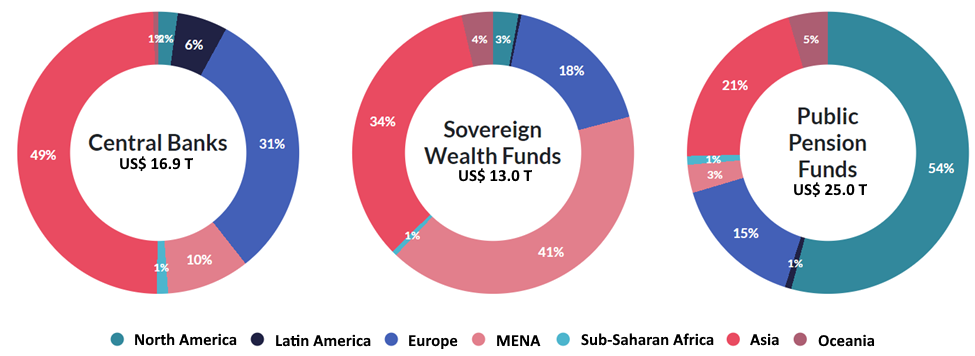

It has been relatively a good year for State-Owned Investment entities. In 2024, State-Owned Investors (SOIs) – specifically Central Banks (CBs), Sovereign Wealth Funds (SWFs), and Public Pension Funds (PPFs) – witnessed growth in their assets (i.e., assets under management (AUM)). This surge, driven by robust returns in financial markets, particularly from public equity investments in large-cap tech and AI firms within the S&P 500, propelled their combined AUM to a record high of $54.9 trillion, representing a 6% YoY increase.

Notably, worldwide CB assets expanded to $16.9 trillion albeit coordinated monetary easing measures, while SWFs reached a peak of $13 trillion. PPFs also saw significant growth, reaching $25 trillion. While continued growth is expected in 2025, the pace is likely to moderate, presenting both opportunities and challenges for these SOIs (Exhibit 3A, 3B).

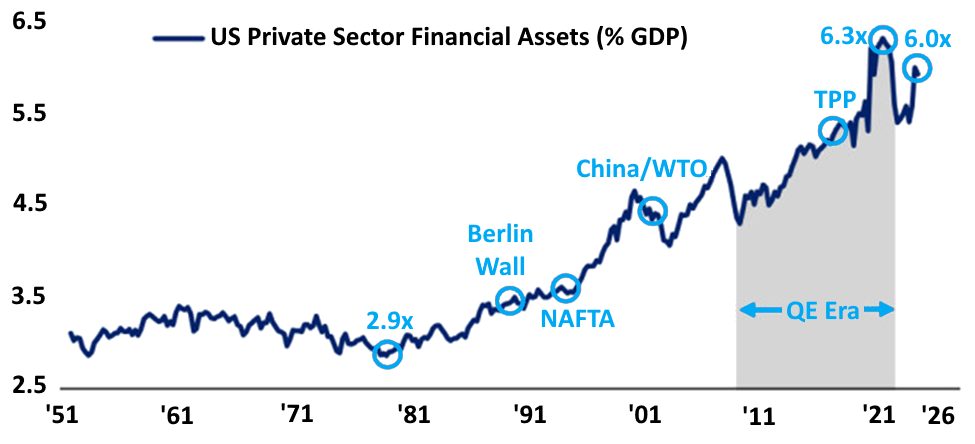

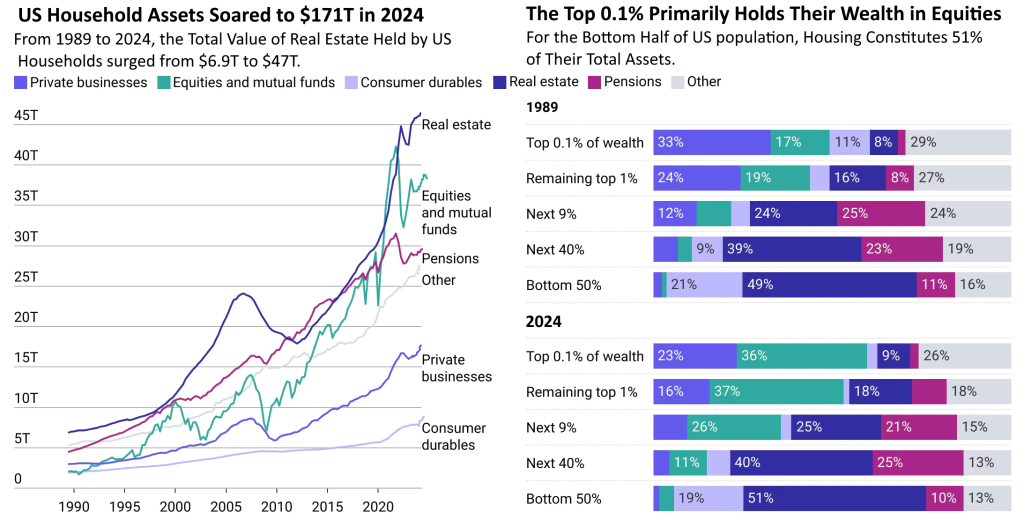

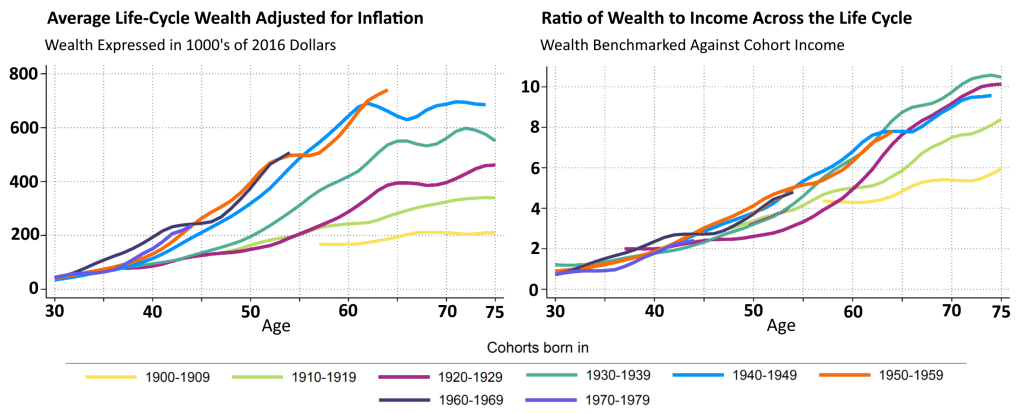

Asset prices have also risen sharply, benefiting investors who prioritized S&P 500 exposure. Is the combined value of “Wall Street” greater than “Main Street”? Absolutely. The “Wall Street” value that encompasses all financial assets except real estate, including cash deposits, loans, private equity, pension fund reserves, stocks, and bonds. Its value currently approaches the all-time high ratio of 6.3 times US GDP reached in June 2021. This steady rise since the 1990s reflects the financialization of the US economy and its significant wealth inequality, as noted by Zinqular Insights team (Exhibit 4). In 3rd quarter of 2024, the Federal Reserve revealed U.S. household net worth had reached an all-time high of approx. $170 trillion, driven by strong performance in housing and stocks; added $3.8 trillion to Americans’ equity holdings. By many indicators, we’re living in an era of unprecedented wealth and progress for the top 10% of the population (Exhibit 5A, 5B, 5C).

Despite appearances of overall economic well-being, a closer look reveals significant imbalances. Over the last four decades, the wealth-to-income ratios in wealthy nations have grown substantially, coinciding with sharp increases in housing and equity values. These dynamics are frequently linked to persistently low interest rates, declining shares of labor income, and the evolving financial behaviors of successive generations. Long-term quantitative easing has disproportionately benefited older generations (55+), who now control 70% of total household assets in the U.S., a substantial increase from 50% in 2001.

This demonstrates the significant impact of asset price appreciation on this demographic. Equity market performance exhibits a pronounced “day and night” divide, with the S&P 500 significantly outperforming international peers to a greater extent than during the Nifty Fifty (1970’s) or Dot-com (2000’s) periods. This outperformance, however, benefits a limited segment of the population. In the U.S., for example, only 22% of households owned stocks directly in 2022, highlighting the limited participation in the equity market.

Zinqular internal data paints a concerning picture of wealth inequality. While the average cash balances for the bank’s entire customer base have increased by 32% since 2019, with the wealthiest clients experiencing even greater gains, consumers with the lowest balances have seen a 7% decline. These exhibits highlight the growing concentration of wealth in the hands of a small segment of the global population.

Exhibit 3A: Growth in State Owned Investors Assets

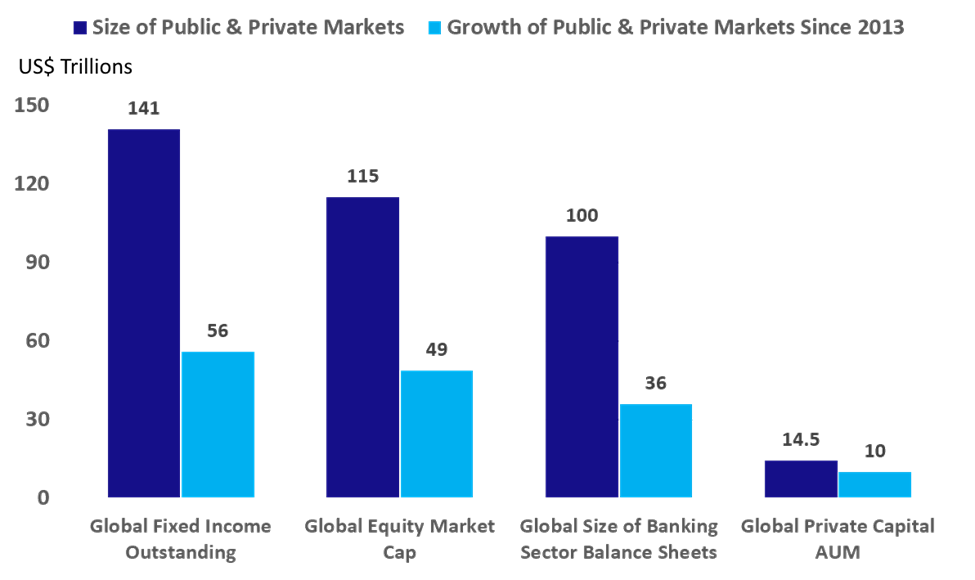

Exhibit 3B: Comparing a Decade of Growth in Public and Private Markets. Contrasting the Expansion of Public and Private Markets Since 2013

Exhibit 4: US Private Sector Financial Assets as a % of US GDP

Exhibit 5A. In 2024, Total US Household Assets Surged to $171T, With the Top 0.1% of Concentrating Their Wealth Primarily in Equities.

Exhibit 5B: Older Generations (55+), Now Control 70% of Total Household Assets in the U.S., An Increase From 50% in 2001.

Exhibit 5C: US Equities Have Outperformed Non-US Equities; No Rotation From US to International Equities

Essential 2025 Takeaways at a Glance

“NEW ERA” THESIS STRONG

“New Economic Era” Proposition Remains Strong: Implications for Investment Landscape.

2024 saw major election results that solidified the contours of our “New Economic Era” framework. This era is defined by higher deficits, increased geopolitical risks, a complex energy transition, and persistent inflation in the United States and rest of the world (RoW). Moreover, there is a growing emphasis on job protection, suggesting a less aggressive approach to combating inflation in 2025. Our top-down analysis indicates that these factors will likely lead to lower returns for investors, necessitating a fundamental reassessment of capital allocation strategies.

UNEVEN ECONOMIC REBOUND

Monetary Policy Divergence and Global Imbalances.

The global economy is navigating uncharted waters, characterized by unprecedented monetary policy divergence. The ECB is cutting rates ahead of the Fed, a departure from historical precedent. Meanwhile, the Bank of Japan is raising rates, while China confronts deflationary pressures and a major deleveraging cycle. These divergent paths, coupled with the surprising shift in bond markets – where Japan’s 30-year bond yields now exceed China’s and Greece’s bond yields are approaching parity with France’s – create a complex and uncertain environment for global markets (Exhibit 6).

CHANGING TERRAIN

The Evolving Landscape: Earnings Growth Takes Center Stage.

The landscape for investment success is evolving. More aggressive GDP and EPS growth estimates for the U.S. at the start of 2025 will make achieving “upside surprises” more challenging. This Fed cycle is expected to be less dovish than previous ones. Consequently, we favor large domestic-oriented economies like the U.S. and India, service-based economies like Spain, and countries actively pursuing corporate reforms, such as Japan. In this context, we believe that earnings growth will be a more critical factor for investment success than multiple expansion.

BEYOND YIELD CURVE FACTOR

Exploring Beyond the Yield Curve: Currency Volatility as the Unseen Risk.

While the market’s attention is currently focused on the surge in 10-year Treasury yields, we believe currency volatility deserves greater scrutiny. Trade wars and widening fiscal imbalances can create significant currency shocks, presenting a unique set of risks compared to previous market cycles.

COMMODITIES NEAR-TERM CAUTION

Commodities Specifically The Oil Market: Near-Term Caution, Long-Term Confidence.

The oil market landscape is evolving. Our near-term oil price forecasts for 2025-26, at $66-$70 per barrel, have been revised downward and now lie below current futures prices. However, our long-term outlook remains bullish, with 2027-28 estimates ranging from $75-$80 per barrel, significantly exceeding current futures prices of around $64 per barrel. Importantly, as AI technologies continue to scale, we believe energy security will become even more critical for national security. For further insights, please refer to our Key Themes section.

LABOR & PRODUCTIVITY PARADOX

The Productivity Paradox: Fueling Growth, Hiding Underlying Risks.

The U.S. economy is currently riding a wave of strong productivity growth, which is supporting robust earnings and economic expansion. While this positive momentum is likely to continue in the near term, it is crucial to recognize the potential risks associated with a future productivity slowdown. We believe such a slowdown could trigger a faster and more significant economic downturn than the market currently anticipates.

EMERGING ENGINES

Emerging Engines of Growth in a Rising Global Rivalries.

We anticipate a new era of investment characterized by a growing convergence of economic and national security considerations. This will likely necessitate political leaders to explore innovative strategies to stimulate domestic investment, including measures to increase national savings, encourage private sector involvement, and reduce the cost of capital. This evolving landscape will likely witness the emergence of key growth markets in India, the Middle East, and Southeast Asia. As a result, we expect Intra-Asia trade to continue its robust growth trajectory, further reinforcing the region’s economic and geopolitical influence.

Exhibit 6: Global Economic Growth Will Be Uneven in 2025

Europe is facing significant economic headwinds. Germany is experiencing a sharp economic slowdown, while bond markets in the U.K. and France are exerting pressure on governments to curb spending. These fiscal battles have even led to the collapse of governments and triggered elections in both countries. Meanwhile, China’s economic landscape is also undergoing a critical transformation. As China shifts its manufacturing focus from consumer goods to industrial automation and the green economy, companies heavily invested in traditional manufacturing sectors are facing significant challenges, reminiscent of the difficulties experienced by U.S. and European manufacturers at the beginning of the century. While this shift may lead to deflationary pressures, the potential for a recession remains a concern.

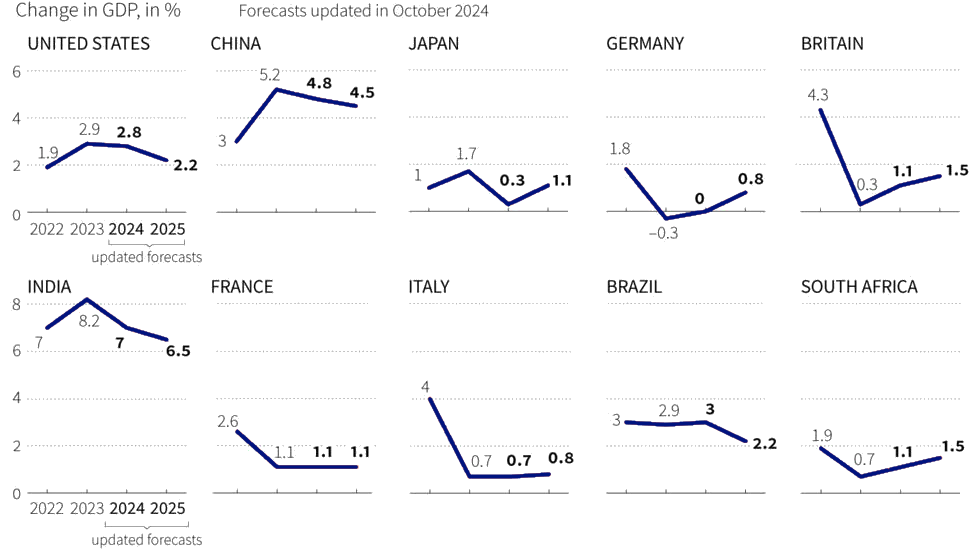

The “day and night” narratives are mirrored in our macroeconomic data, reinforcing our thesis of an uneven and asynchronous global recovery characterized by rolling recoveries and recessions across economies. Reviewing the data, we forecast uneven global growth in 2025. Our U.S. GDP forecast is raised to 2.2%, exceeding the consensus of 2.1%, while our China forecast is kept at 4.5%, in line with the consensus of 4.5%. For Europe, we maintain our forecast of 0.8%, 40 basis points below consensus. This divergence highlights a bifurcated global outlook, with domestic-led economies like the U.S. and India outperforming traditional export nations.

Despite widespread concerns, we have consistently maintained a cautiously optimistic outlook for global capital markets, particularly following the S&P 500’s 25% correction in 2022. This perspective has evolved from our cautious ‘ Excelling Beyond the New Era” – Outlook in 2022, a year characterized by rising interest rates and market volatility, to a more optimistic Going Back to Basics’ message in 2023 and a “Sunny Side of Shifting Currents” approach in 2024.

While we acknowledge the potential for challenges, we maintain a cautiously optimistic outlook for 2025, encapsulated in our ” Thriving Amid Change: Tapping the Strength of Upward Ocean Currents” thesis. However, it’s important to note that higher valuations, increased investor optimism, and rising earnings estimates may lead to more modest returns compared to the exceptional performance witnessed in 2023 and 2024. There will be growth but not so high. Despite these potential headwinds, we remain positive on risk assets in 2025 for the following five reasons:

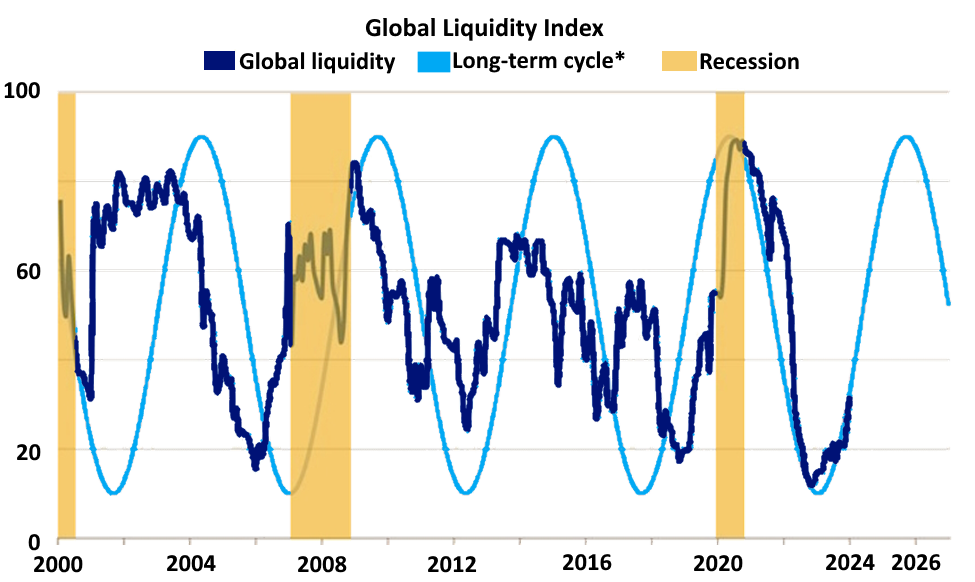

##1: Ample global liquidity stands out as a crucial driver of growth in 2025, in our view. Global Liquidity Index (i.e., a measure of overall liquidity conditions in the global financial system) appears to be on a steady rise. This upswing in available cash follows a familiar pattern. Roughly every 5 to 6 years, we see a tidal wave of liquidity followed by a receding tide (Exhibit 7A).

Since 2000, the index shows several cycles of expansion and contraction. The dot-com bubble burst, the 2008 financial crisis, and the COVID-19 pandemic all coincided with significant liquidity contractions. Currently, we’re riding a rising tide that could potentially peak around 2026. The increase in global liquidity generally signals easier access to capital; but the “higher for longer interest rate” regime are dampening the excitement; making borrowing costs less attractive. Increasing global liquidity often leads to inflationary pressures as more money chases the same amount of goods and services.

Sectors such as technology, consumer discretionary, and financials typically benefit from rising global liquidity as consumer spending and investment increase. Real assets like real estate and commodities might also see increased demand as investors seek inflation protection amidst rising liquidity.

Exhibit 7: Global Liquidity is Increasing Suggesting More Favorable Environment for Economic Activity in the Near Term.

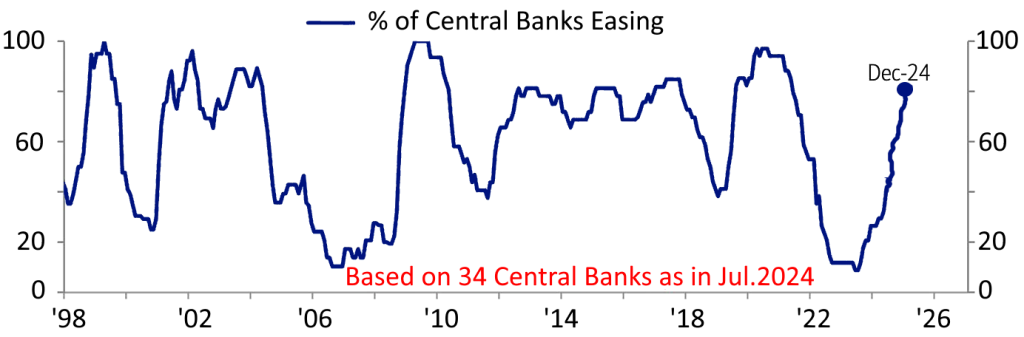

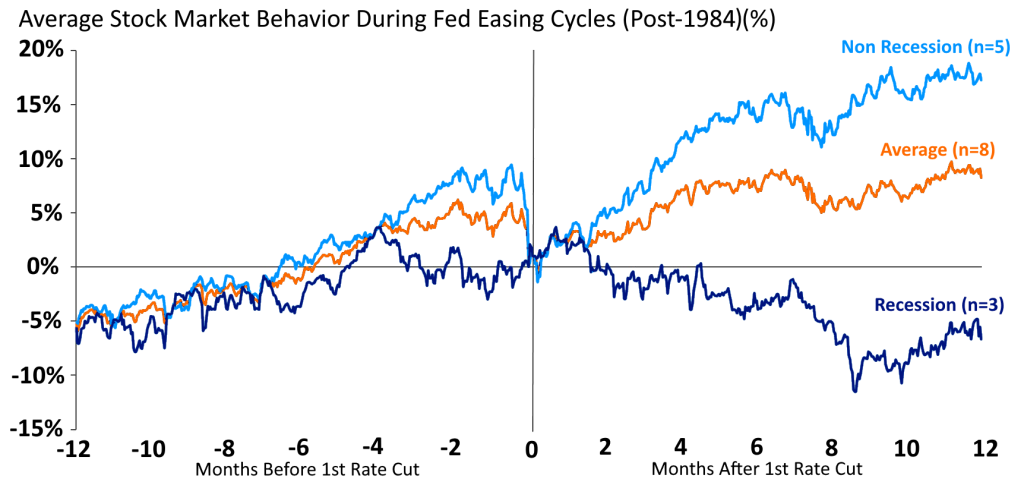

##2: Typically, easing by central banks is beneficial for markets, provided a recession is not in play. Exhibit 8 demonstrates how global central bank policies are transitioning from tightening to easing (albeit slower in some cases for others). While the U.S. Federal Reserve is not in aggressive easing mode, improving interest rate dynamics in China and Europe paint a positive picture. This setup typically favors risk assets. Absent a recession—which we do not anticipate, especially in a higher nominal GDP environment under new United States political administration—markets often move higher, as illustrated in Exhibit 9, 10.

We acknowledge that market performance has exceeded expectations. While historically not unprecedented, the S&P 500’s strong performance suggests that future gains may be more moderate, particularly given our expectation of limited multiple expansion in 2025. This implies a higher hurdle for achieving significant market returns going forward.

Exhibit 8: More Than 80% of Global Central Banks are Easing Monetary Policy Suggests a Positive Outlook for the Global Economy.

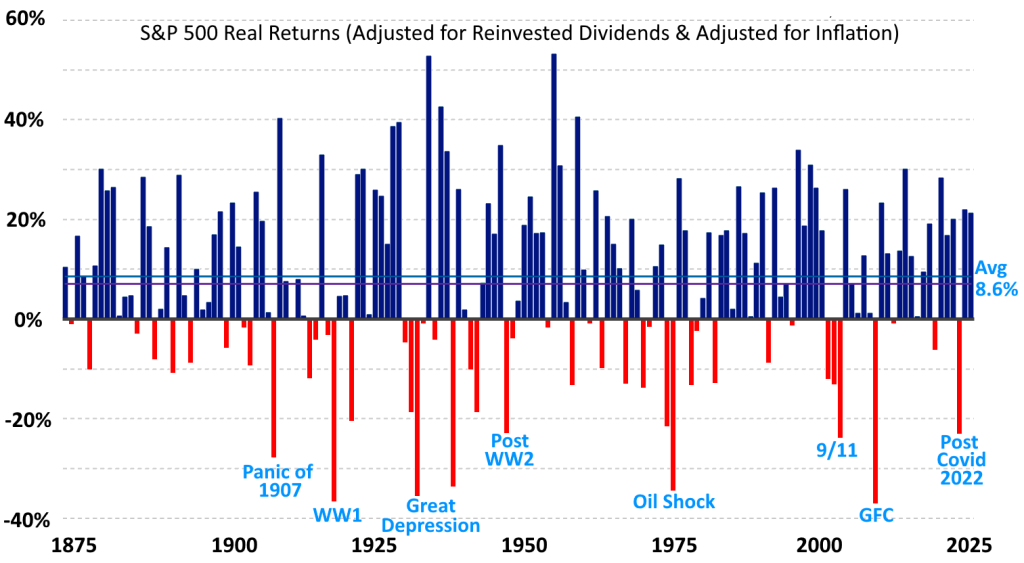

Exhibit 9: Long-Term S&P 500 Market Index Returns (1872-2024).

Exhibit 10: The S&P 500 Outperforms When the Fed Cuts Rates in a Non-recessionary Environment

##3 While market conversations are dominated by fundamental factors like earnings and GDP growth, the significant impact of positive market technical on risk asset performance since COVID cannot be ignored. This favorable technical backdrop, driven by coordinated central bank easing and a notable lack of supply, remains a key factor. Four options support this narrative:

1st: Exhibit 11 reveals a significant decline in net issuance, measured as total proceeds from IPOs, Levered Loans, and High Yield issuance as a percentage of GDP, from a peak of 7.1% in summer 2021 to 2.7% currently.

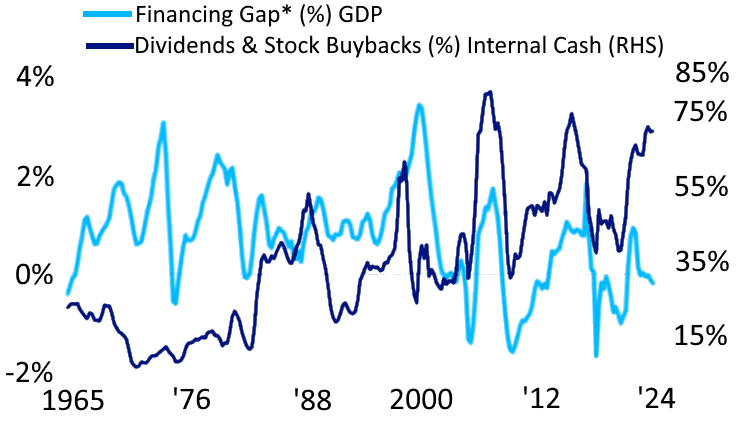

2nd: In contrast, Exhibit 12 indicates that U.S. buybacks are poised for continued strength in 2025. Over the past decade, net buybacks have contributed approximately one percent to earnings per share annually. Looking ahead, we anticipate a 17% year-over-year increase in gross buybacks in 2025, reaching an estimated $1.3 trillion. Data suggest 70% share of internal cash being used by companies on dividend and stock buybacks. It also shows the “financing gap” between capital expenditures and internal cash turning negative, “not surprising given the shift to use productive capacity outside the US and, in turn, earn the wide margin” over the past quarter-century.

3rd, money market balances have surged to $6.5 trillion, with declining global interest rates, we believe individual savers will seek higher-yielding investments, including Alternatives.

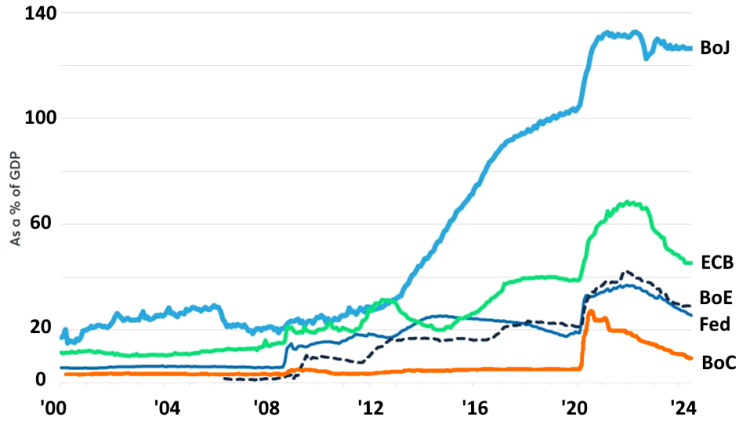

Finally, while central bank balance sheets have contracted from pandemic peaks, they remain significant compared to pre-COVID levels (Exhibit 13).

Ample global liquidity stands out as a crucial driver of growth in 2025, in our view. Global Liquidity Index (i.e., a measure of overall liquidity conditions in the global financial system) appears to be on a steady rise.

– Michael Yaw Appiah (Group Co-CIO)

Exhibit 11: Capital Market Liquidity is Gradually Returning to Normal Levels

Exhibit 12: US Policymakers Face Challenges in Encouraging Firms to Prioritize Capital Investment Over Shareholder Payouts.

Notes: *Financing gap is Capex minus internal funds.

Exhibit 13: Major Central Banks (CB) Still Have Ample Liquidity. CB Total Assets (% GDP). BoJ Balance Sheet Reduction Lags Behind Peers

##4: In the U.S., productivity growth remains a critical engine for economic and earnings expansion. Potential shifts in US immigration policy may significantly impact the workforce and productivity. A potential outcome of stricter immigration enforcement could be the removal of a considerable portion of the current undocumented workforce. This could lead to potential labor shortage, stifled innovation tech ecosystem and disruption on local communities. If we are correct then US productivity could slow down GDP-per-employee by 1% in 2025 and 1.5% in 2026.

Our base case suggests productivity will gain traction in the latter half of this decade, with the pandemic accelerating reliance on automation and digital tools. We project GDP-per-employee to grow 1.7% in 2026 to 2030, exceeding the consensus estimate of 1.0%. Importantly, much of this surge in productivity predates the full integration of industrial automation and AI’s benefits. That said, we are now observing early advantages from AI at the portfolio company level, reinforcing our confidence in the productivity-driven GDP outlook. Notably, unlike the dotcom bubble, today’s key players have healthier balance sheets, reduced capital costs, and operate in more concentrated industries.

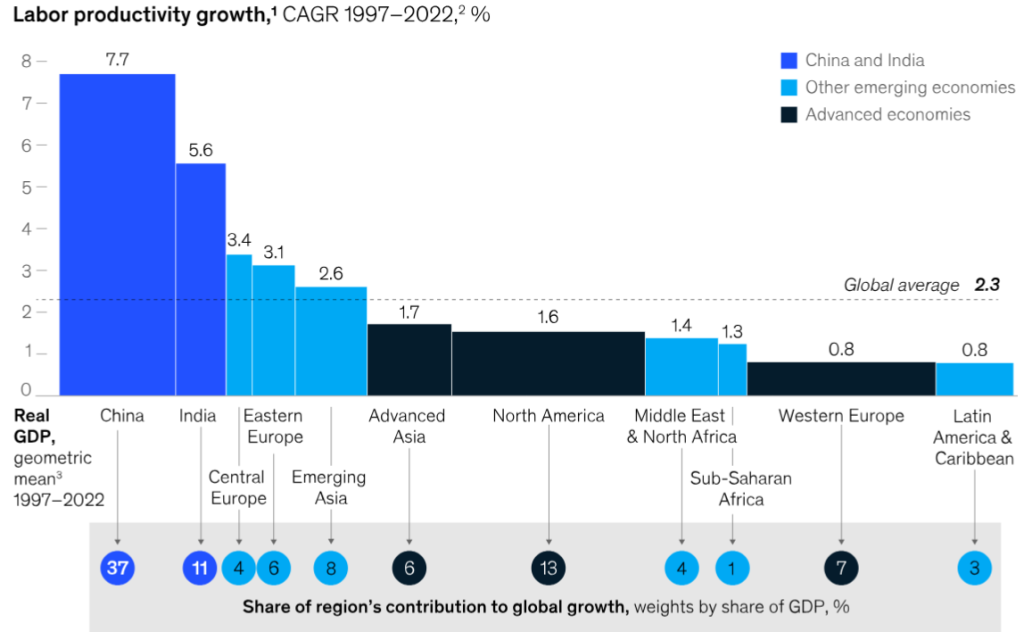

Global productivity has seen extraordinary growth over the past quarter century, increasing sixfold in median economies (Exhibit 14). Thirty emerging economies, representing 3.6 billion people, are on a fast track of progress. Maintaining this pace could allow them to match advanced-economy productivity within the next 25 years.

Exhibit 14: China & India Contributed 50% of Global Productivity Growth, While Emerging Economies Collectively Accounted For 75%.

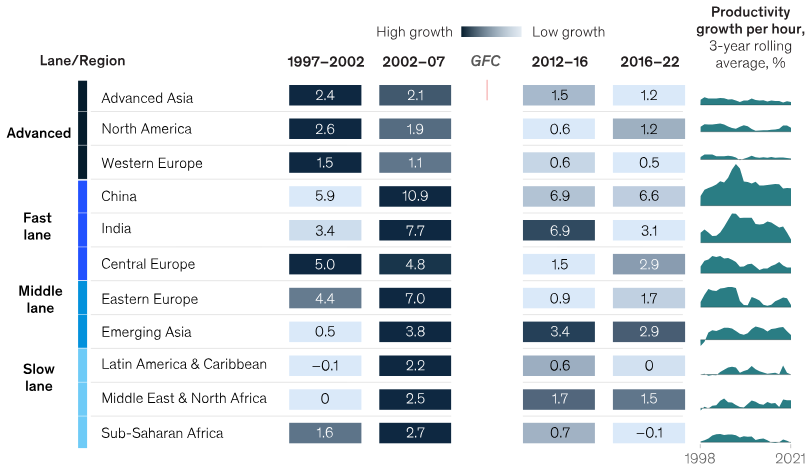

Despite this global transformation, productivity growth has stagnated in many economies. Since the global financial crisis (GFC), advanced economies have seen productivity growth decline by roughly one percentage point (Exhibit 15). Emerging economies in the ‘slow lane,’ home to 1.4 billion people, are progressing so slowly that they risk never closing the gap with advanced-economy productivity levels.

Advanced economies could boost their GDP per capita by 1,500 to 8,000 by 2030 by investing to restore pre-Global Financial Crisis (GFC) productivity growth. The slowdown in these economies occurred as two key drivers of productivity—manufacturing advancements fueled by Moore’s Law and offshoring—reached their limits. Post-GFC, investment plummeted and failed to produce new growth engines. However, targeted investments in digitization, automation, and artificial intelligence today could spark a new era of productivity gains.

For emerging economies, sustained investment is critical to staying in or reaching the ‘fast lane.’ Fast-lane economies, including China, India, parts of Central and Eastern Europe, and Emerging Asia, have consistently invested 20 to 40 percent of GDP. These investments have supported urbanization, enhanced service-sector productivity, and strengthened global manufacturing ties. Middle- and slow-lane economies have the potential to replicate this success by prioritizing similar strategies.

Exhibit 15: Following GFC, Productivity Decelerated in all Industries & Regions, With Advanced Economies Experienced Slowdown Even Earlier.

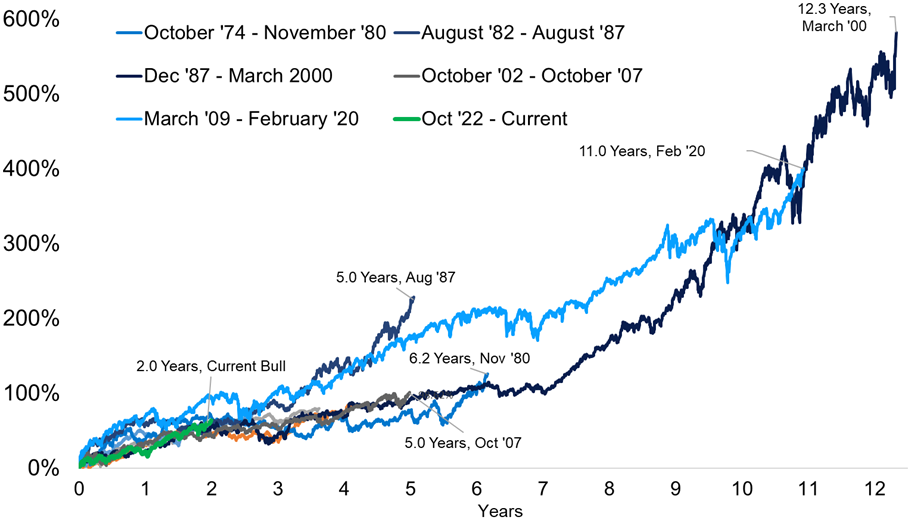

##5: The current bull market, while perhaps ahead of schedule in terms of appreciation, is still in its early stages at just 25 months. Exhibit 16A demonstrates this, with the current recovery period significantly shorter than the historical average of approximately 5 years. Moreover, we believe this bull market has the potential for sustained growth. Unlike previous cycles, we do not anticipate the need for significant consumer or corporate deleveraging, two key factors that have historically curtailed bull market cycles.

Exhibit 16A: Even After Two Years, A Bull Market May Still Have Significant Room To Run.

Notes: Bull markets over the last 50 years (since 1973) that survived beyond their second anniversary.

We continue to urge investors to re-evaluate their asset allocation strategies in light of the evolving economic landscape. Our ‘New Economic Order” proposition highlights three key factors: increased government deficits, heightened geopolitical risks, the complexities of the energy transition, and persistent inflation in the services sector. These factors, combined with elevated nominal GDP growth in the U.S., necessitate a departure from traditional investment approaches.

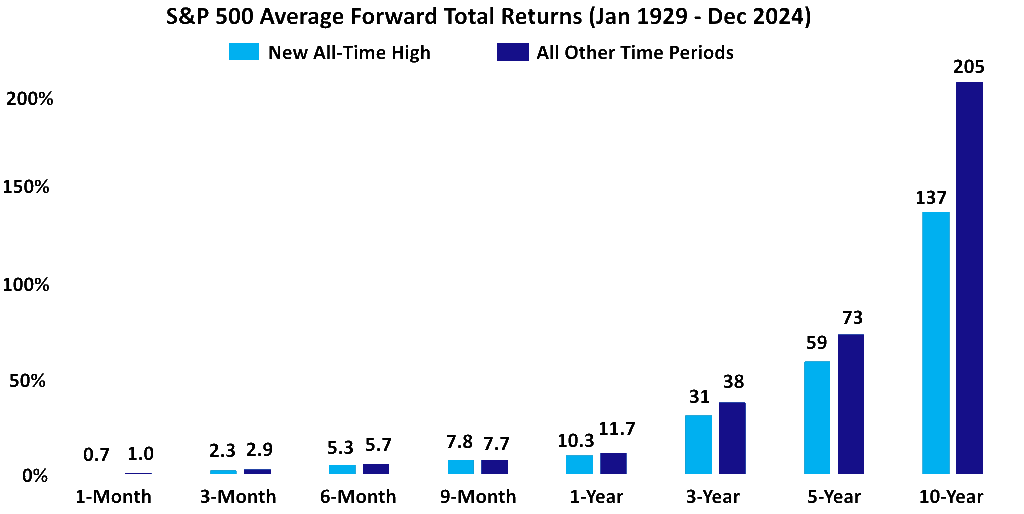

- Our insights hub team anticipate a less pronounced return dispersion across asset classes in the coming years, with the five-year forward median return forecast 200 basis points lower than the past five years. This suggests a flatter return landscape, where the distinction between top and bottom performers may diminish. Concurrently, traditional portfolio correlations are weakening, making asset allocation a more critical driver of portfolio volatility than individual asset risk. Our recommendation is to prioritize uncorrelated assets within portfolios, while also emphasizing the importance of rigorous manager selection, particularly within the Credit space. Additionally, investors should focus on long-term trends, as returns over 5+ years remain strong regardless of entry point (Exhibit 16B). Market corrections do not always signal poor long-term performance, reinforcing the importance of staying invested. Patience is key to capturing long-term gains: Staying invested for longer durations allows investors to potentially ride out market volatility and achieve substantial returns.

- To enhance portfolio resilience in the current inflationary environment, we advocate for increased exposure to assets linked to nominal GDP growth. Recognizing the potential for persistent inflation and a shift in the Fed’s focus towards job creation in 2025, we believe the following strategies are prudent: a) Overweighting modestly leveraged infrastructure and select real estate investments: With a focus on generating consistent cash flows. b) Exploring Asset-Based Finance: As it provides a compelling avenue for shorter-duration investments with attractive cash flow characteristics and strong collateral support.

- In an increasingly uncertain global landscape with rising trade barriers, we advocate for a portfolio strategy that emphasizes control and resilience. This includes a tilt towards domestic consumption themes, which are less susceptible to global trade disruptions. We also favor investment opportunities that offer greater control, particularly within private markets. In private equity, for instance, active management, operational improvements, and strategic consolidation can drive significant value creation. Finally, we believe that policy changes that foster corporate reform, as we observe in Japan, can unlock significant economic potential. However, as the intersection of national and economic security intensifies, we anticipate a policy shift towards encouraging domestic savings, higher corporate profitability, and a lower cost of capital for domestic businesses.

Exhibit 16B: Investors Should Focus on Long-Term Trends; As Returns Over 5+ Years Remain Strong Regardless of Entry Point.

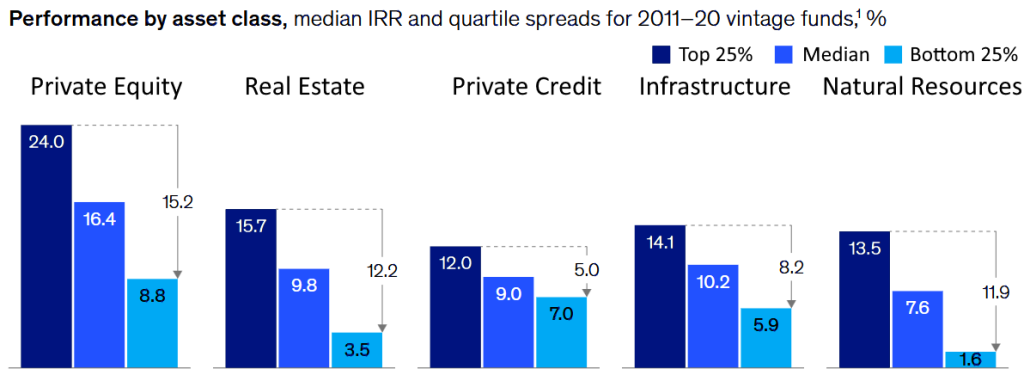

Exhibit 17: Private Markets Funds Show a Greater Performance Gap Between Top & Bottom Quartiles Than Other Asset Classes.

Long-term performance data (Exhibit 17) reaffirms private equity as the leading asset class in private markets. PE funds raised from 2011 to 2020 posted a median net IRR of 16.4% as of September 30, 2023, exceeding the top-quartile returns of all other private asset categories. The spread between top- and bottom-quartile PE funds for these vintages was 15%, a margin 300 basis points wider than any other asset class. Secondaries are also performing exceptionally well and are likely to remain a strong performer over the coming decade.

While the prevailing market sentiment anticipates increasing global liquidity and declining global interest rates, we believe investors should remain vigilant for potential disruptions. Six key risks stand out:

Point #1 – Disruption of Market Dominance. The possibility of sudden emergence of a revolutionary and cost-effective technology platform that could disrupt the competitive landscape, dethroning existing tech giants that dominate the global market. This potential new platform, with its superior capabilities and affordability, enables smaller firms and startups to compete at an unprecedented scale, undermining the market share of industry leaders. Institutional investors scramble to reassess the long-term viability of top global tech firms, leading to a rapid repricing of their valuations. So, what does this mean? We think: 1) Significant devaluation of dominant firms as their competitive edge or “moat” erodes. 2) Rapid capital flow shifts into smaller, technology & AI-driven disruptors, increasing market volatility. 3) Sector-wide repricing in technology, creating ripple effects across global markets.

Point #2 – Possibility of Erratic America Policy Changes. The prospect of new American political administration’s abrupt and unpredictable policy decisions could throw financial markets into disarray. Erratic sweeping changes to taxation, trade agreements, and fiscal spending could create significant uncertainty for businesses and investors. If we are correct then key industries—such as manufacturing, energy, and technology— could grapple with rapidly shifting regulations, supply chain disruptions, and uneven enforcement of new rules. The resulting economic turbulence risks undermining both domestic and global confidence in the U.S. as a stable economic leader.

Point #3 – Chaotic Trade Wars 2.0 & Potential “Collapse” of Global Supply Chains. The new American administration, driven by a nationalist agenda, could abruptly withdraws from key international economic agreements and imposes sweeping tariffs on imports from China, the European Union, and other major trading partners. The move, intended to “bring jobs back to America,” instead triggers a full-blown trade war. Retaliatory tariffs are swiftly enacted, and global supply chains, already strained by years of geopolitical tensions, begin to unravel.

As the cost of goods skyrockets, businesses around the world are forced to cut production, leading to widespread layoffs and economic contraction. The tech industry, heavily reliant on global supply chains, could be hit particularly hard, with shortages of critical components bringing production to a standstill. The automotive sector, already struggling with the transition to electric vehicles, faces existential threats as the cost of raw materials soars. The chaos may not be limited to the private sector. Governments, grappling with the economic fallout, are forced to implement austerity measures, further exacerbating social unrest. In the U.S., the administration’s approval ratings plummet as the promised economic benefits fail to materialize. The global economy, once a tightly interconnected web of trade and investment, begins to fragment into competing blocs, each pursuing its own economic interests at the expense of global cooperation.

Point #4 – Unforeseen Interest Rate Hikes: A combination of large fiscal deficits, robust economic growth, and sluggish productivity could unexpectedly necessitate a more aggressive monetary policy stance, leading to a sharp increase in interest rates, especially at the long end of the yield curve. Market Impact: This scenario could have a significant negative impact on several sectors, including Private Credit, Real Estate, and certain segments of the equity market. Economic Implications: Furthermore, such a rapid tightening of monetary policy could pose significant challenges for the broader economy.

Point ##5 – Large Cap Tech. (Mag7’s) Dominance Under Threat: A Potential Turning Point for US Equities. The sustained outperformance of the Magnificent Seven has driven a significant premium in their valuations and fueled momentum across the U.S. equity market (up 44% YTD vs. 18% for Value and Dividend). However, this premium is vulnerable if these companies fail to maintain their strong earnings growth. A slowdown in revenue and net income could destabilize the market, given the ‘halo effect’ the Magnificent Seven has had on other public equities.

Point ##6 – Currency Markets: Navigating a Turbulent Landscape. A confluence of factors – heightened trade barriers, burgeoning debt levels, and geopolitical instability – is poised to disrupt currency markets. The historical precedent of the 1994-2000 cycle serves as a cautionary tale. While the initial market rally post-2022 rate hikes was encouraging, we anticipate a period of heightened volatility, potentially mirroring the 1998 crisis. This period could be characterized by currency crises, amplified by excessive leverage. We are closely observing the US dollar and emerging market currencies, recognizing the need for some countries to adjust their exchange rates to enhance competitiveness. Put simply, a competitive devaluation could be a realistic possibility within the next four years.

We remain pro-risk but have chosen to moderate our stance compared to recent years, given that starting expectations for 2025 are both higher and more grounded in reality. Economic forecasters, having misjudged the macro landscape in prior years, now recognize the positive effects of productivity growth and government intervention. Alongside this, capital market sentiment is notably upbeat, limiting the likelihood of further compression in credit spreads. At the same time, equity trading multiples suggest a considerable level of optimism in current valuations.

Chaotic Trade Wars 2.0 & Potential “Collapse” of Global Supply Chains. The new American administration, driven by a nationalist agenda, could abruptly withdraws from key international economic agreements and imposes sweeping tariffs on imports from China, the European Union, and other major trading partners. … Retaliatory tariffs are swiftly enacted, and global supply chains, already strained by years of geopolitical tensions, begin to unravel.

– Barry Simon Graham (Group Co-CIO)

Our Key Message

While the challenge of delivering strong absolute returns in 2025 has grown, we remain optimistic under the guiding principle of “Thriving Amid Change: Harnessing Upward Currents.” Against this backdrop, investors should:

- Invest in assets with potential for faster-than-anticipated earnings growth.

- Prioritize opportunities in reform-driven economies with productivity and capital efficiency gains.

- Capture benefits from vital colossal investment themes or supportive market technical factors.

There are some compelling propositions under “Thriving and Change – Tapping the Strength of Upward Ocean Currents,” narrative:

- The Rise of “Super-Platforms”: We are in the “infant stages” of the rise of “super-platforms” – companies that leverage AI, data, and network effects to dominate multiple industries. These platforms could span sectors like finance, healthcare, transportation, and energy, creating unprecedented economic concentration and influence.

- Smart Labor; The “Creative Class” vs. the “Displaced”: The Industrial Revolution saw the rise of a new working class, often facing exploitation and poor working conditions. Looking forward AI and automation will likely displace millions of jobs. The “creative class” – those with high-demand skills in AI, data science, and other emerging fields – will thrive. However, there’s a risk of a widening wealth gap and social unrest if adequate support systems are not in place for those displaced by technological change.

- The Geopolitical Currents of the Next Decade: We think the next decade will be marked by intense geopolitical competition and rising nationalism.We expect continued geopolitical turbulence, with potential flashpoints in areas like the South China Sea, Eastern Europe, and the Middle East. The rise of new powers and the decline of traditional ones will further complicate the global landscape.

- The “Green & AI” Industrial Revolution: The late 19th century saw a technological revolution fueled by coal and steel. We think the 21st century will likely be defined by a “green & AI” industrial revolution, driven by renewable energy, sustainable technologies, and a circular economy. This transition will present both opportunities and challenges, requiring significant investment and collaboration across sectors.