Authors:

Conrad Thomas Walker – Partner & Senior Managing Director

Barry Simon Graham – Senior Managing Partner & Global Co- Chief Investment Officer

Michael Yaw Appiah – Senior Managing Partner & Global Co-Chief Investment Officer

Sheau pei Chong – Chief Operating Officer – Asia & Senior Managing Director

Felix Cederberg – Head of Energy & Climate Infrastructure

Andrew Thompson – Vice President – North America, Infrastructure

Executive Summary

For over a century and a half, the global economy has been inextricably linked to the Crude Oil Paradigm. This system, built upon four fundamental pillars, i.e., cheap extraction, massive storage, efficient transportation, and universal accessibility; transformed oil from a simple commodity into the geopolitical and economic lifeblood of the modern world. It fueled the Industrial Age, enabled globalization, and dictated the pace of human progress, creating a dynamic, fungible, and globally-traded ecosystem that remains the benchmark for all essential resources.

Today, the world stands at the precipice of a transition to a new, equally transformative system: the Electricity Paradigm. Driven by technological breakthroughs in generation, storage, and transmission, electricity is shedding its historical limitations as a non-storable, localized resource. It is evolving into a globally-tradable, highly-efficient, and universally-accessible commodity that will power the next 100 years of global economic expansion. This concept paper posits that the electricity ecosystem has now achieved the same four pillars of dominance that defined crude oil’s 150-year reign.

The transformation is not merely an upgrade; it is a complete overhaul. The paper details how:

- Cheap Power from hyper-efficient renewables and next-generation nuclear is replacing the low-cost extraction of crude.

- Massive Storage (from long-duration batteries to thermal and pumped hydro) is creating the essential buffer, analogous to the Strategic Petroleum Reserve, decoupling generation from consumption.

- Ultra-Efficient Transmission via High-Voltage Direct Current (HVDC) and Ultra-High-Voltage Direct Current (UHVDC) is creating a global pipeline, solving the problem of energy loss over distance and enabling the seamless flow of power across continents.

- Universal Accessibility through smart grids and microgrids is ensuring that this cheap, reliable power is available to every industrial, commercial, and retail consumer.

This transition will unleash an economic shockwave, requiring the replacement or fundamental upgrade of over 80% of all legacy electricity infrastructure—a global investment opportunity estimated to exceed $25 trillion by 2050. This capital expenditure will be the primary driver of global GDP growth for decades, powering the electrification of transport, industry, and the exponential energy demands of the Artificial Intelligence (AI) revolution.

The paper highlights how one nation, through centralized strategic planning and unparalleled investment, has already constructed the blueprint for this new ecosystem. This Pioneer Nation has demonstrated the feasibility of a continent-spanning, ultra-efficient grid, setting a new, inevitable standard for all G10 and G20 economies. Finally, the paper introduces Zinqular Investment Partners, a firm that has prioritized specialized private funds dedicated to providing alpha-sized exposure to institutional investors. Zinqular’s strategy is built on the conviction that the infrastructure required for the Electricity Paradigm represents the most compelling, long-term, and defensive investment opportunity of the 21st century.

.

The Crude Oil Paradigm (1860-2025) – The Engine of the First Industrial Century

The history of the modern global economy is, in large part, the history of crude oil. For approximately 150 years, beginning with the commercial drilling of the Drake Well in Pennsylvania in 1859, petroleum ascended from a novelty to the single most important commodity on Earth. Its dominance was not accidental; it was the result of a perfectly engineered, globally-scaled ecosystem that allowed for the cheap, reliable, and ubiquitous delivery of energy. This system, which we term the Crude Oil Paradigm, established the structural template against which the emerging Electricity Paradigm must be measured.

The Birth of the Oil Economy

The initial demand for petroleum was driven by the need for a superior illuminant to whale oil, leading to the rise of kerosene [1]. However, the true global dominance of crude oil began with the invention of the internal combustion engine and the subsequent mass production of the automobile in the early 20th century. This shift transformed the primary product from kerosene to gasoline and diesel, creating a massive, inelastic demand for liquid fuels that would power the transportation, industrial, and military sectors of the world [2].

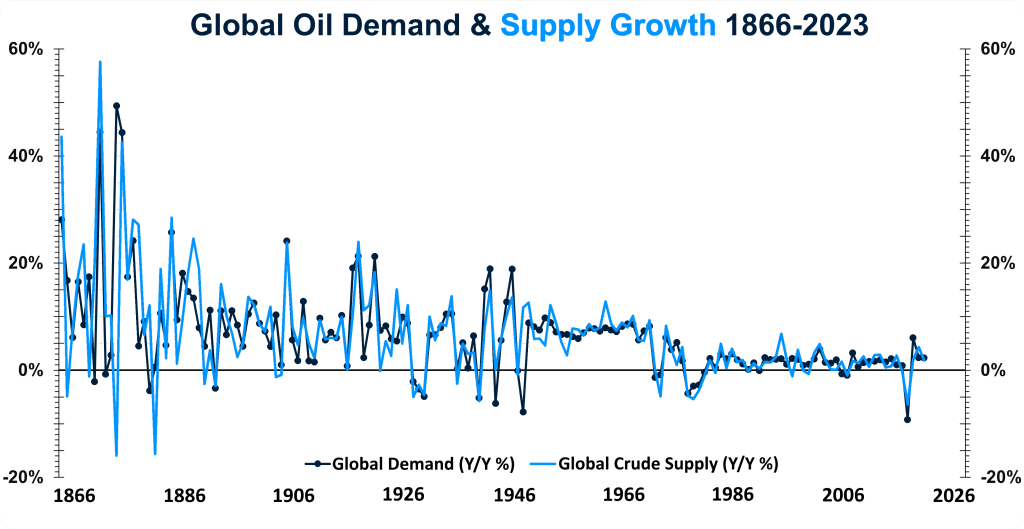

Exhibit 1: Tracing a Century and a Half of Oil Market Cycles: Demand and Supply Growth Compared

The early 20th century saw the consolidation of the industry under entities like Standard Oil, followed by the discovery of vast, easily accessible reserves in the Middle East and elsewhere after World War II. This geopolitical shift, coupled with the establishment of organizations like OPEC, cemented crude oil’s role as a strategic asset, intertwining energy security with national security and international relations [3]. The ability of this system to scale with the exponential growth of the global population and industrial output is the core reason for its enduring legacy.

The Four Pillars of Crude Oil’s Dominance

The success of the Crude Oil Paradigm can be structurally decomposed into four interconnected pillars, each of which contributed to its status as a dynamic, globally-traded commodity.

Pillar 1: Cheap Extraction (Production)

The foundation of the Crude Oil Paradigm was the ability to produce massive volumes of crude at a remarkably low marginal cost. This was achieved through the discovery and exploitation of vast, concentrated, and relatively shallow reserves, particularly in the Middle East, Russia, and the Gulf of Mexico.

The historical abundance of easily accessible reserves… kept costs low for decades, enabling the unprecedented industrialization of the 20th century. [4]

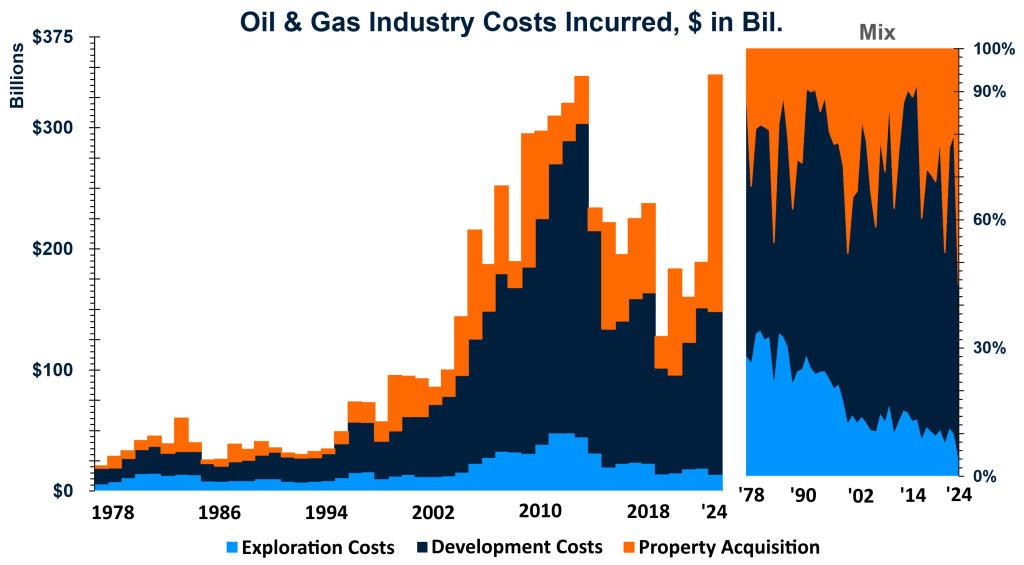

Exhibit 2: Five Decades of Rising Oil & Gas Costs: Exploration, Development & Acquisition Trends. From Boom to Bust: How Industry Spending Has Shifted Since the 1970s

The cost of production is measured by the lifting cost; the expense of bringing a barrel of oil to the surface. For decades, the lifting cost in the most prolific fields remained exceptionally low, often under $10 per barrel. This low cost created an enormous economic surplus that was reinvested, driving down the price of energy and fueling global economic growth. While modern techniques like hydraulic fracturing and deep-water drilling have increased the complexity and cost of extraction, the historical precedent of cheap, abundant supply remains the defining characteristic of this pillar. The sheer energy density of crude oil, combined with the relative ease of its initial extraction, provided an insurmountable advantage over other energy sources for over a century.

Pillar 2: Massive Storage (The Buffer)

Unlike electricity, which historically had to be consumed the instant it was generated, crude oil is highly storable. This simple physical property is the key to its commodity status and its geopolitical power. Storage infrastructure, including onshore tank farms, floating storage on massive tankers, and underground caverns for Strategic Petroleum Reserves (SPR), acts as a critical buffer between volatile production and steady consumption.

The ability to store billions of barrels allows the market to absorb supply shocks, manage seasonal demand fluctuations, and, most importantly, provides nations with a strategic security blanket [5]. This decoupling of production from consumption is what allows oil to be traded as a true commodity, with futures markets and global pricing mechanisms. The existence of the SPR, for instance, is a direct acknowledgment that the physical storage of the commodity is a matter of national economic security.

Pillar 3: Efficient Transportation (The Global Pipeline)

The third pillar is the development of a vast, highly efficient, and globally interconnected transportation network. The system is characterized by its ability to move enormous volumes of crude oil and refined products over vast distances with minimal loss.

The primary modes of transport are:

- Pipelines: The most cost-effective and low-loss method for long-haul, high-volume transport of crude oil from production fields to refineries. Sophisticated monitoring and valve systems ensure that “not a drop of crude is lost” during this phase, a critical point of comparison to the historical losses in electricity transmission [6].

- Seaborne Cargo: Massive crude oil tankers (VLCCs and ULCCs) form the backbone of global trade, moving oil across oceans from exporting nations to consuming nations. This seaborne network ensures that oil is a truly global commodity, instantly tradable and transportable to any coastal region.

- Rail and Truck: Used primarily for shorter distances and final distribution of refined products.

This multi-modal, low-loss transportation system is what transformed regional oil fields into a globalized ecosystem, ensuring that supply could meet demand anywhere in the world, regardless of geography.

Pillar 4: Universal Accessibility

The final pillar is the seamless and ubiquitous accessibility of the final product to the consumer. Crude oil is refined into a range of products—gasoline, diesel, jet fuel, heating oil, and petrochemical feedstocks—at centralized refineries. These products are then distributed through a dense network of terminals, blending facilities, and, most visibly, the global network of retail gas stations.

The genius of this system lies in its ubiquity and ease of consumption. The final consumer, whether an industrial plant, a commercial airline, or a private motorist, can access the energy source instantly and utilize it with existing, standardized infrastructure (the internal combustion engine). This seamless integration into the daily lives and industrial processes of the world is the ultimate measure of the Crude Oil Paradigm’s success.

The Economic & Geopolitical Legacy

The Crude Oil Paradigm did more than just power the world; it shaped its political and economic structure. The availability of cheap, dense, and transportable energy was the catalyst for the post-war economic boom and the subsequent era of globalization. However, this dependence also created significant vulnerabilities.

The oil crises of the 1970s, triggered by geopolitical events, demonstrated the global economy’s profound sensitivity to disruptions in the oil supply chain, leading to stagflation and recessions across the developed world [7]. This legacy underscores a fundamental truth: control over the dominant energy commodity is control over the global economy.

The next chapter will detail how the Electricity Paradigm is now poised to replicate and surpass this structural dominance, creating a new, more resilient, and more powerful engine for the 21st century.

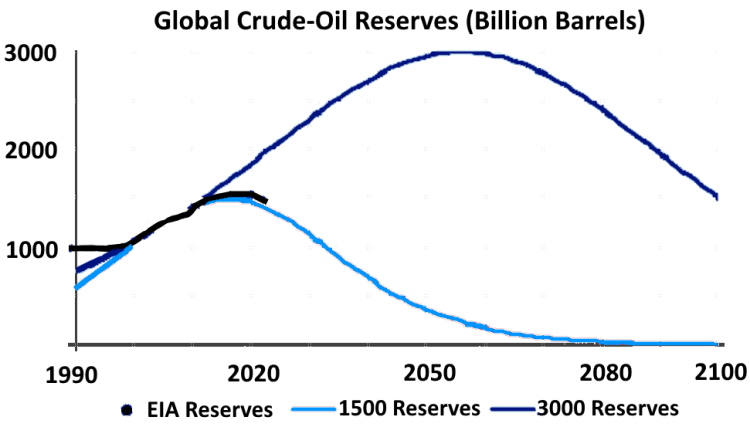

Exhibit 3A: All Trajectories Converge Toward Very Low Reserves by 2100

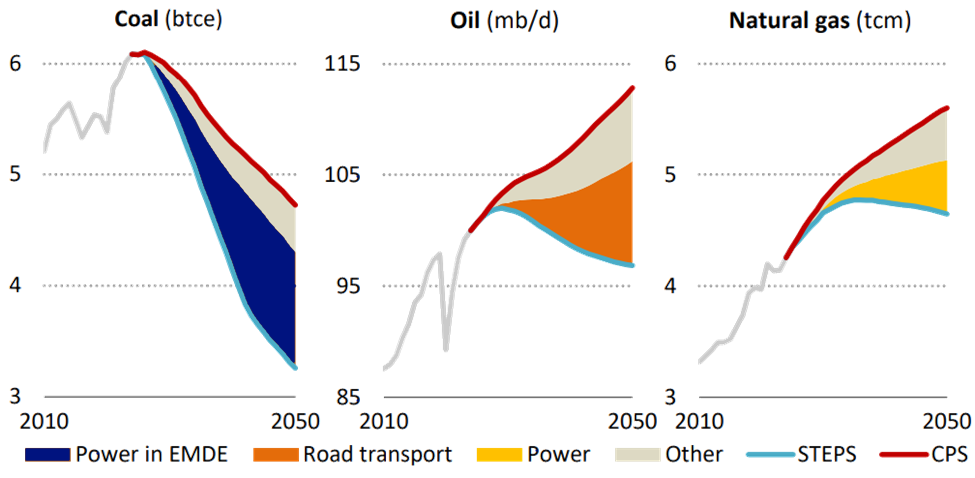

Exhibit 3B: Coal & Oil Demand Peak by 2030 in the Steps; Growth is Higher in the CPS Due to Slower Uptake of Technologies Such as Renewables & EVs

.

The New Electricity Paradigm – The Engine of the Next Century

The world is transitioning from a liquid-fuel-based economy to an electron-based economy. If our assessment is correct, this transition will unfold over several decades. This shift is not merely a change in fuel source; it is a fundamental re-engineering of the global energy infrastructure, driven by technological advancements that have finally overcome the historical limitations of electricity. For the first time, electricity can be generated cheaply, stored massively, and transmitted efficiently over vast distances, achieving the same four pillars of dominance that defined the Crude Oil Paradigm.

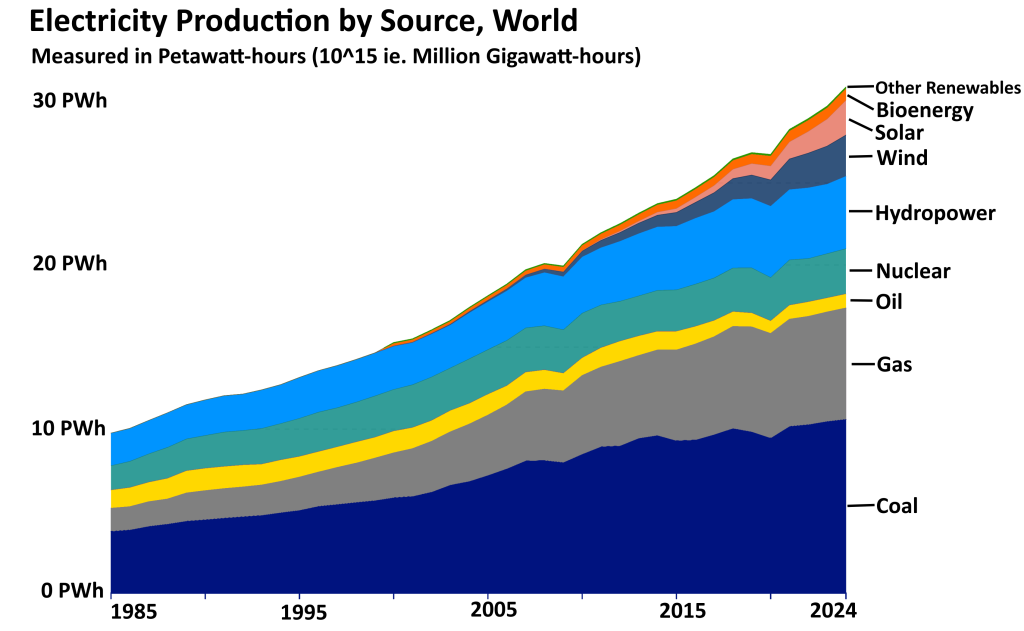

Exhibit 4: Global Electricity Production Has More Than Doubled Since 1985, Rising From Under 10 Pwh To Nearly 30 Pwh By 2024—Showing Both Population Growth And Increasing Electrification.

The Imperative for Transformation

The legacy electricity grid, largely built in the mid-20th century, was designed for a centralized, one-way flow of power from large thermal power plants to passive consumers. It was an Alternating Current (AC) system, inherently inefficient for long-distance transmission and fundamentally incapable of handling the variable nature of modern renewable energy sources.

The transformation is mandated by two converging forces: the decarbonization imperative and the exponential growth of new demand. The electrification of transport (Electric Vehicles, e-trucks) and industry (electric furnaces, heat pumps) is dramatically increasing the total share of energy consumption accounted for by electricity. More critically, the rise of Artificial Intelligence (AI) and the associated massive data centers are creating an unprecedented, inelastic demand for reliable, high-density power.

The energy requirements of Large Language Models (LLMs) and the AI revolution are creating a demand multiplier that the legacy grid simply cannot support. The need for ‘Always-On’ power is the ultimate stress test for the new system. [8]

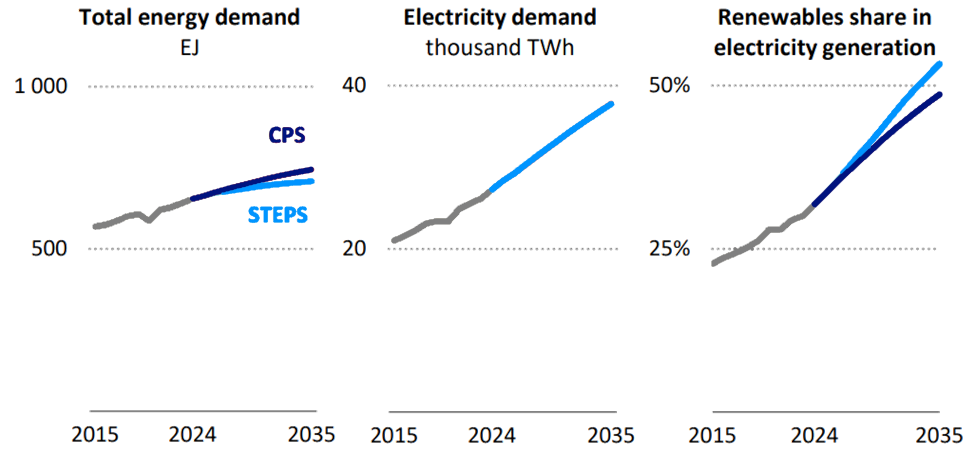

Exhibit 5: Electricity Demand Outpaces Total Energy Demand Growth By A Wide Margin; Renewables Account For An Increasing Share Of Surging Electricity Demand

The Four Pillars of the New Electricity Ecosystem

The New Electricity Paradigm is built on a foundation that mirrors the structural integrity of the crude oil ecosystem, transforming electricity into a storable, transportable, and globally accessible commodity.

Pillar 1: Cheap Power (Generation)

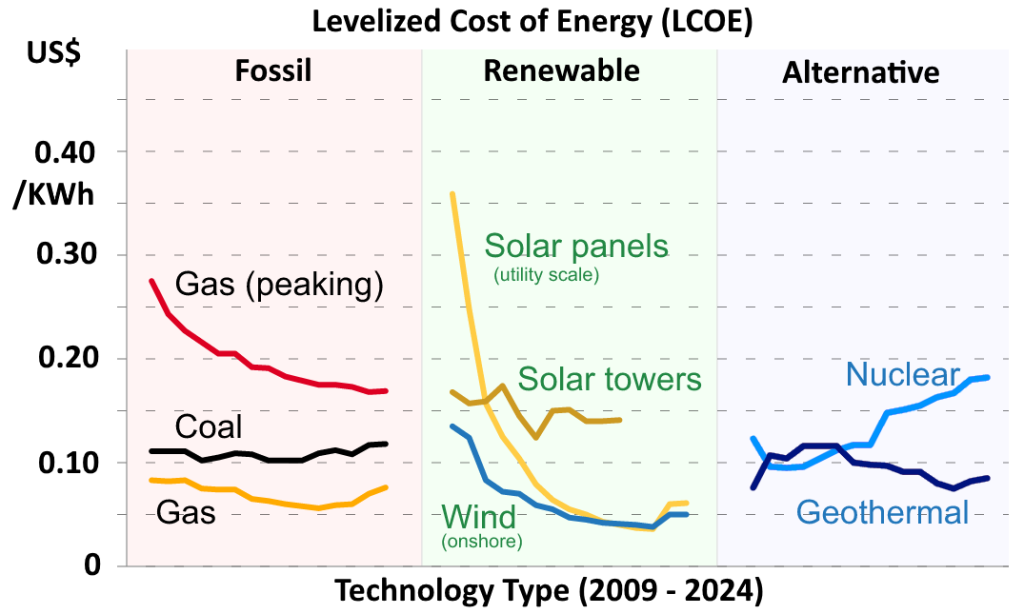

The equivalent of cheap crude extraction is the dramatic reduction in the Levelized Cost of Energy (LCOE) for renewable sources, particularly solar and wind. In many regions, new utility-scale solar and wind farms now offer the cheapest source of bulk power generation in history, undercutting the operational costs of existing fossil fuel plants [9].

The new generation mix is characterized by:

- Hyper-Efficient Renewables: Continuous innovation in photovoltaic cell efficiency and wind turbine design has made these sources the economic default for new capacity.

- Hard Sources for Resilience: Nuclear, Hydro, and Geothermal provide the essential, dispatchable, and high-capacity factor baseload power that stabilizes the grid. This diverse portfolio ensures that the system is not reliant on a single fuel source, offering a resilience that the oil-dependent economy lacked.

- Decentralization: The ability for power to be generated at the point of consumption (rooftop solar, micro-turbines) adds a layer of resilience and cost-efficiency that was impossible in the centralized oil model.

Exhibit 6: Energy Economics Rewritten: How Renewables Became The Cheapest Power Source (The Economic Turning Point)

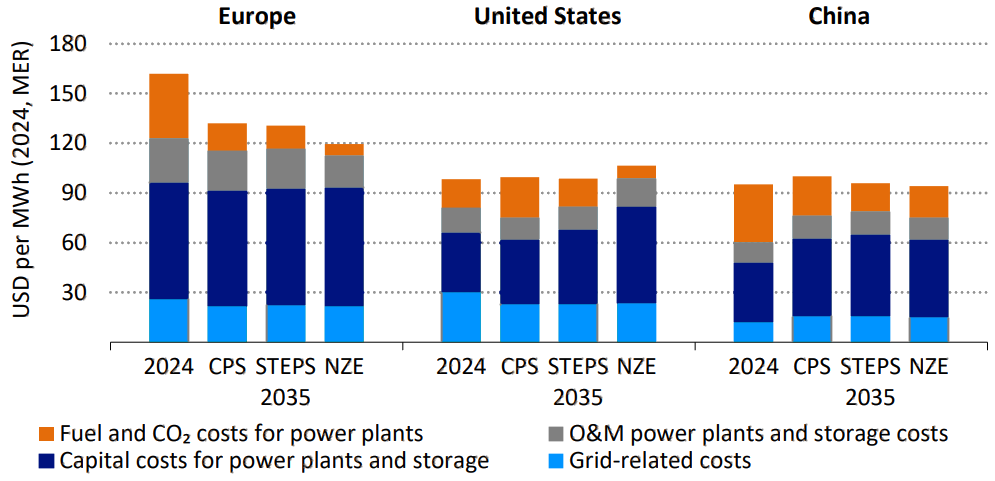

Exhibit 7: The Transformation Of Electricity Systems Entails A Shift In Cost Structure, From Fuel And Operational Expenses Towards Upfront Investments In Clean Technologies And Infrastructure

Pillar 2: Massive Storage (The Decoupling Factor)

Storage is the single most critical breakthrough, transforming electricity from a flow to a stock. This pillar is the direct analogue to the Strategic Petroleum Reserve, allowing for the decoupling of generation from consumption and creating a true commodity market for electrons.

The scale of storage is moving from hours to days and even seasons, utilizing a diverse portfolio of technologies:

- Utility-Scale Batteries: Enhanced Lithium-ion and Flow Batteries provide the necessary short-duration (4-8 hour) flexibility for daily grid management.

- Long-Duration Storage (LDS): These technologies are the game-changer, enabling regional and country-level energy security.

- Thermal Storage: Systems like the “sand battery” (e.g., in Finland) and molten salt systems store excess renewable energy as heat for later conversion back to electricity, offering a low-cost, long-life solution [10].

- Alternative Chemistries: New battery chemistries (e.g., Al-Ni molten salt) and gravity-based systems are being developed for seasonal storage, ensuring supply during periods of low renewable output.

- Pumped Hydroelectric Storage (PHS): Remains a dominant form of large-scale storage, often utilizing existing dam infrastructure.

Pillar 3: Ultra-Efficient Transmission (The Global Pipeline)

The historical problem of electricity transmission was the significant energy loss (up to 8-10% over long distances) inherent in the AC system. The solution, and the third pillar of the new ecosystem, is the global adoption of High-Voltage Direct Current (HVDC) and Ultra-High-Voltage Direct Current (UHVDC) transmission.

HVDC technology is highly efficient for transmitting large amounts of electricity over long distances, with losses reduced to as low as 3% per 1,000 kilometers [11]. This technological leap is the equivalent of the low-loss oil pipeline network, allowing power to be generated in the most resource-rich locations (e.g., sunny deserts, windy plains) and delivered to distant consumption centers with minimal waste.

HVDC is a key enabler for a carbon-neutral energy system. It is highly efficient for transmitting large amounts of electricity over long distances, allowing for the creation of a resilient, interconnected super-grid. [12]

The development of UHVDC, capable of transmitting up to 10 GW of power, is the final piece of the puzzle, enabling the creation of continent-spanning “super-grids” that can balance supply and demand across vast geographical areas, further enhancing reliability and reducing cost.

Pillar 4: Universal Accessibility

The final pillar is the seamless integration of this cheap, reliable, and transportable power into the consumer ecosystem. The new system is defined by the Smart Grid, which uses digital communication technology to manage the flow of power in two directions, accommodating both centralized and decentralized generation.

- Microgrids and Resilience: Localized microgrids increase resilience by allowing communities and industrial parks to operate independently during grid failures.

- Consumer Integration: The consumer is no longer a passive recipient but an active participant. Technologies like Vehicle-to-Grid (V2G) allow electric vehicles to act as mobile storage units, feeding power back into the grid during peak demand, further stabilizing the system and reducing the final cost of energy.

The convergence of these four pillars means that electricity is no longer a localized, perishable utility. It is a globally-scalable, storable, and transportable commodity—the new engine of the global economy.

.

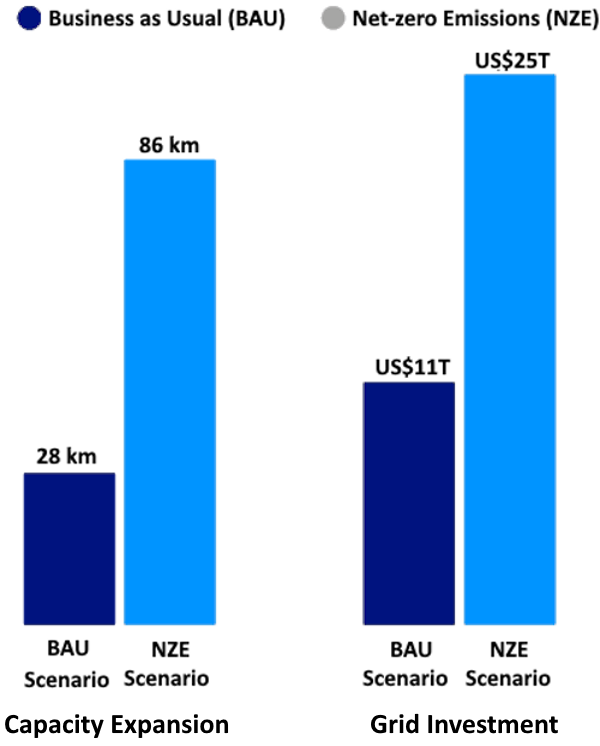

The Economic Shockwave – $25 Trillion in Infrastructure Replacement

The transition to the Electricity Paradigm is not a gradual evolution; it is a massive, capital-intensive undertaking that will generate the largest sustained wave of infrastructure investment in human history. The sheer scale of the required capital expenditure—estimated to be over $25 trillion globally by 2050—will act as a powerful, multi-decade stimulus, driving global GDP growth and fundamentally restructuring the industrial landscape [13].

Exhibit 8: By 2050, The Global Power Grid Faces a Massive Investment & Expansion Shortfall of US$25 Trillion

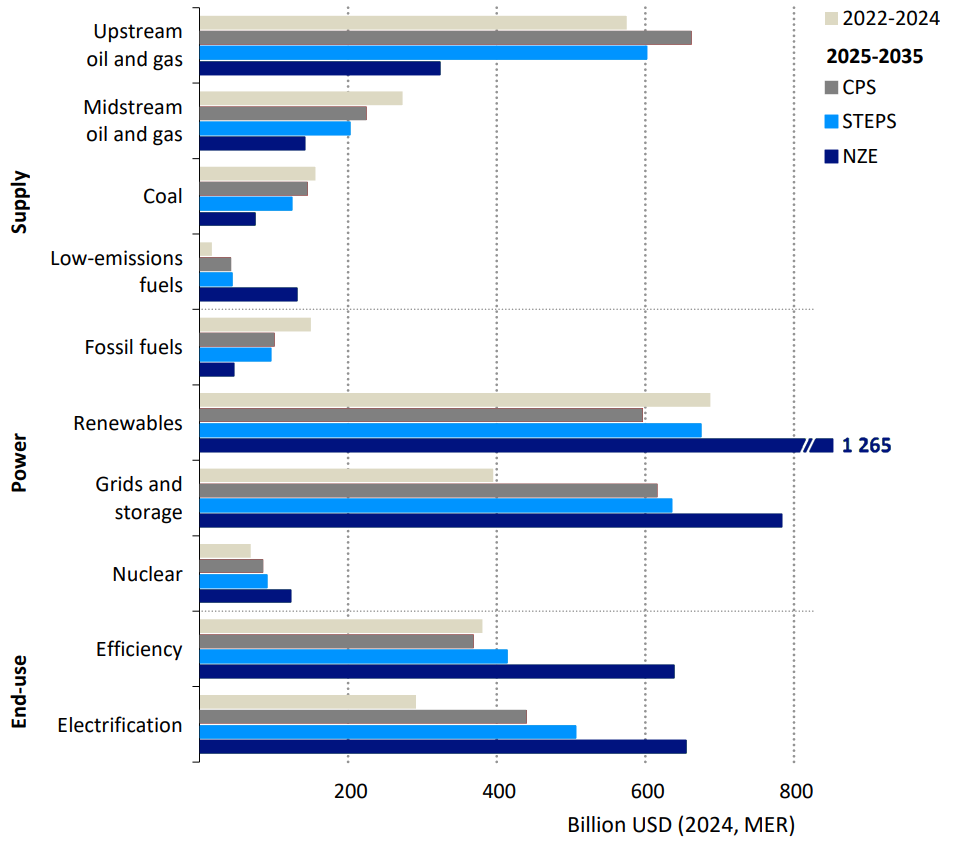

Exhibit 9: As The Age Of Electricity Emerges, Investment Shifts From Fossil Fuels Towards Low-Emissions Power Generation And Fuels, Grids And Storage, And End-Use Electrification

The Scale of Obsolescence

The central economic reality of the transition is that the existing global electricity infrastructure is largely obsolete. Built for a different era, the legacy grid is too fragile, too lossy, and too centralized to handle the demands of a modern, electrified, and decarbonized economy.

Over 80% of all legacy electricity ecosystem infrastructure requires replacement or fundamental upgrade to meet the demands of the New Electricity Paradigm.

Exhibit 10: Many Advanced Economies Have Ageing Grid Infrastructure In Need Of Modernisation, Emerging Market And Developing Economies Have Newer Grids. Grid Length By Type, Age And Region/Country, 2024

This 80% replacement figure is driven by the need to:

- Replace AC Transmission with HVDC/UHVDC: The existing AC transmission lines are simply too inefficient for the long-distance transport of power from remote renewable hubs. New corridors and converter stations must be built from the ground up.

- Integrate Massive Storage: The grid needs to be re-engineered to handle the two-way flow of power and the rapid charge/discharge cycles of utility-scale storage facilities, which did not exist in the original design.

- Modernize Distribution: Local distribution networks (the “last mile”) must be upgraded with smart grid technology, sensors, and digital controls to manage decentralized generation and consumer-side storage.

- Electrify End-Use: The infrastructure at the point of consumption—from industrial furnaces to residential heating systems and vehicle charging networks—must be completely overhauled to run on electricity rather than fossil fuels.

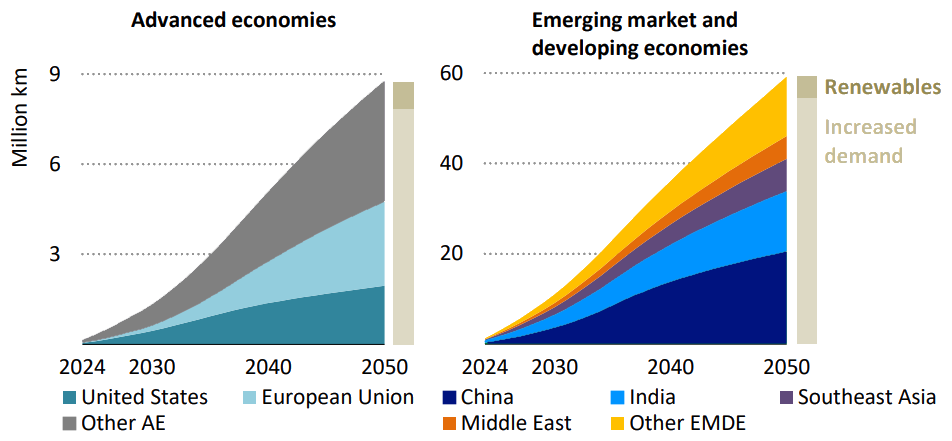

Exhibit 11: Most New Lines Are Installed To Meet Increased Demand; Nearly 90% Of All New Lines Are In Emerging Market And Developing Economies. Expansion Of Grid Lines By Driver In Selected Region/Country In The Cps, 2024-2050.

Exhibit 12: More Than 45 Million Km Of Grid Line Are To Be Replaced By 2050, Accounting For 40% Of All Cumulative Grid Additions, Of Which More Than Two-Thirds Are In Advanced Economies. Grid Line Replacement By Selected Region/Country And Replacement Share Of Grid Additions In The Cps, 2024-2050

Exhibit 13: Grid Investment Rises In Nearly All Regions To Modernise And Expand Transmission And Distribution To Meet Rising Electricity Demand And To Connect New Sources Of Generation. Average Annual Grid Investment By Economic Grouping In The Cps To 2035.

The AI & Data Center Demand Multiplier

The most urgent and demanding driver of this infrastructure build-out is the exponential growth of Artificial Intelligence (AI). The training and operation of Large Language Models (LLMs) and the vast data centers that house them require an unprecedented amount of power.

| Metric | Legacy Data Center (2015) | AI Data Center (2025) | Growth Factor |

| Power Density | 5-10 kW per rack | 50-100+ kW per rack | 10x |

| Annual Consumption | 1-5 TWh per facility | 10-20+ TWh per facility | 4x |

| Reliability Requirement | 99.99% (Tier III) | 99.999% (Tier IV equivalent) | Critical |

The AI revolution demands not just power, but perfectly reliable power. This requirement elevates the importance of the storage pillar to a matter of economic survival for the technology sector. Data centers are increasingly being located near major renewable generation and storage hubs, making power availability the new factor of production, replacing proximity to fiber optic lines or cheap land. The need for this “Always-On” power is accelerating the deployment of new, dedicated generation and storage infrastructure at a pace unseen since the early days of the oil boom.

Electrification of the Global Economy

Beyond AI, the wholesale electrification of the global economy is driving the investment mandate.

Transportation:The shift from the internal combustion engine (ICE) to Electric Vehicles (EVs) is a direct transfer of demand from the Crude Oil Paradigm to the Electricity Paradigm. This requires a massive build-out of charging infrastructure, but more fundamentally, it requires the grid to handle a massive, flexible load. The integration of EVs, however, also presents an opportunity, as V2G technology can transform millions of parked cars into a distributed storage network, further stabilizing the grid.

Industry: Heavy industry, which has historically relied on the high heat generated by burning fossil fuels, is transitioning to electric processes. This includes:

- Green Steel: Using electric arc furnaces powered by renewable electricity.

- Green Hydrogen: Electrolysis powered by cheap, excess renewable electricity to create hydrogen for industrial processes and long-haul transport.

- Industrial Heat: Replacing gas boilers with high-efficiency electric heat pumps and thermal storage solutions.

This wholesale shift means that electricity’s share of final energy consumption will rise dramatically, making the efficiency and reliability of the new grid the single most important determinant of national economic competitiveness.

Macroeconomic Impact

The $25 trillion investment wave will have profound macroeconomic effects:

- GDP Growth: The sustained capital expenditure on infrastructure will be a powerful, non-cyclical driver of GDP growth in developed and developing nations alike.

- Deflationary Energy: As the LCOE for renewables continues to fall and the efficiency of transmission and storage increases, the marginal cost of electricity will trend downward. This creates a deflationary effect on the economy, as the cost of the most fundamental input i.e., energy; becomes cheaper and more stable.

- Geopolitical Stability: The shift to a decentralized, domestically-generated, and storable energy source fundamentally reduces reliance on volatile, geopolitically sensitive fossil fuel supply chains, leading to greater national energy security and stability.

.

The Blueprint for the Future – China’s Transformation & the New Global Standard

The transformation of the electricity ecosystem from a localized utility to a global commodity has not been a theoretical exercise; it has been a reality in one Pioneer Nation that has strategically invested in and deployed the complete four-pillar system at a continental scale. This nation, which has recreated the dynamic of the crude oil ecosystem for electricity, is China. Its success is not merely a domestic achievement but a blueprint for the rest of the G10 and G20 countries seeking energy security, economic growth, and decarbonization.

The Strategic Vision: From Coal Dependency to Global Grid Leader

China’s energy strategy has been defined by two major challenges: a massive, rapidly growing energy demand and the geographic mismatch between its vast renewable resources (wind and solar in the West) and its industrial and population centers (the coastal East). The solution was a centralized, state-led commitment to building a national super-grid capable of transporting power over thousands of kilometers.

This vision was formalized through massive, long-term planning that viewed the grid not as a utility, but as a strategic national asset; the electronic equivalent of a national highway system or a strategic oil pipeline network. This policy framework enabled the rapid deployment of capital and the overcoming of regulatory hurdles that plague grid modernization efforts in Western democracies.

The UHVDC Revolution: The New Global Standard

The core technological enabler of China’s success is its pioneering and world-leading deployment of Ultra-High-Voltage Direct Current (UHVDC) transmission. While HVDC was a known technology, China scaled it to unprecedented levels, creating what has been dubbed the “bullet train for power” [14].

| UHVDC Project Example | Voltage (kV) | Capacity (GW) | Length (km) | Key Feature |

| Changji-Guquan | ±1100 | 12 | 3,324 | World’s highest voltage and longest transmission line. |

| Xianjiaba-Shanghai | ±800 | 6.4 | 1,907 | Connects hydro power from the Southwest to the East Coast. |

| Jiuquan-Hunan | ±800 | 8 | 2,383 | Connects massive wind/solar bases to central China. |

These UHVDC lines solve the problem of electricity loss over distance, achieving transmission efficiencies of over 97% [15]. This is the direct, functional equivalent of the low-loss oil pipeline, transforming power generated in remote, resource-rich areas into a cheap, reliable input for distant industrial hubs. This capability is the single most important factor in creating the “cheap power” pillar at the national level.

The Scale of Renewable Integration

The UHVDC network is the backbone that allows China to integrate the world’s largest and fastest-growing fleet of renewable energy assets. China produces more clean energy than any other country, with massive, multi-gigawatt solar and wind farms built in the Gobi Desert and other remote regions [16].

The strategic genius lies in the simultaneous build-out of generation and transmission. The UHVDC lines were built to the renewable bases, guaranteeing a path to market for the power and thus de-risking the massive private and state investment in generation. This coordinated approach has driven down the LCOE for renewables within China to world-beating levels.

Furthermore, China has recognized the critical role of storage in stabilizing this variable supply. Significant investment has been channeled into utility-scale battery storage and the development of long-duration solutions, ensuring that the power transmitted via UHVDC is dispatchable and reliable, thereby achieving the “massive storage” pillar.

The New Standard for G10 & G20 Countries

The Chinese model is not merely a local solution; it is the inevitable standard for all major economies. G10 and G20 nations face the same fundamental challenges: aging, inefficient grids, the need to integrate remote renewable sources (e.g., offshore wind, desert solar), and the massive new demands from electrification and AI.

The key takeaways for the rest of the world are:

- Centralized, Long-Term Planning: The success of the UHVDC build-out demonstrates that grid modernization cannot be achieved through piecemeal, localized efforts. It requires a national or even continental strategic vision.

- UHVDC as the Default: For any long-distance transmission, UHVDC is no longer an option but a necessity to achieve the efficiency and low-loss rate required for a commodity-grade electricity system.

- Coordinated Build-Out: Generation, transmission, and storage must be planned and financed as a single, integrated system to ensure economic viability and grid stability.

Through its strategic investment and technological leadership, China has proven that the four pillars of the Electricity Paradigm are achievable at scale, providing the blueprint for the global energy transition and setting the new standard for energy infrastructure for the 21st century.

.

Some Frictional Points Unveiled: Navigating Systemic Hurdles

Although the structural investment case for the Electricity Paradigm is exceptionally strong, institutional investors should anticipate a transition path that is nonlinear and shaped by meaningful systemic frictions. Geopolitical competition, regulatory fragmentation, supply-chain constraints, and the scaling curve of emerging technologies each have the potential to slow, reshape, or raise the cost of the transition. These dynamics introduce timing uncertainty and cost variability that must be reflected in underwriting assumptions. For private-market allocators including pensions, sovereign wealth funds, insurers, endowments; these hurdles are not deterrents but essential inputs to scenario design. Incorporating such risks enables more realistic, risk-adjusted deployment strategies and uncovers opportunities where complexity, delay, or misalignment create mispricing and scarcity value. Ultimately, disciplined modeling of these friction points positions long-horizon capital to capture the full breadth of opportunity across multiple electrification pathways, rather than relying on a single optimistic base case.

While the structural case for the Electricity Paradigm is powerful, its trajectory will be nonlinear.

The Implementation Hurdles in G10 & G20 States

For private-market institutional investors evaluating large-scale grid and transmission opportunities, it is tempting to view China’s rapid system build-out as a replicable benchmark. Yet the structural foundations that enable China’s “centralized blueprint” simply do not exist across G10 and G20 markets, making direct transplantation impossible.

- Regulatory Fragmentation and Permitting: In the United States, for example, building major transmission infrastructure requires approvals from a mosaic of federal, state, and local agencies, a process documented by the Congressional Research Service that can take significant efforts and time. For instance, SunZia Southwest Transmission Project took nearly 17 years from conception to the start of construction; illustrates the inherent procedural drag that investor must underwrite.

- Community & Local Resistance: Projects in U.S. (for example 2100MV SOO Green High Voltage Direct Current transmission line in the Midwestern) and in Europe have faced protracted legal and community challenges related to land use and visual impact, despite their clear role in regional decarbonization strategic vision, benefits and priorities.

- Divergent Investment Models: Finally, the capital-deployment models differ fundamentally. China’s state-directed system leverages policy banks and state-owned enterprises to mobilize financing at unprecedented speed and scale. Western markets, by contrast, rely on layered project-finance structures including private capital, public-private partnerships, regulatory risk-sharing; and while these frameworks enhance transparency and distribute risk, they inevitably lead to a more incremental and fragmented build-out. For investors, the implication is clear: the opportunity set in Western markets is compelling, but it is defined by structurally slower execution cycles, more complex stakeholder management, and a financing architecture that demands sophisticated risk allocation rather than centralized direction.

The New Industrial Geopolitics: Where Energy, Security, and Capital Converge

The global energy transition is reshaping the world’s balance of power but not in the way most assume. The narrative that mineral-rich nations will replace oil producers as the new energy superpowers misses the far more consequential shift already underway: strategic leverage has moved downstream, toward the nations that dominate the processing, refining, and industrial conversionof critical minerals. This creates a new geopolitical landscape defined by a tense struggle between the efficiency of established supply chains and the urgent pursuit of resilient, secure alternatives.

- The Processing Bottleneck: Mining concentration is well known; the Democratic Republic of Congo (DRC) produces more than 70% of global cobalt but the real vulnerability lies further along the chain. According to the International Energy Agency (IEA), China controls nearly 90% of rare-earth separation capacity and a dominant share of lithium and cobalt refining. This is not an accident. It is the outcome of decades of deliberate state-supported investment in heavy industrial infrastructure that Western economies consciously offshored.

- The Western Onshoring Dilemma: Now, the U.S., EU, Japan, and their partners are scrambling to unwind this dependency. Through sweeping industrial policies including the Inflation Reduction Act, the Critical Raw Materials Act, and a growing web of strategic trade alliances; Western governments are attempting to rebuild what was lost: domestic and “friend-shored” processing capability for the metals and materials at the heart of electrification. But reindustrialization comes with a price. Processing and refining are capital-intensive, environmentally contentious, and difficult to permit in high-cost jurisdictions. For the first time in nearly three decades, Western economies must internalize the industrial footprint they once exported in the name of efficiency.

- The Resilience-Cost Trade-off in Practice: This marks the beginning of a new global trade-off cost-efficiency versus resilience. The existing supply chain; centralized, optimized, and overwhelmingly China-centric; is cheaper. The emerging supply chain distributed, politically aligned, and domestically anchored; is more secure but inherently more expensive. For private-market institutional investors, this is the inflection point. What emerges from this geopolitical reset is not simply a supply chain shift, but a multi-decade industrial investment cycle: the rebuilding of refining capacity, midstream processing infrastructure, specialty materials manufacturing, and enabling clean-energy supply-chain assets across allied markets.

Security is being repriced. Industrial capacity is being rebuilt. And private capital will play the decisive role in financing the new architecture of the global energy economy.

The Scalability & Economic Hurdles of Storage

Long-duration storage (LDS) is the final unresolved pillar of a fully renewable electricity system and yet it remains the least investable today as its path to widespread, cost-effective deployment is fraught with challenges. While the global energy transition has driven extraordinary cost declines in solar, wind, and short-duration batteries, the absence of scalable, affordable LDS is a structural bottleneck for achieving a 24/7 decarbonized grid. No technology has yet emerged as a clear, economical, and scalable winner for the multi-day and seasonal storage required for a fully renewable grid. For institutional investors, this category represents immense long-term opportunity but few near-term avenues for deployment.

1. The Technology Mismatch

Lithium-ion dominates today’s short-duration storage market, performing efficiently for 4–8 hour applications. But when stretched to multi-day or seasonal use cases:

- Economics collapse due to high capex, cycle inefficiencies, and idle self-discharge.

- Supply chains are volatile, with lithium projected to tighten sharply before 2030 (IEA).

- Commercial maturity is insufficient for institutional-scale deployment.

In short, lithium-ion cannot deliver the trifecta investors demand: scalability, cost efficiency, and bankable reliability for long-duration applications.

2. Traditional Alternatives Are Constrained

Established technologies offer no immediate remedy:

- Pumped Hydro Storage (PHS): While PHS provides the vast majority of the world’s current grid storage capacity, its future scalability is severely limited. Most viable sites in developed nations are already utilized, and new projects face prohibitive costs, significant lead times, and environmental opposition. While retrofitting existing facilities offers incremental gains, we must consider other scalable solution for a rapid transition over the next decade.

- Thermal Storage (e.g., sand, molten salt): These systems are highly effective and low-cost for providing heat for district heating or industrial processes, displacing natural gas. However, reconversion to electricity is often inefficient (~30% – 50%), destroying their economic value for the grid. Their primary role is in decarbonizing heat, not in competing with batteries for electricity services.

- Compressed Air (CAES) & Green Hydrogen: CAES is geographically niche, requiring specific geological formations. Green hydrogen, while ideal for seasonal storage and hard-to-abate sectors, has a very low round-trip efficiency (~30-40%), making it an expensive electricity source. Its highest value is as a clean feedstock for industry and for decarbonizing sectors like shipping and aviation.

3. Emerging Chemistries: Potential vs. Deployability

Next-generation batteries including flow systems, metal-air, and other novel chemistries offer long-term upside but are trapped between pilot demonstrations and gigawatt-scale commercialization. Flow batteries offer longer duration than lithium-ion but at a higher upfront cost.

Newer chemistries are even further from proven manufacturing and levelized cost competitiveness. Widespread, economical deployment is a medium- to long-term prospect, not a near-term certainty.

- Technology readiness levels are too low for institutional underwriting.

- Scaling from pilot to gigawatt projects is capital-intensive and slow.

- Timelines for commercialization are measured in decades, not years.

The result is a market searching for its first truly bankable, utility-scale solution.

Conclusion

The transition to the Electricity Paradigm is the defining structural shift of the 21st century, but its path is neither linear nor certain. Its pace and the shape of the trajectory will be determined by the balance between accelerating innovation and these persistent, systemic frictions. Long-duration storage sits at the intersection of strategic necessity and commercial underdevelopment.

For institutional investors to capture outsized risk-adjusted returns solving the storage gap is imperative. The market is waiting for its breakout technology, and the next wave of decarbonization will be defined by those who anticipate it.

For stakeholders, this reality creates both risk and opportunity. This is also where Zinqular’s platform provides a decisive advantage: our capability to navigate, model, and price these multifaceted hurdles allows our partners to build more resilient and valuable strategies in an uncertain landscape.

.

Zinqular Investment Partners – Capitalizing on the Paradigm Shift

The global transition to the Electricity Paradigm represents a generational investment opportunity, characterized by long-term, defensive, and essential assets. Zinqular Investment Partners has positioned itself at the forefront of this capital deployment, recognizing that the infrastructure required for this new ecosystem is the “New Alpha” for institutional investors [17]. Zinqular’s strategy is to move beyond general infrastructure funds and provide specialized private funds dedicated to capturing the highest-value, alpha-sized exposure in this complex and rapidly evolving sector.

The Alpha Opportunity in Energy Infrastructure

Infrastructure as an asset class has long been valued for its stability, inflation protection, and predictable cash flows, often supported by regulatory frameworks or long-term contracts. However, the energy transition has introduced a new dimension: Alpha Generation.

Alpha in this context is not derived from market timing or speculative trading, but from:

- Deep Sector Specialization: Possessing the technical and regulatory expertise to identify, acquire, and manage complex, next-generation assets (e.g., UHVDC converter stations, long-duration storage facilities).

- Operational Excellence: Implementing proprietary technologies and management practices to optimize asset performance, reduce downtime, and increase efficiency beyond industry benchmarks.

- First-Mover Advantage: Targeting mid-market, complex projects in G10 and G20 nations that are beginning to adopt the Pioneer Nation’s blueprint, thereby securing assets before they become commoditized.

The global investment required for grid modernization is estimated to be in the trillions, but the capital is constrained by limited traditional funding and regulatory hurdles [18]. This creates a perfect environment for specialized private capital to step in and generate outsized returns.

Zinqular’s Specialized Private Funds Strategy

Zinqular Investment Partners offers a suite of specialized private funds, each designed to provide institutional investors with targeted exposure to the most critical and high-growth segments of the New Electricity Paradigm.

The Grid Modernization Fund (GMF)

- Focus: Targeting the 80% replacement opportunity in transmission and distribution infrastructure. This includes investments in HVDC/UHVDC converter stations, smart grid technology, advanced metering infrastructure (AMI), and specialized, low-loss cabling.

- Alpha Thesis: Returns are generated by acquiring and upgrading legacy assets, and by financing the construction of new, essential transmission corridors that are guaranteed long-term, regulated returns. The GMF provides a defensive, non-cyclical exposure to the core backbone of the new economy.

The Long-Duration Storage Fund (LDSF)

- Focus: Dedicated to the “Massive Storage” pillar, specifically non-Li-ion technologies required for seasonal and regional energy security. This includes thermal storage (sand/molten salt), compressed air energy storage (CAES), and green hydrogen production facilities linked to grid stabilization.

- Alpha Thesis: The LDSF targets the highest-value segment of the market—the decoupling factor. By financing and operating assets that solve the intermittency problem, Zinqular captures the premium associated with dispatchable, reliable power, analogous to the strategic value of crude oil reserves.

The Global Electrification Fund (GEF)

- Focus: Investing in the essential supply chain and end-use infrastructure that facilitates the final transition. This includes manufacturing facilities for specialized components (e.g., high-efficiency transformers, HVDC components), and the build-out of large-scale EV charging and industrial electrification networks.

- Alpha Thesis: The GEF captures returns from the massive volume growth driven by the electrification of transport and industry. It is a high-growth, cyclical exposure that benefits directly from the accelerating adoption curve of electric end-use technologies.

Institutional Investor Value Proposition

Zinqular’s funds are structured to meet the stringent requirements of institutional investors (pension funds, endowments, sovereign wealth funds):

- Risk-Adjusted Returns: Providing superior, risk-adjusted returns through a focus on essential, contracted infrastructure assets.

- GSR & ESG Alignment: Offering a clear, measurable contribution to global net-zero mandates, ensuring alignment with institutional Global Sustainability & Resilience (GSR) and Environmental, Social & Governance (ESG) criteria.

- Defensive Positioning: The demand for electricity is inelastic and growing, making these assets highly defensive against economic downturns and market volatility.

By focusing on the four pillars of the New Electricity Paradigm, Zinqular Investment Partners is not just investing in the future of energy; it is investing in the foundational infrastructure of the next global economic cycle, providing institutional clients with a unique path to alpha-sized exposure.

.

The Dawn of the Electrified Century

The Inevitability of the Transition

The transformation from the Crude Oil Paradigm to the Electricity Paradigm is no longer a matter of technological possibility or political will; it is an economic inevitability. The convergence of cheap renewable generation, scalable storage, and ultra-efficient transmission has created a system that is structurally superior to its predecessor in terms of cost, resilience, and environmental impact.

The historical dominance of crude oil was predicated on its four pillars. The fact that electricity has now achieved functional equivalence in all four: Cheap Power, Massive Storage, Efficient Transmission, and Universal Accessibility; signals the end of the oil-centric economic era and the dawn of the electrified century.

Social & Geopolitical Implications

The shift will have profound social and geopolitical consequences:

- Decentralization of Power: While the Pioneer Nation demonstrated the power of centralized planning for the backbone, the new grid is inherently more decentralized at the edges. This democratization of energy production can lead to greater energy independence for communities and nations.

- New Geopolitics: The strategic importance of oil-producing nations will wane, replaced by the strategic importance of nations that control the critical minerals for batteries and the manufacturing capacity for UHVDC components and solar/wind technology. The new geopolitical battleground will be the supply chain of the electrified world.

- Poverty Reduction: Cheap, reliable electricity is the most powerful tool for economic development. The new paradigm promises to deliver this essential input to the developing world at a cost and scale previously unimaginable, accelerating global poverty reduction and industrialization.

Final Call to Action

The $25 trillion infrastructure opportunity is a one-time chance to rebuild the foundation of the global economy. For policymakers, the call to action is to embrace the blueprint set by the Pioneer Nation, streamlining regulatory processes to enable the rapid deployment of UHVDC and long-duration storage. For institutional investors, the message is clear: the alpha is in the infrastructure. The time to commit capital to the specialized funds that are building the new global commodity network is now.

The next 100 years will be defined by the electron, just as the last 150 were defined by the barrel of oil. The New Electricity Paradigm is not just a cleaner alternative; it is the most powerful and efficient engine ever devised for human progress.

.

Appendix & References

Appendix A: Comparative Analysis of the Two Paradigms

| Pillar | Crude Oil Paradigm (1860-2025) | Electricity Paradigm (2025-2125) |

| 1. Cheap Production | Cheap Extraction: Low lifting cost from concentrated, easily accessible reserves (e.g., Middle East). | Cheap Power: Low Levelized Cost of Energy (LCOE) from hyper-efficient renewables (Solar/Wind) and stable hard sources (Nuclear/Hydro). |

| 2. Storage | Massive Storage: Physical storage in tanks, tankers, and Strategic Petroleum Reserves (SPR). Decouples production from consumption. | Massive Storage: Utility-scale batteries, Long-Duration Storage (LDS) like sand/molten salt, and Pumped Hydro. Decouples generation from consumption. |

| 3. Efficient Transport | Low-Loss Pipeline Network: Pipelines and supertankers move liquid fuel over vast distances with near-zero loss. | Ultra-Efficient Transmission: HVDC/UHVDC lines move electrons over vast distances with minimal loss (3% per 1,000 km). |

| 4. Accessibility | Universal Accessibility: Refinery network and ubiquitous retail distribution (gas stations). Standardized consumption (ICE). | Universal Accessibility: Smart Grids, Microgrids, and V2G. Standardized consumption (Electric Motors, AI Data Centers). |

Appendix B: Glossary of Technical Terms

| Term | Definition |

| HVDC | High-Voltage Direct Current. A system for transmitting electrical power that uses direct current (DC) instead of alternating current (AC). Highly efficient for long distances. |

| UHVDC | Ultra-High-Voltage Direct Current. An advanced form of HVDC, typically operating at ±800 kV or higher, capable of transmitting massive amounts of power (up to 12 GW) over thousands of kilometers with minimal loss. |

| LCOE | Levelized Cost of Energy. The net present value of the unit-cost of electricity over the lifetime of a generating asset. Used to compare the cost-effectiveness of different generation technologies. |

| LDS | Long-Duration Storage. Energy storage systems capable of discharging power for 10 hours or more, including thermal storage, compressed air, and certain battery chemistries. |

| V2G | Vehicle-to-Grid. A system in which plug-in electric vehicles (EVs) communicate with the power grid to sell demand response services or feed power back to the grid. |

| SPR | Strategic Petroleum Reserve. Government-owned stockpiles of crude oil intended for use in an energy crisis. The analogue for the Electricity Paradigm is LDS. |

References

[1] Yergin, D. (1991). The Prize: The Epic Quest for Oil, Money, and Power. Simon & Schuster.

[2] Hamilton, J. D. (2011). Oil Prices, Exhaustible Resources, and Economic Growth. Handbook of the Economics of Climate Change.

[3] Al-Qaddafi, M. (1970s). Re-negotiation of terms of business in Libya. (Cited in historical accounts of the oil crisis).

[4] Investopedia. (2025). Oil Extraction Economics: Costs, Profits, and Global Impact.

[5] CME Group. (2025). Understanding Commodity Storage.

[6] API. (2025). Oil Supply Chain.

[7] Dallas Fed. (2014).150 Years of Boom and Bust: What Drives Mineral Commodity Prices? [8] U.S. Department of Energy. (2024). New Report Showcases How Innovation Can Fast Track Affordable Energy Storage.

[9] Lazard. (2025). Levelized Cost of Energy+ Report.

[10] Polar Night Energy. (2025).World’s first large-scale ‘sand battery’ goes online in Finland.

[11] National Grid. (2025). High Voltage Direct Current Electricity – technical information.

[12] Hitachi Energy. (2025). High-Voltage Direct Current (HVDC).

[13] Deloitte Insights. (2024). Grid expansion and modernization. (Estimates global US$25 trillion investment by 2050).

[14] BBC Future. (2024).’A bullet train for power’: China’s ultra-high-voltage grid.

[15] Pictet Asset Management. (2025). China adopts UHVDC to make electricity transmission ultra-efficient.

[16] Ember. (2025). China Energy Transition Review 2025.

[17] Mirova/Natixis IM. (2025). Energy transition infrastructure: generating alpha through sector specialisation.

[18] Infrastructure Investor. (2025). Which infra managers are generating pure alpha?

[19] World Energy Outlook (2025). International Energy Agency