Authors: Barry Simon Graham (Group Co-CIO) and Michael Yaw Appiah (Group Co-CIO)

This is Part B of our Investment Outlook 2024 series. You can find Part A here: Part A: Sunny Side of Shifting Currents – Global Investment & Economic Outlook 2024. In Part B of our latest macro insights, we dig deeper into key themes that may shape the landscape of private markets in the upcoming cycles. Explore some thoughts on the issues that could have a significant impact in 2024 and in the next two decades – under the scope of central themes and strategy asset allocations.

Central Themes.

Regarding central themes, the following observations are noteworthy:

1 Infrastructure

Infrastructure is currently experiencing a notable surge as an asset class. The persistence of high inflation and recent fluctuations in stock and bond markets have underscored the inherent resilience of numerous infrastructure investments. Given their indispensability to the economy and daily life, infrastructure assets provide cashflows that exhibit less correlation with economic cycles compared to other asset classes. Typically featuring long-term, inflation-linked contracts spanning decades, infrastructure holds a substantial advantage in times of market volatility. The enduring structural trends further bolster the case for infrastructure investment in the years and decades ahead. The global landscape is undergoing a transformative shift, necessitating a revamped energy system and widespread investment across sectors for decarbonization.

The global landscape is witnessing a significant expansion of digital infrastructure, intensifying the demand for datacenters, fiber broadband and cell towers. Concurrently, geopolitical fragmentation is reshaping supply chains, expediting trends like localization, regionalization, onshoring, nearshoring, and friend-shoring. This transformation is catalyzing fresh investments in pivotal logistics infrastructure, including railways and ports. Despite the numerous tailwinds favoring the asset class, managers must not grow complacent. The era of readily available cheap financing, which once bolstered returns, has ended, compelling managers to deploy additional strategies for value creation and active ownership. A more discerning and selective approach is imperative, with expectations of increased dispersion in manager returns. The current macroeconomic backdrop has also contributed to a slower year of fundraising, and in the secondaries market, discounts are emerging for the first time. For those with available capital, an enticing opportunity window has opened to acquire quality assets at more favorable entry points with attractive structures.

Infrastructure 3.0

Despite the robustness demonstrated by infrastructure in the past year, the more compelling narrative revolves around the opportunities unfolding in the foreseeable future. Coined as ‘Infrastructure 3.0,’ this encompasses forward-looking structural trends, with the transition to a net-zero and low-carbon economy emerging as a paramount investment opportunity within today’s private markets.

These trends are fueled by momentous policy strides that occur once in a generation. Although the Chips and Science Act and the Inflation Reduction Act and Chips in the U.S. made headlines in 2022 and due to its substantial incentives, the true impact is now beginning to unfold. Beyond providing direct financial support for numerous infrastructure projects, the legislation also facilitates favorable financing costs for various new assets and technologies. In Europe, the tangible effects of the REPowerEU Plan and EU Green Deal Industrial Plan are starting to manifest in day-to-day business operations. Continuous technological advancements persist in reducing costs and reaching the required maturity for the development of large-scale infrastructure 3.0 projects.

Cornerstone #1: Decarbonization

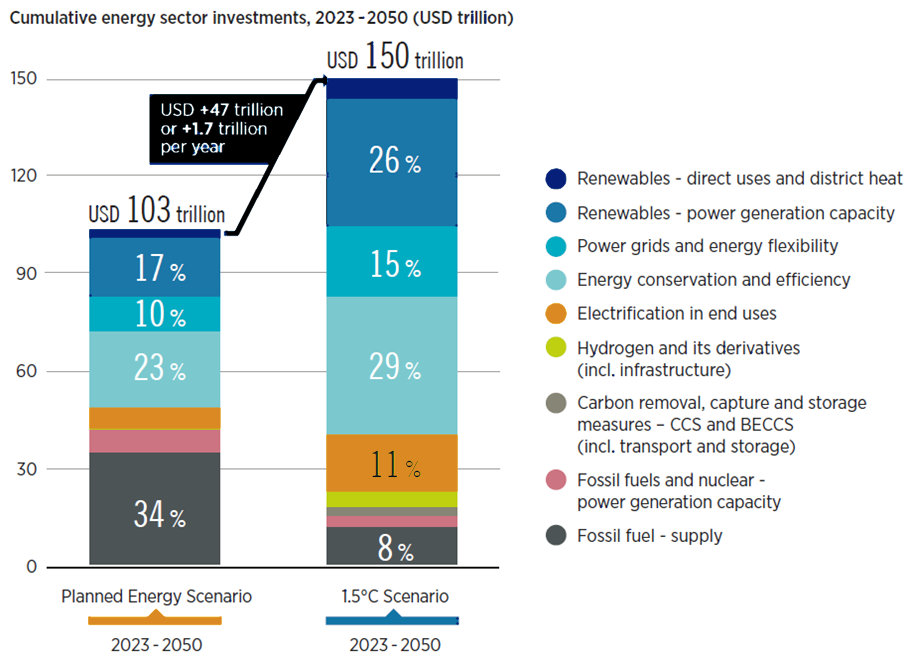

The move towards a net-zero and low-carbon economy stands out as one of several vital cornerstones reshaping both markets and the broader global economic landscape (refer to Exhibit 18, Exhibit 19, Exhibit 20). Despite the fact that its effect will reverberate across various asset classes, it holds particular significance for the realm of infrastructure. Looking into the future, the Zinqular Research and Insights Hub decarbonization scenario foresees a surge in the adoption of low-carbon energy sources, driven by the declining relative costs of these sources. This transition is poised to stimulate an average annual capital investment of about $ 5.3 trillion in the global energy system until 2050 under the 1.5°C Scenario, marking a substantial increase from the current level of just over $3.6 trillion per year on average under Planned Energy Scenario. This translates to investments of $150 trillion in transition technologies and infrastructure by 2050 (as shown in Exhibit 21). Low-carbon sources are also expected to constitute around 70% of the world’s energy within 30 years.

Technological progress is anticipated to drive cost reduction and enhance efficiency in energy storage, electrified transport, and alternative fuels for aviation and shipping. Our assessment of the potential extends to both global scale and local demand. Companies are intensifying their monitoring of emissions, extending into new domains like their buildings. The shift toward a low-carbon economy not only presents an investment opportunity but also serves as a lens through which to approach investment and risk. Given the immense scale of the transition, capitalizing on it requires investors to formulate views on cost trajectories, technological directions, and the evolving dynamics among value-chain segments. Although the transition directly impacts infrastructure, often at the forefront, it’s essential to adopt a comprehensive portfolio perspective.

Energy storage is a key component in the landscape of electrification— the transition to low carbon electricity— a significant shifts unfolding across power generation, transportation, and diverse domains. With the escalating pace of electrification, the importance of storage (i.e., batteries) and other energy-storage systems is increasingly apparent. The comprehensive energy storage value chain, spanning manufacturing, mining, refining, energy-grid support, deployment in vehicle charging, recycling, and second-life applications, is brink of significant growth.

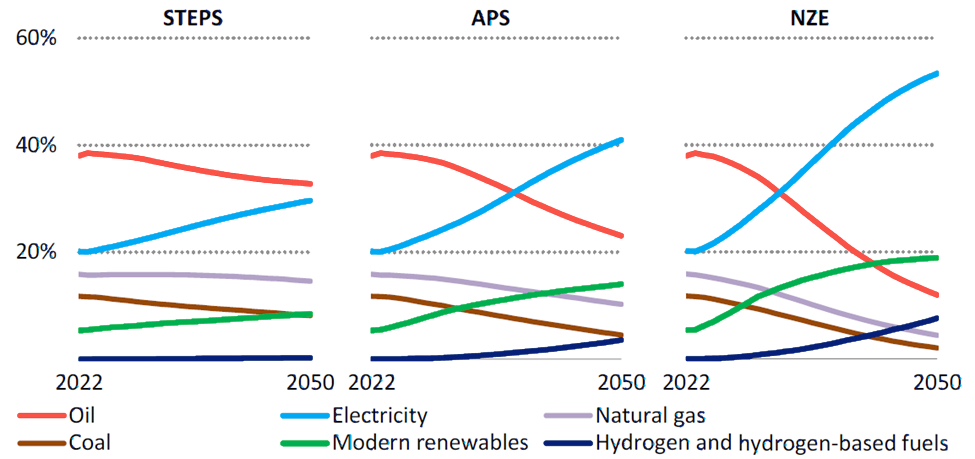

Exhibit 18: Share of Global Total Final Consumption by Selected Fuel and Scenario, 2022-2050. The Contributions of Electricity and Modern Renewables Increase While the Share of Fossil Fuels Declines in Each Scenario.

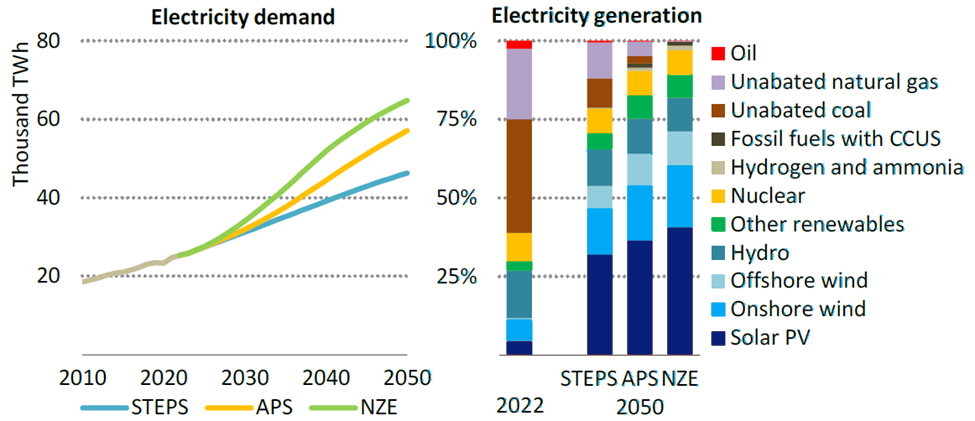

Exhibit 19: Electricity Electricity demand rises over 80% to more than 150% by 2050 across generation mix & scenarios and is met increasingly by low-emissions sources at the expense of unabated coal and natural gas.

Source: International Energy Agency | World Energy Outlook 2023, September 2023 Data: IEA, Zinqular Insights Hub

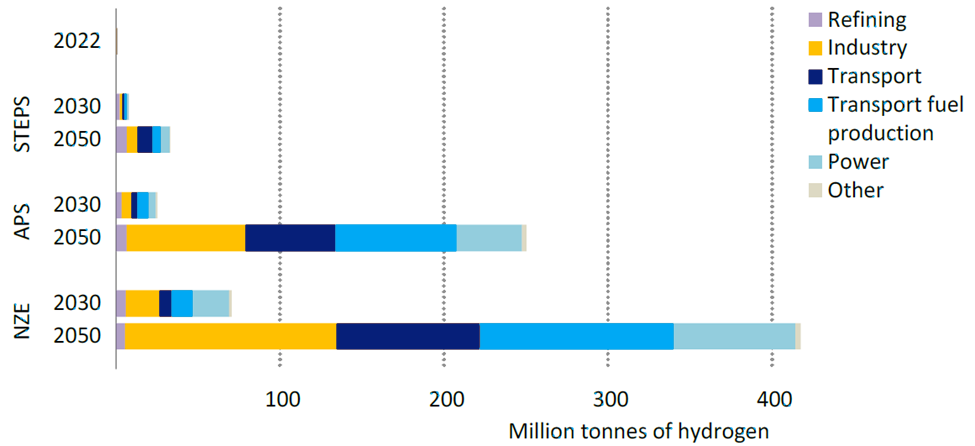

Exhibit 20: Global H2 demand by sector & scenario, 2022-2050. Demand for low-emissions H2 increases 60% per year to 2030 in APS, but despite continued strong growth, by 2050 it is at only 60% of the level required in the NZE Scenario.

Exhibit 21: Between Now & 2050, USD 150 trillion in Investments Would be Required for Decarbonization (Under 1.5°C Scenario).

The focus on decarbonization as a pivotal investment theme endures, with our perspective highlighting the dual facets of the Energy Transition ‘coin’ that demand investor attention. We maintain the belief that, throughout this transition, increased investments are essential in traditional energy sources, including oil and gas. Concurrently, we hold a positive outlook on the brown-to-green transition within existing corporate and government frameworks, offering substantial opportunities to enhance energy efficiency across major sectors of the global economy. While the past two decades witnessed asset-light decarbonization efforts fueled by advancements in software and technology, the upcoming phase is expected to lean towards more asset-intensive solutions. This shift is closely linked to the imperative of decarbonizing traditional power generation, property, transportation, and industrial sectors, as well as upgrading global supply chains, buildings, and data centers for sustainability. Managing this reality poses challenges for regulators facing the conundrum of balancing low-cost solutions in a high inflationary environment with the objectives of grid bolstering for decarbonization and environmental impact mitigation. The potential conflicts between these objectives elevate regulatory risk. Finally, the evolving landscape of AI and emerging energy forms necessitates a restructuring of energy distribution, offering significant opportunities for Infrastructure and specific segments of Private Equity.

Next Generation Digitalization

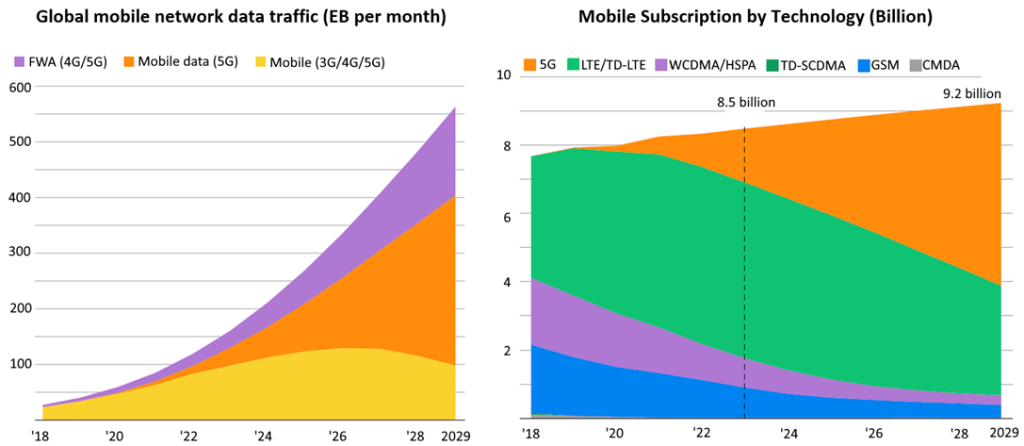

The world’s rapid digitization necessitates the development of physical infrastructure to support this transformation. As global connectivity to high-speed broadband internet proliferates, the demand for underground fiber grows. Simultaneously, the surge in mobile data transmission prompts the construction of additional wireless towers. Every online interaction and/or smart phone use contributes to data creation, intensifying the demand for storage infrastructure such as data centers. Notably, infrastructure is shifting closer to end users as governments prioritize self-sufficiency and security. The changing geopolitical landscape is fostering the localization of energy and industry, anticipating ongoing investments in domestic industrial infrastructure and the onshoring or near-shoring of critical industries.

Exhibit 22: Global Demand for Digital Services is Projected to Increase 400% by 2029. Global Mobile Data Traffic Consumption per Smartphone is Expected to Reach 56GB per Month at the End of 2029.

Evolution of Intra-Asia Infrastructure

In the area of connectivity; our data indicates a substantial shift in progress. Asia is increasingly orienting itself towards intra-regional trade, surpassing engagements with developed Western markets. Notably, the share of Asian trade within the region, compared to the West, has surged significantly from 46% to 60% within 3 decades. Foreseeing additional gains in market share, particularly when juxtaposed with intra-Europe trade at 67% in 2021, our focus lies on critical domains such as hyperscale data centers, sub-sea cables, logistics assets, energy transmission and transportation assets. A significant aspect of this expansion involves local financial institutions securing more of the regional market share. In contrast to the pre-Global Financial Crisis era when Western financial firms commanded 68% of overseas lending market, local Asian financial institutions dominated by China, Japan, and Singapore, now constitute over 50%. The region’s growth engine is robust, with more active participation and benefits observed in numerous countries. We think India and Southeast Asia as poised to gain from ongoing changes. Beyond favorable demographics, the expansion of multinational companies beyond China plays a pivotal role in this transformative process, fostering supply chain resilience and creating opportunities in data centers, logistics, and cost-effective manufacturing within the region.

2 Private Equity

As we navigate a new era marked by higher rates and market uncertainty, private equity finds itself in a phase of adaptation. Our “sunny side of shifting currents” persists, driven by the asset class’s remarkable track record of results / outperformance during market volatility. There are promising signals that near-term opportunities could be particularly appealing for buyers with accessible and plentiful capital. Let’s explore the key private equity themes defining this transformative period.

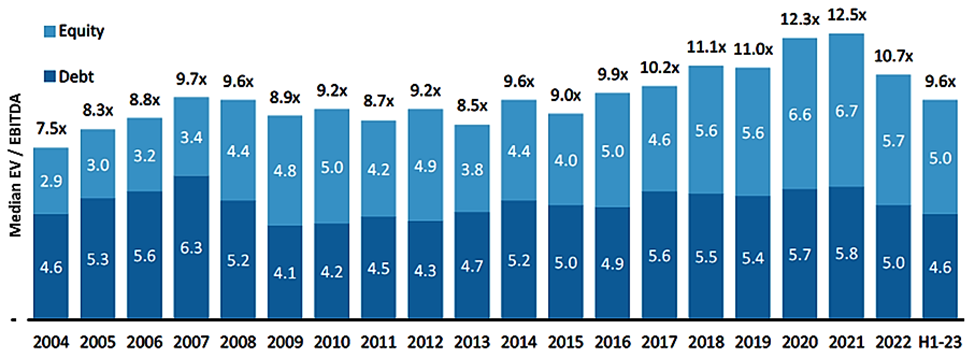

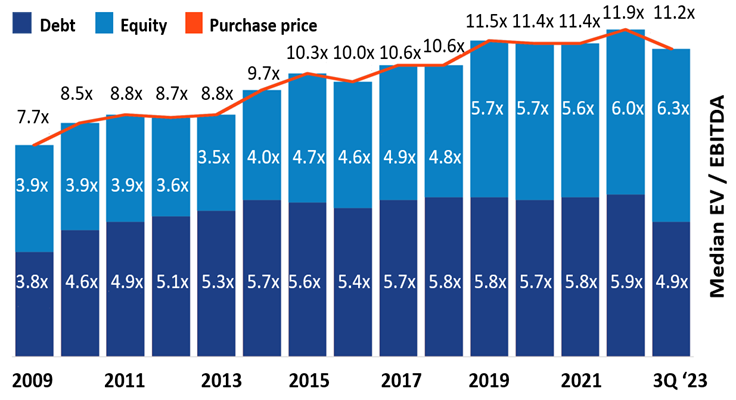

Valuation Evolution: The fluctuations witnessed in public markets are now influencing the realm of private equity valuations, marking a discernible descent. Following a persistent upward trend post the global financial crisis, valuations underwent a correction in 2023, declined by 9,6x EBITDA in the European market and resting at 11.2x EBITDA in the United States. This shift, however, unfolded against the backdrop of notably diminished deal activity, marking a deviation from the peak of 12.5x in 2021 for Europe and 11.9x noted in 2022 for the United States.

Deal Activities: Navigating the currents of rising interest rates, inflationary pressures, and the ebb and flow of economic and geopolitical uncertainties has ushered in a period of tempered deal activity. The year-over-year deal count witnessed a notable retreat, declining by a substantial 67% in 2022, with an additional 42% dip in 2023.

Transactions Types: Amid a shift in deal dynamics from the peaks of 2021 (Europe) & 2022 (US), the private equity landscape remains dynamic. Firms are pivoting towards strategic add-on acquisitions and leveraging the opportunity presented by lowered public equity valuations to fuel take-private transactions. Notably, public-to-private deals constituted excess 23% of the total deal value throughout the year, surpassing the 15% average observed over the past five years.

Transactions Equitization: With debt becoming scarcer and more expensive, private equity buyers are boosting their equity contributions to finalize deals. While the proportion of equity in total capital has been on the rise in recent years, the noteworthy shift in 2023 marks the first time that the average equity contribution surpasses the 50% milestone.

Demand for Quality: Navigating economic challenges and the surge in capital costs, private equity buyers are now setting their sights on industry leaders characterized by solid cashflow and impressive returns on capital. Investment priorities are favoring high-quality sectors and firms, with technology and healthcare taking center stage for their proven resilience.

Exhibit 23: European Area Private Equity Investments – Average Valuation Declines. There has been a slight dip in private equity valuations compared to their previous peak levels.

Exhibit 24: United States Private Equity Investments – Average Valuation Declines. There has been a slight dip in private equity valuations compared to their previous peak levels.

// Seize Perfect Opportunity to Buy

A positive outlook points to an upcoming uptick in deal activity, promising alluring returns for private equity buyers equipped with capital. This propitious timing positions the current period as an enticing opportunity to delve into this dynamic asset class.

Driven Sellers: With restricted entry into the IPO market and a muted appetite from buyside sponsors, the preceding two years witnessed exit deal volumes significantly below the norm. The cumulative exit volume for 2022 and 2021, totaling $ 961 billion, is a mere 67% of the average over this two-year period.

Debt Access: The slowdown in rate increases has sparked vitality in the syndicated loan market during 4Q 2023. This, complemented by significant inflows into private debt, is reshaping the borrowing landscape into a more favorable and dynamic terrain.

Corporate Divestitures: As the business landscape grapples with economic uncertainties, major corporations we believe are gearing up for an augmented wave of divestiture activities. This surge in corporate carve-outs presents a dynamic landscape of opportunities, allowing astute investors to acquire non-core divisions that harbor not only proven business models but also untapped reservoirs of value-creation potential.

Valuations: In the ever-shifting landscape of valuations, the dynamic interplay of volatility in public equity markets and the upward march of interest rates adds an extra layer of complexity. Marked by a significant doubling since December 2021, as indicated by the leveraged loan index, the prevailing environment necessitates a conservative pricing approach from buyers, safeguarding the integrity of returns.

Surge in Demand for Secondaries: With approximately 78% of private portfolios facing a shortage of exit opportunities, the quest for liquidity and meeting distribution needs has led limited partners to explore the secondaries market. Within this dynamic landscape, a surplus of opportunities continues to exert pressure on prices, creating enticing valuations. Notably, the mid-sized secondaries market, often overlooked by larger managers or deemed too substantial for smaller capital pools, stands out as an especially attractive area.

Dynamic Structuring: Private equity stakeholders are now exploring innovative avenues, such as minority sales and meticulously structured capital raises, to navigate the complexities of realizations and address maturing capital structures in a challenging deal environment. This dynamic approach unveils compelling risk-return prospects for potential buyers.

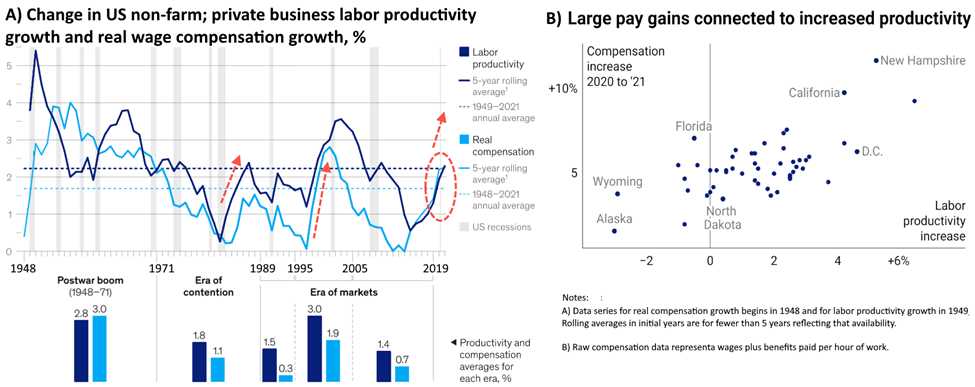

Labor Productivity & Evolution

Firms are urged to prioritize automation and the pursuit of increased productivity, particularly during periods of labor scarcity. Our team at Zinqular pays special attention to technological advancements that can positively influence productivity. Notably, significant technological trends like automation and digitalization, which were already underway before the pandemic, have experienced a notable acceleration. We are optimistic about trends in worker retraining, utilizing data and educational strategies to enhance the skills of students and employees, aligning them more effectively with the evolving labor requirements of corporations. Drawing insights from history, we associate recent increases in productivity with a resurgence in capital investment about 10 years. While the initial focus was heavily on manufacturing, there’s a visible shift as the aging population presents challenges in filling junior roles in service industries. Instances like robots taking on tasks at major ports in the Europe & United States and handling dishes in Japanese settings point to a growing trend of automation in sectors including retail, leisure, hospitality, and healthcare. Undoubtedly, we consider automation and productivity as emerging major forces, constituting a significant portion—around 30-35%—of our deal teams’ private equity activities.

Exhibit 25: Throughout history, rises in wages have typically been followed by boosts in productivity levels.

Shift towards Industrial Automation

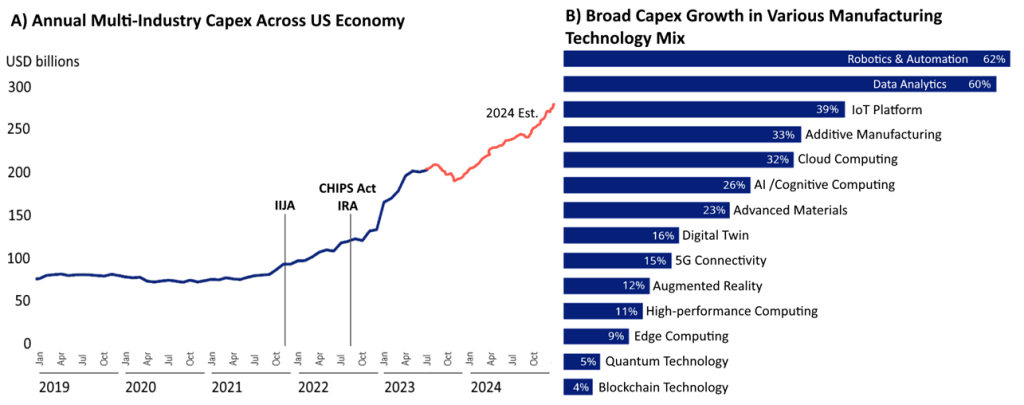

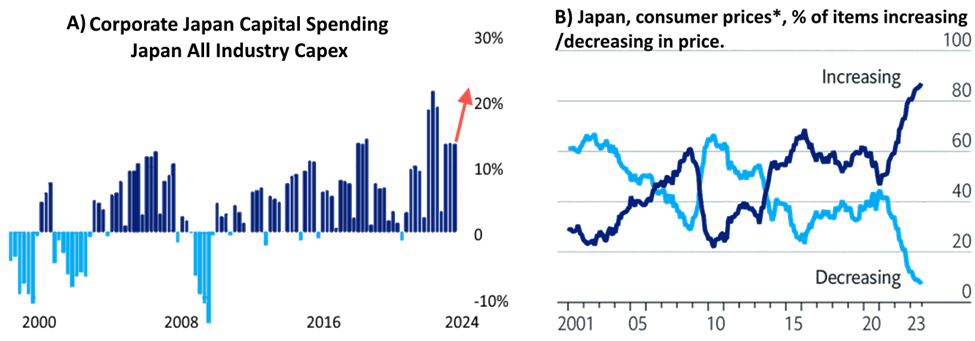

A significant theme particularly in Asia and the United States, is the unfolding industrial automation cycle (see Exhibit 26). In Japan, companies are experiencing record-breaking capital expenditures (illustrated in Exhibit 27) as they explore fresh avenues to enhance productivity. In a world marked by higher nominal GDP, where rising labor costs and other inputs pose a threat to profit margins, these investments play a crucial role. Similar sentiments resonate in China, Germany and the United States, where firms are strategically leveraging digitalization, technology and automation to drive efficiency and productivity, adapting to challenges posed by changing demographics and evolving cross-border connections. In this context, we express a preference for software innovations, such as those streamlining warehouse operations for improved energy efficiency, and industrial automation initiatives focused on modernizing manufacturing processes for enhanced global competitiveness. Additionally, our interest extends to mission-critical, highly engineered, and application-specific products characterized by a high cost of failure, despite constituting a small percentage of total product cost (e.g., flow control, testing/inspection/certification equipment).

Exhibit 26: US multi-industry capital spend expected to increase YoY in the near term due to major government programs, localization initiatives; and massive adaption of robotics & automation

Figure 27: Japan’s increased corporate capital expenditure remains robust, particularly amid worsening labor shortages. It getting expensive in Japan which is good for the economy after years of deflation.

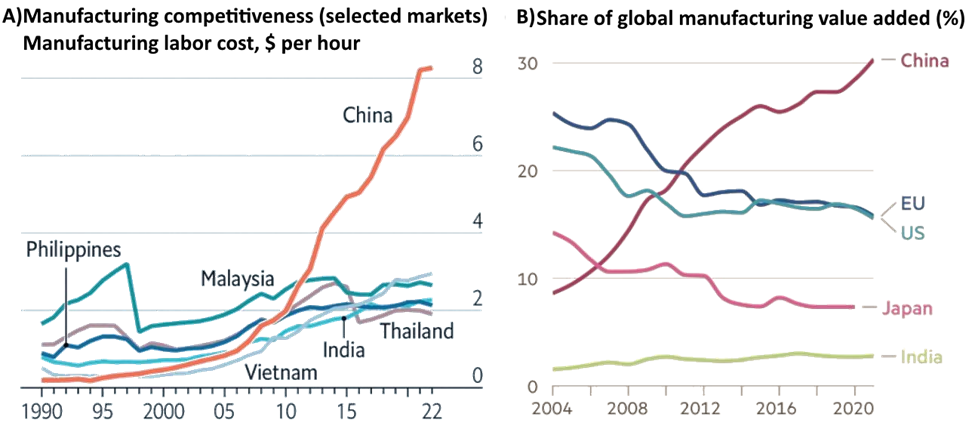

In addition, we see that China’s manufacturing wages correlates with its global manufacturing market share (see Exhibit 28). Far from being a headwind, it seems rising productivity translated to higher manufacturing competitiveness and higher wages. The high wages are sustainable because data indicates Chinese are more productive than their peers. Moreover, high-value-added jobs just don’t leave China. Therefore, a bit of caution is warranted; China is still an important player even within the scope of deglobalization/ regionalization. Allocators should bear that in mind.

The following is worth considering:

- Rising labor costs (wages) in the absence of inflation is a good sign for China’s economy. Manufacturing cost ex. wages is quite competitive.

- China’s manufacturing is a lot higher value-added goods (e.g., aviation spare parts, advanced robotics, electric vehicles, some semiconductors, etc.) than the lower value-added goods that move to say Philippines, Thailand, Vietnam and India.

- We think the west decoupling from China is doable but will take much longer time & certainly lead to inefficient commerce through the “unwinding” of global supply chains.

Figure 28: High wages correlates high productivity that also mean high manufacturing competitiveness in value added goods.

Cornerstone #2: Artificial Intelligence (AI)

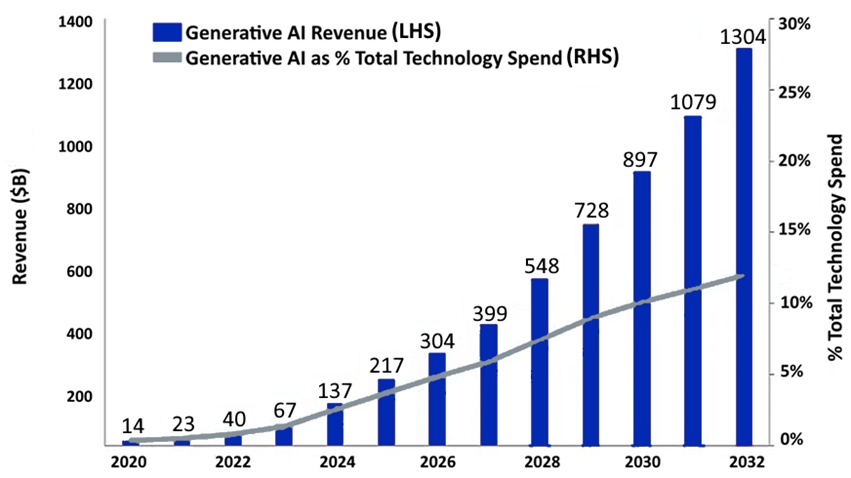

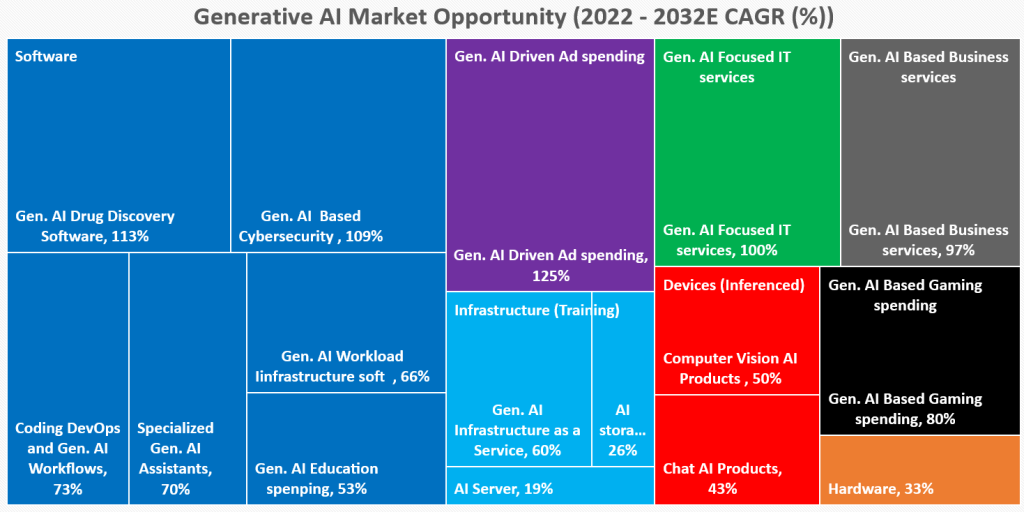

The potential for generative AI (Gen AI) is unlimited and it is poised to unleash the next wave of productivity. Gen AI’s economic benefit is forecast to worth up to $7.9 trillion annually (refer to Exhibit 29, Exhibit 30). AI has permeated our lives incrementally, through everything from the tech powering our smartphones to autonomous-driving features on cars to the tools retailers use to surprise and delight consumers.

Generative AI applications such as OpenAI’s ChatGPT, GitHub Copilot, Stable Diffusion, Anthropic’s Claude, Google’s Bard and others have captured the minds of people around the world in a way past legacy AI program(s) did not, thanks to their broad utility—almost anyone can use them to communicate and create—and preternatural ability to have a conversation with a user. The latest generative AI applications can perform a range of routine tasks, such as the reorganization and classification of data. But it is their ability to write text, compose music, and create digital art that has garnered headlines and persuaded consumers and households to experiment on their own. As a result, a broader set of stakeholders are grappling with generative AI’s impact on business and society.

The potential within the Artificial Intelligence (AI) investment landscape is enormous, with estimates projecting Generative AI (Gen AI) market to potentially exceed $1.3 trillion within a decade (2033).

Exhibit 29: Generative AI revenue to exceed $1.3 trillion by 2032 delivering $7.9 trillion economic benefits.

Exhibit 30: AI Industry to Grow at CAGR of 42% Over Next 10 Years. Rising demand for Gen. AI products to add ~ $280 billion of new software revenue.

// Unlocking New Avenues of Opportunities

We think within traditional venture and growth investing AI is an enticing avenue for investment in innovative firms, even more AI holds the transformative potential to rebalance the scales in favor of established players. The impact of Gen AI has reshaped the landscape in software, where industry giants’ AI investments have set ambitious benchmarks for startups to catch up. The horizon of AI applications extends into our investments in industrials, infrastructure and real assets offering potential in areas with mission-critical services. Across diverse sectors, AI emerges as a potent force, expanding the canvas of investment opportunities.

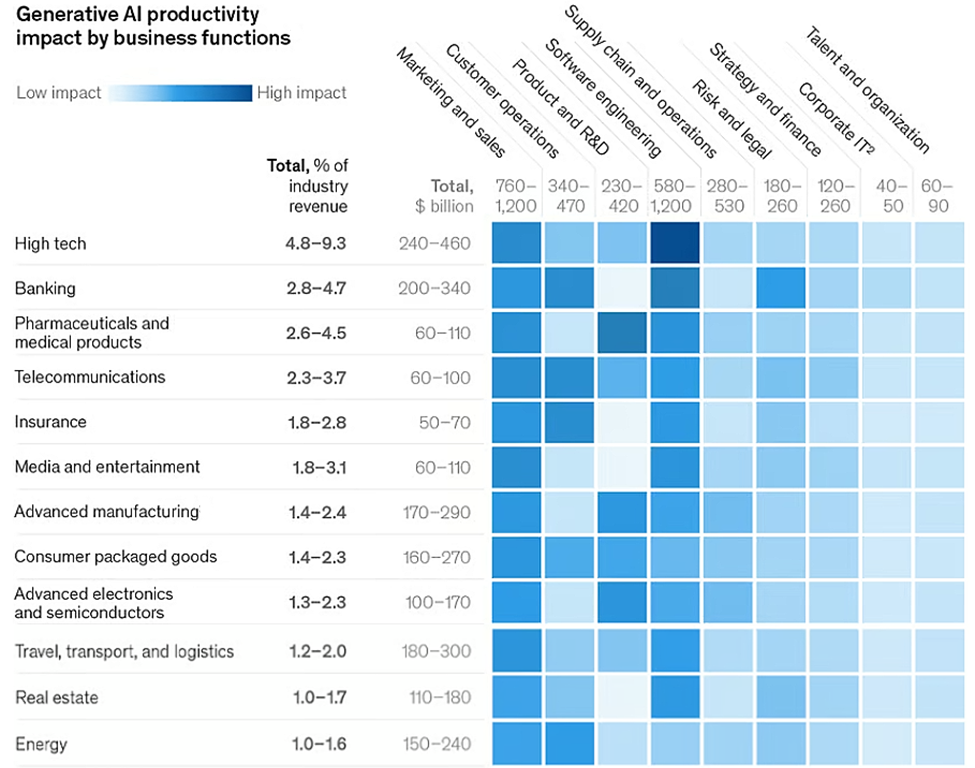

Generative AI’s impact on productivity could add up to $4.4 trillion annually across the 63 use cases; increasing the impact of all AI by 15 to 40 percent (refer Exhibit 31). This estimate would roughly double if we include the impact of embedding generative AI into software that is currently used for other tasks beyond those use cases.

Exhibit 31: Across 63 use cases, generative AI potential to generate up to $4.4 trillion in value across industries. Impact depends on mix of factors, e.g., mix & importance of different functions /incl., scale of industry’s revenue.

About 75% of the value that generative AI use cases could deliver falls across four areas: Customer operations, marketing and sales, software engineering, and R&D. Across 16 business functions; generative AI will have a significant impact across all industry sectors. Banking, high tech, and life sciences are among the industries that could see the biggest impact as a percentage of their revenues from generative AI. Across the banking industry, for example, the technology could deliver value equal to an additional $200 billion to $340 billion annually if the use cases were fully implemented. In retail and consumer packaged goods, the potential impact is also significant at up to $660 billion a year.

The pace of workforce transformation is likely to accelerate, given increases in the potential for technical automation. Our updated adoption scenarios, including technology development, economic feasibility, and diffusion timelines, lead to estimates that half of today’s work activities could be automated between 2030 and 2060, with a midpoint in 2045, or roughly a decade earlier than in our previous estimates.

Generative AI can substantially increase labor productivity across the economy, but that will require investments to support workers as they shift work activities or change jobs. Generative AI could enable labor productivity growth of 0.1 to 0.6 percent annually through 2040, depending on the rate of technology adoption and redeployment of worker time into other activities. Combining generative AI with all other technologies, work automation could add 0.2 to 3.3 percentage points annually to productivity growth. However, workers will need support in learning new skills, and some will change occupations. If worker transitions and other risks can be managed, generative AI could contribute substantively to economic growth and support a more sustainable, inclusive world.

// Caution: Brace for the Hype!

The era of generative AI is just beginning. Excitement over this technology is palpable, and early pilots are compelling. But a full realization of the technology’s benefits will take time, and leaders in business and society still have considerable challenges to address. These include managing the risks inherent in generative AI, determining what new skills and capabilities the workforce will need, and rethinking core business processes such as retraining and developing new skills. With AI taking the spotlight in media, countless businesses are flaunting their AI capabilities. Yet, as the landscape of this evolving technology unfolds, a closer look is warranted. When exploring a company’s AI solutions, it’s wise to uncover the obstacles that competitors might grapple with on their AI journey.

// AI Influence on Investment Process

AI’s role in revolutionizing the investment process is in constant flux. Companies are actively charting its potential to amplify value and efficiency, all the while safeguarding against risks for their businesses and clients. At Zinuqlar, our current approach involves employing AI and expansive language models, enabling us to craft predictive strategies rather than reactive ones in managing deal flow.

// Investing in the Value-Chain

Zinqular’s investment approach in AI are strategically delicately balanced and refined. While direct investments in Gen AI technology development are interesting, they can also be fairly pricey. Conversely, we identify AI Value Chain or non-direct play on AI; encompassing semiconductor manufacturing, hyperscale data center capital expenditure, and power transmission and distribution, as potential areas for substantial investment cycles driven by the imperative to develop core infrastructure.

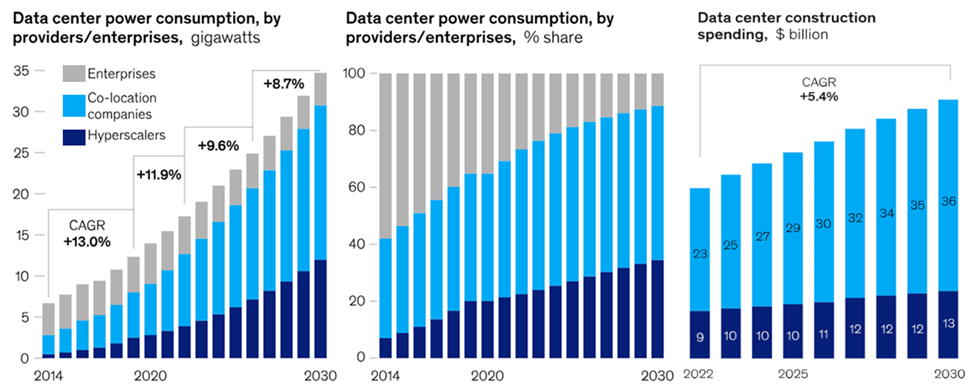

The explosion in demand for data centers has attracted the attention of investors of all types; often due to the steady, utility-like cash flows and risk-adjusted yields. The expansion of AI work streams occurs amid significant backlogs, rising lead times, and heightened construction costs for hyperscale datacenter operators and owners, who contribute about 50% of data center capital-related investments (as shown in Exhibit 32, Exhibit 33). In the US market alone, demand—measured by power consumption to reflect the number of servers a data center can house—is expected to reach 35 gigawatts (GW) by 2030, up from 17 GW in 2022. The United States accounts for roughly 40 percent of the global market.

Scaling data center infrastructure swiftly to meet the escalating demand for computing capacity is expected to be challenging. Estimates suggest that servers used in model training and inference could add up to 18% increase from the current. Beyond increased data center demand, we anticipate heightened focus on power distribution. The intensified power demand from AI work streams, known for their computational intensity, is driving a shift from air cooling to liquid cooling in data centers. However, we harbor reservations about Gen AI’s ability to fully counter demographic challenges and labor shortages on wages at the macro level. Various ‘gating factors,’ including cybersecurity complexities, data privacy concerns, regulatory uncertainties, labor disputes, and shortages in high-end computing capacity, may impede the widespread adoption of Gen AI in displacing high-skill service positions. At the same time, we acknowledge the long-term potential of AI, we believe that some of the most enticing opportunities may lie beyond mega-cap software firms, focusing instead on addressing physical infrastructure bottlenecks and the substantial investments required, especially in building the essential ‘backbone’ before Gen AI can achieve widespread scalability.

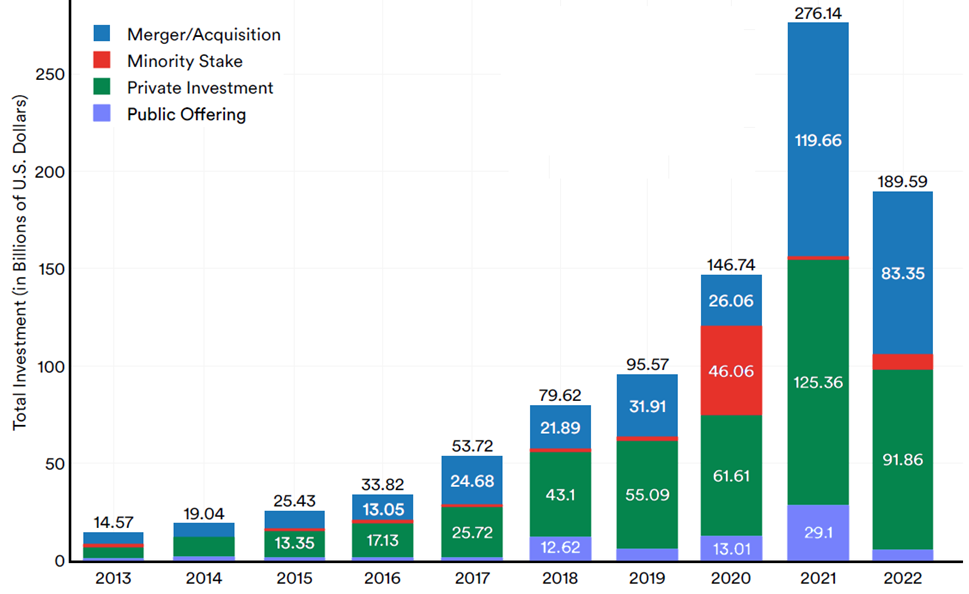

Exhibit 32: AI-related investment from 2013 to 2022 increased 13folds. For the first time since 2013, YoY global AI investment decreased. In 2022, total global AI investment was $189.6 billion, roughly a 3rd lower than it was in 2021.

Apart from pure-play investments in AI data centers assets in recent years, there are plentiful opportunities in the sector’s other value chain going unnoticed.

Exhibit 33: US Data center demand is forecast to grow by some 10% annually until 2030. Global spending on the construction of data centers is Forecast to reach $49 billion by 2030.

Source: Synergy Research Group (SRG). Data: SRG, Mckinsey, Zinqular Insights Hub

Data centers have other value chain opportunities / assets such as: Hosting and infrastructure as a service (IaaS); Power and connectivity; Sustainable (or green) energy; Cooling and energy consumption; and Constructing prefab and modular data centers.

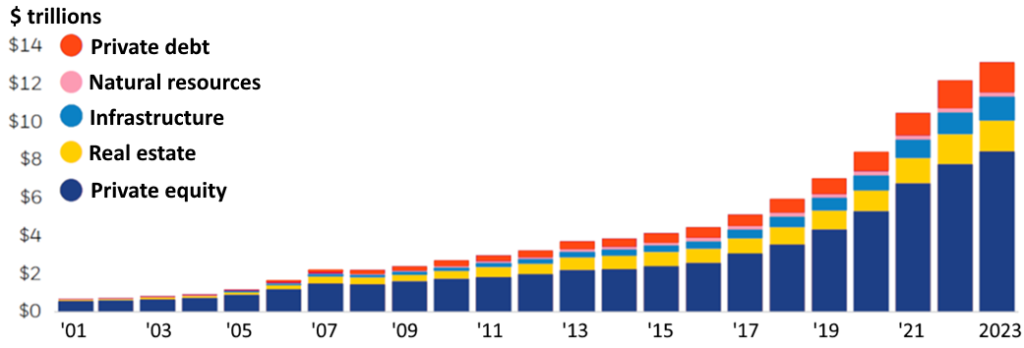

3 Private Debt

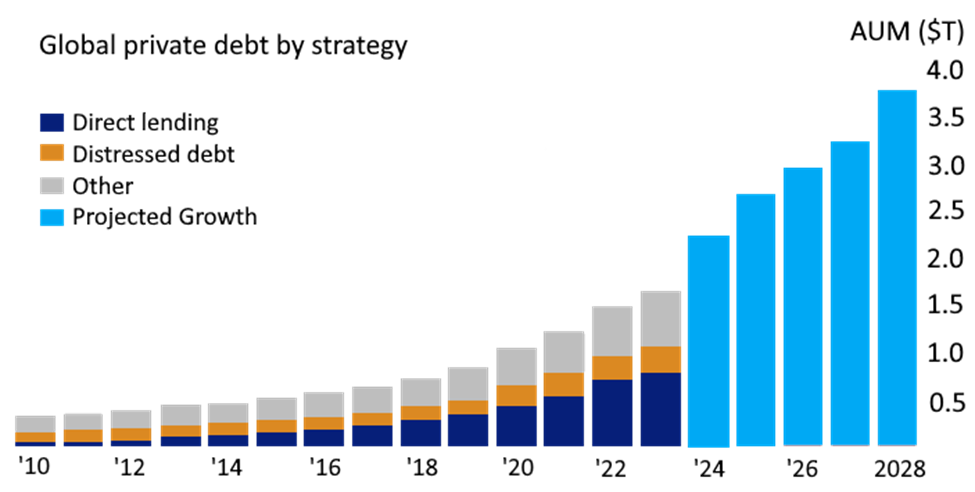

The momentum of private debt’s expansion persists, solidifying its stature as a substantial and scalable asset class appealing to a diverse set of long-term investors. Surpassing $ 1.94 trillion globally as of December 2023 reaching almost $17 trillion in 2030, it comprises around 13% of the extensive $1.3 trillion alternative investment landscape per Zinqular Insights data (refer to Exhibit 34, Exhibit 40 for further details). Under the overarching label “private debt,” various strategies coalesce, with direct lending emerging as the largest in terms of assets under management. These encompass strategies like venture, distressed, opportunistic and mezzanine approaches. Over the past decade, the addressable market in private debt has notably widened, driven by the retreat of banks and public lenders from the middle market. This evolution has empowered direct lenders to facilitate more substantial deals, prompting a heightened investor inclination toward private debt for tapping into income opportunities within middle-market enterprises.

Although direct lending remains the predominant private debt strategy, the annual shift in private debt fundraising dynamics can exhibit fluctuations. Investor preferences are notably influenced by the macroeconomic environment, with economic downturns creating opportunities for strategies like distressed lending. We think in 2024, the diverse impact of heightened capital costs on sectors and firms will hinge on factors such as business resilience, pricing power, and capital structure management. This context is expected to promote divergence, not disruption, across asset classes, sectors, and issuers. A subtle distinction and defensively-oriented investment strategy, incorporating structural protections, meticulous underwriting, and judicious credit selection, will be pivotal in 2024 to maintain attractive all-in yields, particularly in segments like senior direct lending.

Exhibit 34: Growing in importance, private debt now accounts for 12% of the overall value of alternative assets under management, encompassing both unrealized value and dry powder

Private Debt Landscape: Challenges & Opportunities

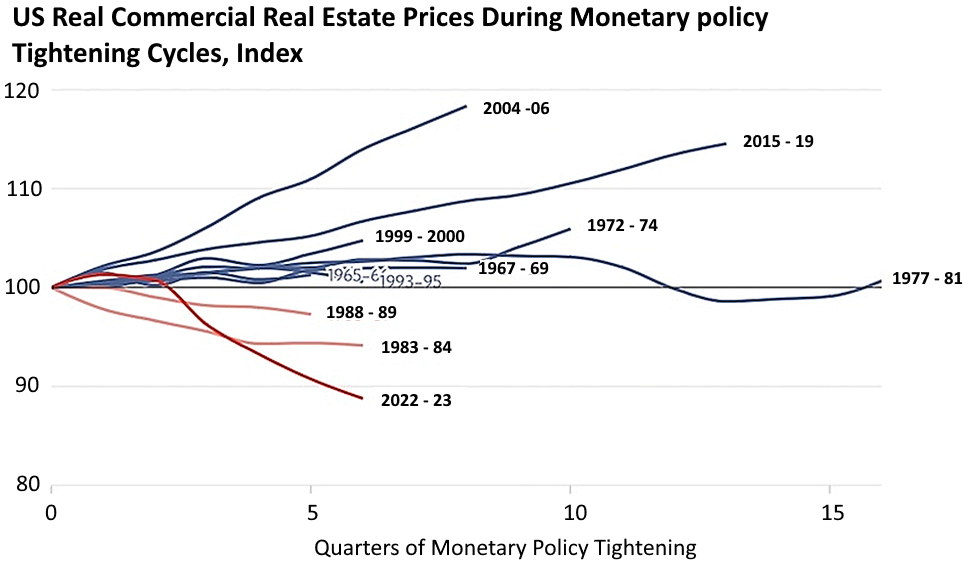

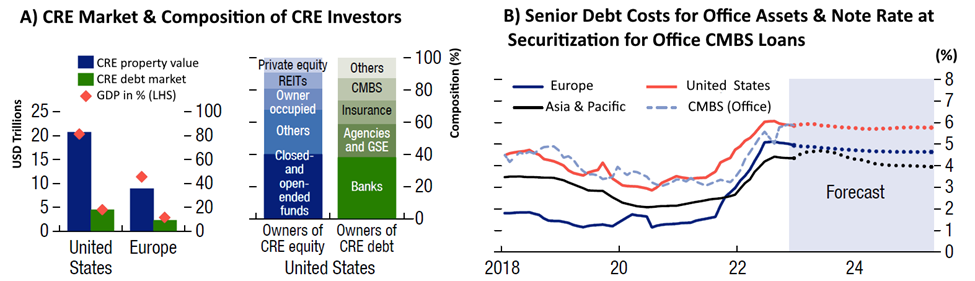

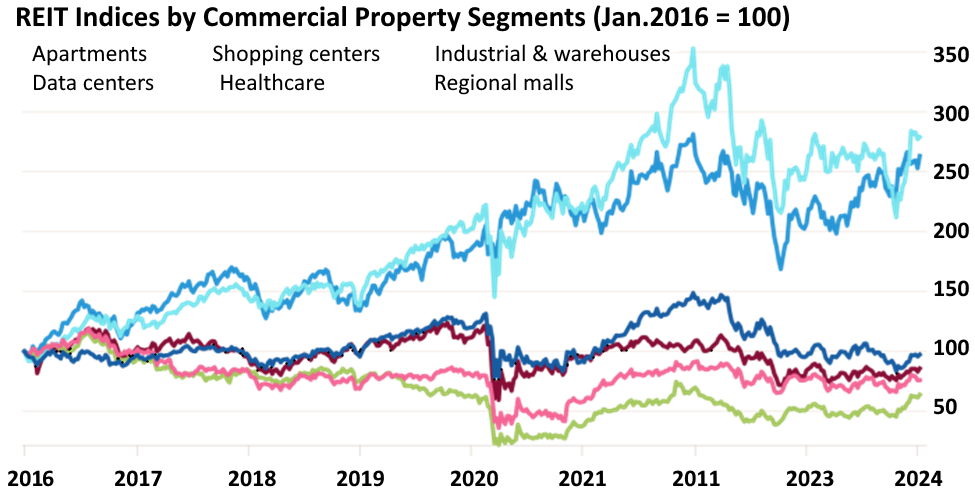

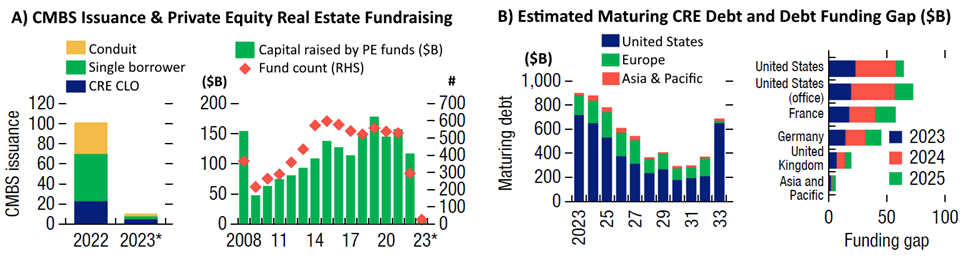

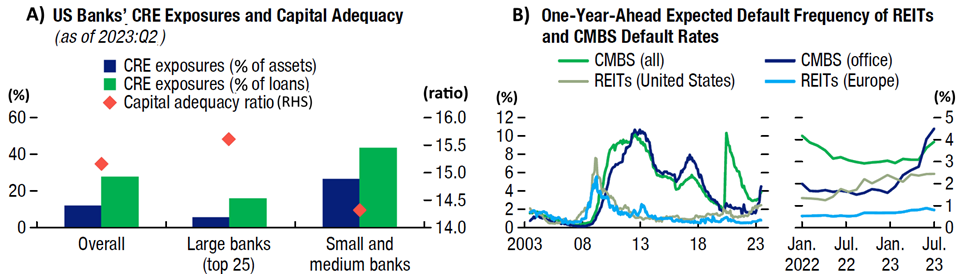

In the domain of private debt, the U.S. and Europe commercial real estate market is displaying discernible levels of divergence. Specific subsets, notably the commercial office area, find themselves amidst a perfect storm of well-communicated challenges. These obstacles encompass an environment of stricter lending criteria from banks, “higher-for-longer” interest rates, resulting in elevated refinancing costs, substantial maturity walls in the near future, and shifts in asset utilization post-pandemic, particularly in commercial office sector (shown in Exhibit 35, Exhibit 36, Exhibit 37, Exhibit 38, Exhibit 39). Concurrently, we anticipate favorable trajectories for various real estate debt categories like industrial asset, hotels, self-storage, and retail beyond malls, propelled by robust business fundamentals, demographic trends, sustained demand, and structural transformations such as the impact of ecommerce shopping and the reinforcement of supply chain resilience through inventory buildup.

// Expansive Tailwinds

Companies are increasingly looking to the private debt markets as a viable funding option, influenced by various factors such as stricter bank lending standards and shifts in public markets catering to larger borrowers. More companies are adopting “multi track” approaches, simultaneously exploring several avenues including both public and private markets for their financing needs. A noteworthy trend is the surge in direct lending deals aimed at refinancing widely syndicated term loans. Our internal data records show at least 12 such transactions in 2023, amounting to nearly $24 billion in total. With the continued growth of the private debt market, its capacity to compete directly with public debt financing markets is likely to expand. This broader spectrum of available deals will enable the private debt market to extend its reach to more borrowers, fostering the continued growth of this asset class.

Exhibit 35: Serious Setbacks. Prices in the US Commercial real estate sector have dropped more in this present monetary policy tightening cycle regime than in earlier periods

Exhibit 36: CRE exposures constitute a major share of GDP and balance sheets of financial institutions. Borrowing costs are up and are expected to remain elevated, particularly in the CRE office.

Notes: A) CRE debt estimates are based on the historical debt stock and the investable universe of real estate stock. Total CRE values are based on Australian Prudential Regulation Authority top-down approach for Europe and Nareit estimates for the United States. B) note rate at securitization for CMBS loans is weighted average coupon of new-issue office-backed conduit CMBS. CMBS = commercial mortgage-backed security; CRE = commercial real estate; GSE = government sponsored enterprise; REIT = real estate investment trust.

Exhibit 37: The market for commercial Real Estate Assets has seen Dispersion across various property segment. Industrial & Warehouse and Data centers outperformed its peers by over 300%.

Exhibit 38: The turmoil facing lenders force some to step back, leaving space for investors; CRE funding hurdles remain. Large refinancing volume is coming due, further driving repricing in vulnerable markets impacted by structural trends.

Exhibit 39: We think banking sector should be able to absorb CRE losses, but larger shocks could impact smaller & regional banks and put pressure on REITs and CMBS, as declining demand dampens rental growth and occupancy rates while borrowing costs escalate.

Cornerstone #3: Finance 3.0

The global financial sector is experiencing seismic changes, reshaping the landscape of every facet of finance especially the deposits and credit markets in the United States. In this transformative shift, the private debt market positions itself as a crucial recipient of advantages. Reviewing our data, we envision a global private debt market with the potential to soar to $ 3.8 trillion in assets under management by the close of 2028, a significant leap from the global $ 1.8 trillion recorded as of November 2023 (as shown in Exhibit 40).

What is propelling this growth? This is being driven by borrower preferences for tailor-made funding solutions, execution certainty, and the adaptability of establishing enduring borrower/lender relationships. Institutional investors and asset managers seek diversification within a comprehensive portfolio, aiming to integrate framework of safeguards based on their strategy.

Furthermore, foundational changes in public markets, now catering to larger borrowers, make public debt-market deals too substantial for most middle-market companies. Ongoing reduction in the availability of bank credit is poised to open up additional opportunities for the private debt sector to broaden its reach among potential borrowers.

Private debt has typically outperformed the public markets in terms of loss rates. In the 2Q2023, trailing 12-month loss rates for USD Leveraged Loans and USD High Yield were 1.68% and 1.62% respectively, whereas direct lending recorded a lower rate of 0.69%, as per the Cliffwater Direct Lending Index.

Exhibit 40: Private debt is booming. We estimate it will grow to almost $4 trillion globally by 2028.

3 Real Estate

// Unlocking Value in Uncertainty

A promising horizon is unfolding for real estate investors. On a global scale, valuations are in the process of adjusting downward from their peaks in 3Q2022, influenced by heightened inflation, interest rates, and volatility. This unique landscape offers investors the opportunity to acquire top-tier assets at appealing prices, frequently below replacement cost. Additionally, bid-ask spreads are beginning to converge as investors demand higher risk premiums across various sectors.

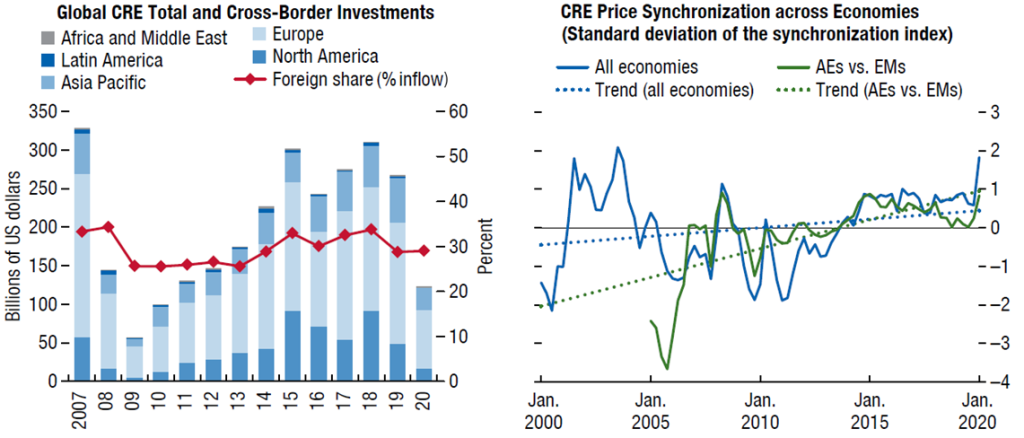

The real estate asset class has a track record of robust performance in the aftermath of market disruptions, making the current environment of repricing against a backdrop of stable market fundamentals quite enticing (refer to Exhibit 41 see how real assets investments recovered after GFC). Yet, there are formidable challenges ahead. Global transaction volume has experienced a substantial 60% year-over-year decline, primarily driven by the elevated cost of capital. Looking ahead, limited access to financing is poised to shape an environment markedly different from the low-rate era that followed the global financial crisis.

As banks navigate the evolving landscape, the persistent financing constraints pave the way for non-bank lenders like pure play debt funds and insurance firms to play a pivotal role. This dynamic shift in capital availability, varying across sectors and markets, sets the stage for a compelling opportunity. In this evolving scenario, investors leaning towards minimal or no leverage stand to benefit in a less-liquid environment. Over the next few years, the landscape promises a tapestry of performance across sectors, markets, and asset quality, unlocking avenues for alpha generation. Since 1H2022, dispersion has been a defining feature of the asset class, spurred by the impact of interest rates on private markets. Looking ahead in 2024, we anticipate dispersion to continue as a major investment theme. In navigating this terrain, we emphasize the significance of astute asset selection, with location retaining its critical role. For investors poised to deploy their dry powder, a strategic focus on higher-quality real estate, known to outperform in the early stages of real estate market recoveries, is worthy of consideration.

Exhibit 41: Unlocking Potential in Times of Uncertainty. Global and cross-border CRE investments had recovered since the global financial crisis.

Sources: Global Financial Stability Report: Preempting a legacy of vulnerabilities. Data: MSCI Real Estate, Real Capital Analytics, IMF, Zinqular Research Hub.

// Exploring Islands of Potential

In the evolving market scenario, income growth and yield are set to take center stage for real estate investors. This underscores the significance of resilient cash flows and the ability to set competitive rent prices. As the market undergoes shifts, it’s crucial for investors to keep a close eye on specific areas. For instance, is the emergence of excess supply in certain high-growth U.S. multi-family apartment markets, sparking essential queries for these sectors.

Zooming out, the mid-term landscape signals a mitigated risk on the supply front. Developers are encountering heightened capital costs in both equity and debt markets, potentially acting as a significant brake on new development endeavors. Concurrently, the anticipation is for a restrained influx of new logistics supply in specific markets, especially in leading cities of Germany, Sweden, Australia and New Zealand, influenced by the intricacies of land zoning geographic layout and.

Let’s take a stroll through the Asia-Pacific, where the impact of higher interest rates on the sales market is quite evident. Amongst the neighboring countries; Japan and Vietnam have good market dynamics. For example, Japan stands out as an exception with its relatively low interest rates. This unique scenario reflects in real estate transaction volumes, where Japan experiences a mere 11% year-over-year decrease, in stark contrast to the broader APAC region’s significant 34% decline per Zinqular Research Hub data.

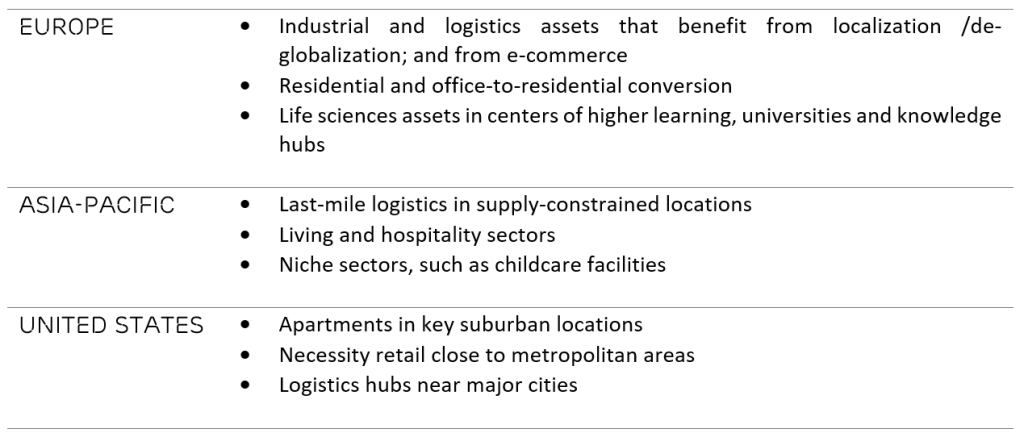

Even in the midst of a measured pace in capital markets, compelling trends persist on the ground, bolstering various property types. Industrial and logistics properties maintain their allure on a global scale. Residential sectors in the Europe, U.S., and select APAC markets present robust growth potential. Moreover, necessity retail in the U.S. stands out favorably due to enticing entry points and limited supply. Beyond the cyclically influenced opportunities arising from adjusted valuations, we discern powerful forces influencing performance dispersion. These include noteworthy trends like demographic shifts, the restructuring of supply chains, and the shift toward a net-zero economy.

// Areas and Assets Primed for Exceptional Performance.

Cornerstone #4: Impact of Demographics

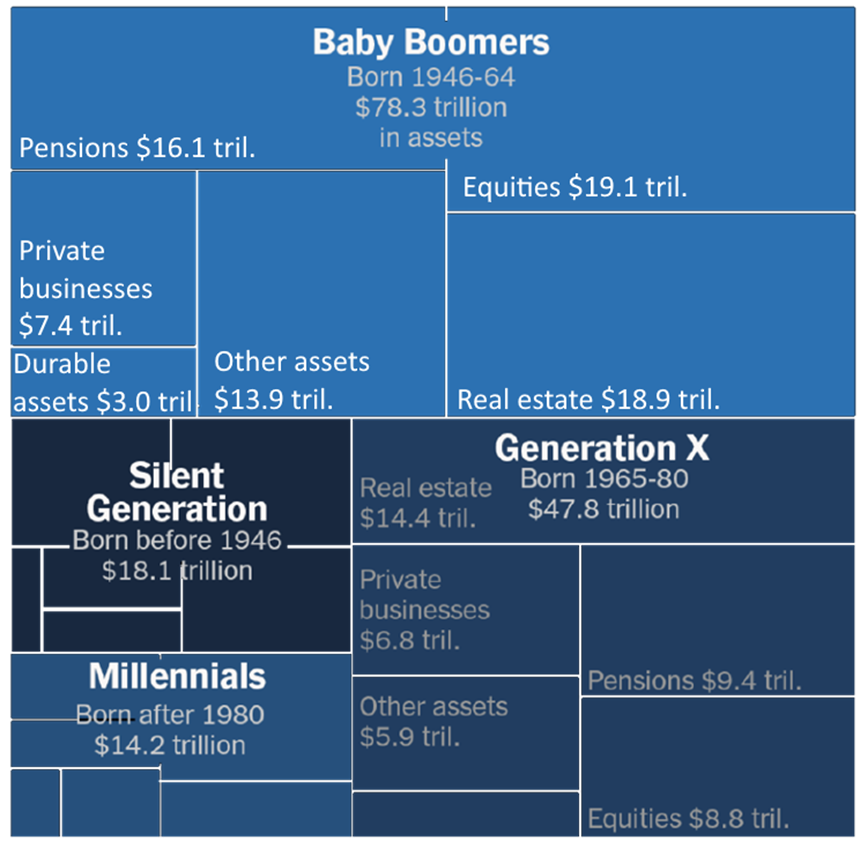

Two colossal generational cohorts are embarking on transformative journeys, propelling dynamic shifts in the real estate landscape (refer to Exhibit 42, Exhibit 43). The transfer of wealth across generations in America is currently underway, and its scale surpasses anything seen in the past. This process is not a future projection but is actively occurring at present.

With the rising trend of “giving while living,” heirs no longer have to await the passing of older family members to access family wealth directly. This approach includes various methods such as property acquisitions, repeated tax-free cash transfers from estates, and other strategies, enabling millions to gain an early advantage. Amidst this landscape, the top 10 percent of households emerge as pivotal players, both contributing to and receiving the lion’s share of wealth transfers.

Exhibit 42: Baby boomers hold 50% of America’s $140 trillion wealth. Inter – generational wealth transfer from Baby Boomers to Millennials is underway.

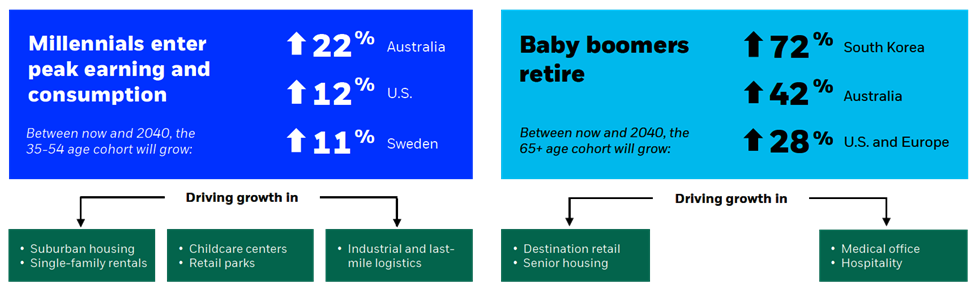

The dynamic interplay between two colossal generational forces, the Millennials and Baby Boomers, is reshaping the global real estate landscape. With 1.85 billion Millennials forming families, the demand for spacious apartment units and suburban single-family houses is on the rise worldwide. Notably, homeownership remains a global challenge for this generation, propelling a growing inclination towards renting and potentially fueling the momentum of the residential rental sector.

The years of building families not only mark a time of abundant growth in consumption and income but also set the stage for significant changes in retail and industrial landscapes. As Millennials step into this phase, their demand for essential retail in bustling locations will soar, driving the growth of industrial properties fueled by the expanding realm of e-commerce. Additionally, Millennials are poised to fortify specialized sectors like childcare centers, especially when these are structured as triple-net leases, offering a strategic shield against inflation risks for both investors and operators.

In tandem, the advancing age of the global Baby Boomer cohort, recognized as the “Silver Wave,” is set to unleash heightened demand in key sectors. The affinity of retirees for travel is boosting the attractiveness of destination retail and hospitality properties; and healthcare and social services real estate; while the aging demographic is fueling a surge in global demand for medical office spaces. Specific housing communities designed for various age groups also emerge as compelling investment prospects. To navigate this mega trend successfully, investors must possess a nuanced understanding of the unique social, economic, and cultural trends prevalent in specific regions, countries, and micro-locations.

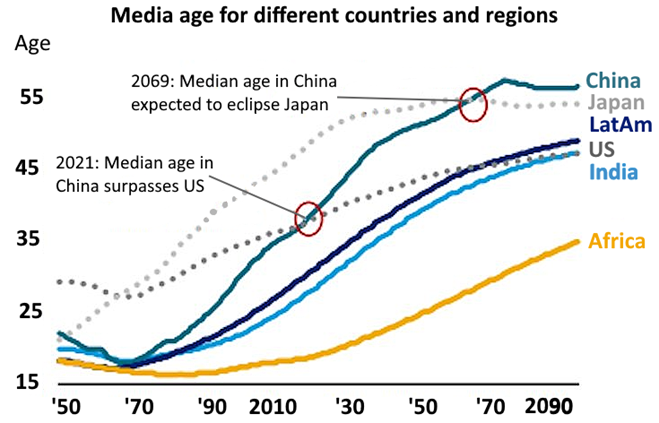

Age – Demographics

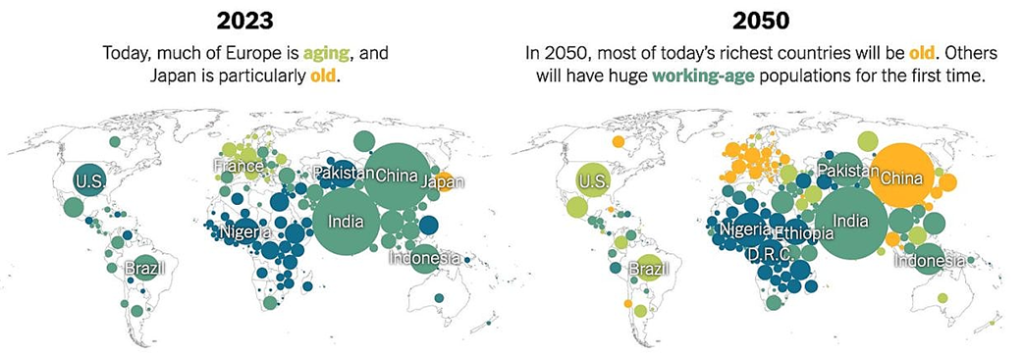

So the question is what will be the most important markets in the next 30 to 60 years? Aging demographics impacts factors such as global order & economic growth. Zinqular data suggests by 2050, people age 65 & older will make up nearly 40% of the population in some parts of East Asia and Europe (refer to Exhibit 43). Today’s wealthier countries will almost inevitably make up a smaller share of global GDP. Emerging markets outside of China will still be young. Much of South Asia and Africa have similar age structures with huge economic upside.

Exhibit 43: Emerging economies outside of China will be important markets in the next 30 – 60 years due to their vibrant young populations.

Favorites & Bottom Ranks

↑ De-Globalization, Regionalization & Localization:

The post-pandemic era has only hastened the rise of emerging trends favoring de-globalization, regionalization, and localization—two forces that, in our view, present significant opportunities for both public and private market investments in the upcoming cycles. We anticipate substantial capital requirements and increased costs as companies strategically position more production closer to consumption. Simultaneously, the region/country of origin is poised to become increasingly pertinent to the development of private market strategies, particularly as supply-side challenges are addressed by both private and public sectors. Consequently, we believe investors in private equity, venture capital, real assets (e.g., real estate and infrastructure), and private credit stand to benefit with adaptable strategies, aligning with the dynamics of the local market. This sets the stage for a new evolving world, emphasizing the value of active ownership, local market expertise, and globally informed multi-asset relative value perspectives.

In 2023, we saw the US importing more from Mexico than China for first time since 2003. But tracing a path forged by Japan & South Korean firms, a high number of Chinese firms are moving to Mexico; establishing factories that allow them to label their products “Made in Mexico,” then trucking these products into the US duty-free. The interest of Chinese manufacturers in Mexico is part of a broader trend known as nearshoring. Caution is warranted as we believe China is still an important player even within the scope of deglobalization/ regionalization. Allocators should bear that in mind.

↑ Geographic Granularity:

We like targeted approach to geographic exposure. In developed markets, Japan captures our interest. We favor India and Mexico in emerging markets (EM) as beneficiaries of major global shifts despite their elevated valuations. Our team at Zinqular holds an optimistic view of the investment climate in Japan. A positive development is the acceleration of capital expenditures, a vital element in bolstering productivity to mitigate the impact of rising wages, as well as increases in food and oil prices. Furthermore, we take note of the continued momentum in corporate reforms, particularly within listed companies, under the current political leadership. Our focus persists on identifying opportunities in corporate carve-outs, and we recognize considerable value in direct transitions from public to private, with a belief in the substantial potential for creating operational value.

↑ Cash Flow Hinged on Collateral Assets:

Despite the heightened need for inflation protection in portfolios, our research underscores that a considerable portion of both individual and institutional investors still maintain suboptimal allocations to Real Assets, notably Infrastructure and Energy. We find optimism in the evolving scope of infrastructure, now encompassing more narratives that revolve around operational enhancements. This additional avenue for value creation becomes particularly advantageous in an environment marked by high or increasing interest rates. Simultaneously, within the Credit sphere, we exhibit a preference for Asset-Based Finance as a strategic move aligned with our “New Economic Outlook” exposition. Despite a moderation in inflation and indications of a more accommodative stance from the Federal Reserve, we argue that the ‘higher for longer’ scenario will persist. Structured products integral to this investment strategy frequently provide funding for traditional Infrastructure and Real Estate assets such as renewable power assets, warehouses and aircraft. Backed by tangible assets that tend to appreciate with consumer prices, these products demonstrate a degree of inflation linkage. Furthermore, their floating coupons can be advantageous for lenders, especially when interest rates are elevated.

↑ Positive Energy/Oil Prices Adjustments:

Oil and gas prices play a crucial role in balancing the energy system by adjusting to changes in supply and demand, ensuring that sources of supply meet fluctuating demand effectively. Foreseeing a shift, we predict a moderation in oil prices to the mid $70-85 range due to a slowdown in global demand and enhanced global supply in 2024. Looking further into the future, our belief persists that ‘ $85 signifies the new $60.’ The ongoing significance of shale as a primary contributor to prolonged global supply growth remains. Producers continue to exhibit a reluctance to augment supply unless prices stabilize at or above $80-85. This forecast differs notably from futures, which consistently embed the expectation of prices declining to $65-74 in 2025 and beyond. Our approach refrain from predicting the price cycles inherent in commodity markets, but we acknowledge the persistent risk of volatility in oil and gas prices. This risk is heightened by the significant transformations necessary to achieve worldwide climate targets.

↑ Opportunistic Credit:

Our team continuously identify substantial value in dynamic and agile liquid credit instruments capable of adjusting allocations across Structured Credit. High Yield, and Levered Loans. This flexibility extends to sectors and themes, capitalizing on pockets of relative value amid shifts in spreads and the risk-free rate. We see absolute returns of these vehicles often rival those of Public Equities, with potentially lower volatility and a more favorable position in the capital structure. Simultaneously, the Private Credit arena presents appealing relative valuations, especially in Asset-Based Finance and Capital Solutions Credit for acquisitions, major expenditures, and domestic re-shoring initiatives.

↑ Embracing Equilibrium on Duration:

We adopt a cautious approach to duration, recognizing the impact of long-term government borrowing on elevating the risk-free cost of capital. However, we see clear value in allowing investors to secure yields resembling cash at the longer end of the curve. In light of historical trends where inverted yield curves tend to resolve through bull steepening, we believe investors may find merit in reducing their overweight exposure to floating rates in 2024. This rationale extends across the risk spectrum, prompting our call for a more balanced strategy between Loans and High Yield.

↑ Residential Mortgages:

Reviewing the data, we see banks are originating much fewer mortgages and the Federal Reserve is selling its mortgage holdings, we observe occasional indiscriminate selling. Remarkably, despite overall improvements in quality, we anticipate a strong performance from prime consumers in this economic cycle. This presents a compelling context, and we advise seizing any market downturns to build positions, particularly beneficial for investors with fixed liabilities such as pension funds and insurance companies.

↑ Short-Term (< a Year) Lending Strategies:

We overall prefer short term bonds over long term. That’s due to more uncertain and volatile inflation, heightened bond market volatility and weaker investor demand. In the scenario where the Fed implements rate cuts more slowly than market expectations, the return provided by the shorter end of the yield curve will play a significant role in influencing performance throughout 2024. Our specific focus lies on sub-lines, presenting an avenue to garner enhanced compensation for engaging with top-tier counterparts in a domain where regional banks have scaled back on fresh lending.

↑ Data-centers & Energy Infrastructure Fueling AI:

The surge in demand for cloud infrastructure, data centers, semis and hardware will continuously pique our interest across within our platform. The team at Zinqular is of the view that ongoing AI surge will significantly impact escalating energy requirements for training AI models (while high portion of investors concentrate on the semiconductor facet). The fact remains that, in numerous cases, the existing infrastructure falls short of meeting the necessary demand. In light of this situation, our optimism extends to vital energy transmission assets, data centers, and cooling technologies.

↓ Commercial Office Property:

In the current landscape, office capitalization rates remain notably elevated, surpassing those seen in the data center and multifamily sectors by nearly 175 basis points. Despite this discrepancy, we assert that investors in office commercial real estate (CRE) are not receiving commensurate compensation for the inherent volatility in revenues. This assessment is particularly relevant given the ongoing decline in occupancy rates and the gradual absorption of sublet space. While certain sectors face cyclical challenges, we’ve identified emerging opportunities in Industrials, data centers, and Single-Family Rentals. These sectors boast wider average cap rates than two years ago.

↓ Possibility of Fed Rate Cuts:

Our stance differs from the market expectation embedded in forward markets, suggesting the Fed will implement nearly six rate cuts in 2024. It’s crucial to recall the Fed’s aim of maintaining real rates at or above two percent until inflation stabilizes at the target sustainably. Given our assessment indicating a potential decline in inflation to the mid-two percent range in 2024, it becomes apparent that maintaining a nominal rate close to four percent could lead to an excessive level of accommodation in real terms within the prevailing market dynamics

↓ Waning Impact of Inverted Yield Curves:

Given the structural pressures observed in the treasury market, notably the surplus supply and the diminishing foreign interest in USTs, we anticipate a tempered rally in bonds relative to historical trends following rate cuts by the Federal Reserve. Based on our term premium model, it is evident that the prevailing 10-year yields within the market are heavily impacted by enduring structural elements. These elements, encompassing broader deficits, diminishing savings rates, and favorable stock-bond correlations, are anticipated to endure in the short to medium term, shaping investment strategies. As we analyze the dynamics in the short-term sector, we anticipate that the Federal Reserve will retain a degree of maneuverability to implement multiple rate cuts throughout 2024, albeit potentially fewer than market expectations. This strategic move is poised to contribute to a broader yield curve steepening trend, offering nuanced opportunities within the private equity landscape.

↓ Intersection of Credit & Non-Control Equities:

In the backdrop of sluggish nominal growth, there’s a notable trend of reduced pressure on bond yields. This shift is fostering a more vibrant atmosphere within capital markets, prompting increased participation. While improvements are evident, a notable number of financially vulnerable companies with weak capital structures are expected to face the imperative of refinancing in the coming quarters. Echoing our perspective from the previous year, our strategy for 2024 remains rooted in simplicity, steering clear of excessive pursuit of quality. The marginal increase in yield observed in the lowest-rated unsecured High Yield, for instance, does not align with the perceived risks, in our assessment. Given this context, we foresee a considerable amplification in the distinction between control and non-control stakes throughout 2024. The heightened valuation of assets demands intensified focus on operational enhancements and the adept reshaping of companies’ capital structures, particularly as lending markets show signs of recovery.

↓ Non-Core U.S. Consumer Segment:

Our analysis indicates that segments of the younger demographic and individuals with lower income brackets in the United States have faced heightened exposure to inflationary pressures during this economic cycle. Consequently, there is a growing dependence among these cohorts on credit instruments such as credit cards and loans to bridge financial gaps. In contrast, a significant portion of ‘core’ U.S. consumers, including homeowners, remains relatively resilient. This resilience is attributed to factors such as fixed-rate mortgages, a manageable overall debt burden, and a substantial reservoir of excess savings, all contributing to sustained spending. Against this backdrop, our expectation is that a considerable portion of the deceleration in consumer spending and the increase in consumer distress during this economic cycle will unfortunately be concentrated among lower-income households, particularly if our observation of a slowdown in the labor market comes to fruition.

↓ Unsecured Credit Dynamics:

our data unveils a discernible pattern in consumer financial behaviors. It suggests a prioritization of critical expenses such as mortgage commitments and essential utilities over discretionary spending on items like unsecured loans. It is crucial to note that our central scenario anticipates a relatively mild rise in unemployment during this cycle, with an expected increase of 125 basis points. This is notably lower than the historical norm, which typically witnessed elevations of 300-400 basis points in previous cycles. Despite the overall positive outlook in the private equity markets relative to prior cycles, there is a shared concern that certain lenders may have pushed the boundaries of prudence during the period of heightened spending following the post-COVID recovery. We anticipate the lenient lending practices during the spending surge are expected to have repercussions, particularly in cases without a direct claim on collateral.

↓ U.S. Regional Banks:

Despite U.S. regulators’ strong commitment to the health of the regional banking system, we anticipate that regional banks could be compelled to offer higher rates for deposits. This comes at a time when they are grappling with substantial losses on their real estate lending portfolios. Concurrently, regulatory challenges are incentivizing banks to seek ways to diminish their risk-weighted assets, resulting in a diverse array of changes to their assets and portfolios. Although we don’t predict a full-scale meltdown akin to the 1990’s Savings & Loans crisis, we do foresee ongoing distress in the system, exacerbated by elevated borrowing costs that impact net income margins.

Next Week Check Out Part C – Sunny Side of Shifting Currents: Global Investment & Economic Outlook 2024 Exposition