Authors: Barry Simon Graham (Co-CIO) and Michael Yaw Appiah (Co-CIO)

[wpfd_single_file id=”1979″ catid=”327″ name=”Download Print Friendly PDF Version”]

We believe 2022 will mark a monumental change on the path to new social, financial, and economic era. Several concurrent changes will propel the switch from the “current” to “new era”; that has begun within geopolitics, economic and social spheres. This will have massive implications for investors.

The evolving uncertainty connected to pandemic led to launch of ultra-easy fiscal and monetary policies for prolonged period relative to history. The unusual mix of the pandemic; economic downturn; enormous stimulus; ultra-low interest rates; excess savings; and supply & demand pressures unleashed a situation where for two years in a row global equity market returned positive and bonds returned negative yields. Amazingly, this has not occurred in over 50 years.

The economy has rebounded in ways that are considerably different than contemporary economic recoveries. Our foundational view is that after almost forty years, most governments introduced fiscal or monetary policies designed to expand output, stimulate spending, and curb the effects of deflation after the economic uncertainty due to COVID-19 pandemic (i.e., reflation has displaced disinflation). Therefore, to be successful “beyond the new era” will require realignment of strategies and priorities, plans and playbook.

In general, we at Zinqular think that the current environment remains positive for risk assets. Foundation to our understanding is that the overall ‘stock’ of global monetary support, including the over $12.96 trillion of increased central bank liquidity injected from the G4 economies since the beginning of the pandemic, will overrun the global interest rate tightening regime that has begun. Moreover, real rates, except in China, are still extremely low, which elevates the value of the illiquidity premium.

In this discussion, we will share our thoughts on the road ahead, albeit a rough one, especially as the ‘flow’ of liquidity into the economy slows. We share potential occasional market dislocations and robust opportunities that may present itself. In addition, – more than ever –this era will favor thematic investors who are thoughtful in their approach both of their strategies and agile plans.

And so, what is the situation now and what might the situation be in the next few cycles? Given the huge size of liquidity that is in the economy, our core research, quantitative models and our proprietary data help us to forecast that economic growth will continue at a good pace on a nominal basis for the next couple of years and/or cycles. In other words, the current period ‘mirrored’ to a past, could be the 2001-07 economic recovery. In those years, China’s fixed investment build-out led to inflationary pressures and a strong capex cycle; this time, by comparison, it is both record levels of stimulus and the global energy transition that are catalysts for upward pressure on input costs.

Key Messages: Setting the Scene

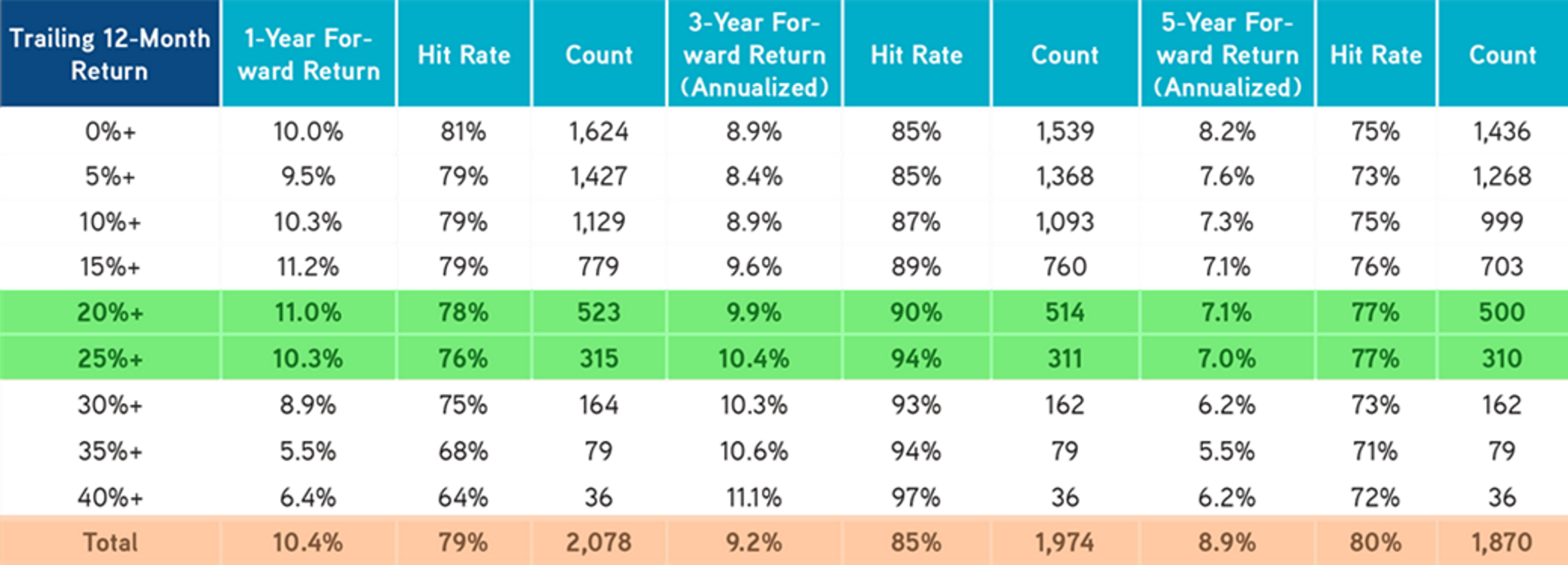

Essentially in reference to Exhibit 1, our research suggests that, despite several macroeconomic headwinds, now is not the time to hit the FUD (i.e. fear, doubt, uncertainty) button. In reality, grounded on 2021’s strong returns, the probability of positive forward returns over the next 12 months is approximately 72% or greater. On a 3-year basis, it is actually 88% plus.

Here are some key messages and/or summary from the “excelling beyond the new era” thesis.

- Inflation path: Several economic and market events will determine the path of inflation. Their combined effects are changing the dominant inflation narrative from low and temporary, to higher for longer. Inflation will not likely return to precrisis levels, as supply chain bottlenecks, surging energy prices, the rebalancing towards higher wages and rising tax rates will push it higher compared to the past decade. What initially has been a US story is spreading globally through rising food and energy prices, with the notable exception of China, where consumer prices (CPI) are under control but producer prices (PPI) are being squeezed, putting pressure on corporate margins.

Inflationary pressures, labor and housing in particular, will remain key areas of focus. All told, 24 of 26 headline CPI inputs are now above the Fed’s two percent long-run inflation goal. We boost our CPI forecast in the U.S. to 4.8% in 2022, compared to a consensus of 3.6%. We remain positive on pricing power stories and collateral-based cash flows across Private Equity and Real Assets.

In this transition from old (fighting inflation) to new (supporting a more equal and sustainable growth path) mandates, Central Banks will face the dilemma of when and how fast to switch on/off the accommodation button in a world of higher/permanent inflation and slower growth (a stagflationary path). The narrative of a trade-off between growth and inflation (on top of the stagflationary one) will drive Central Banks’ actions. - The Emerging Market (EM) Split: We think the EM concept as a group seems to be over. The great split will be spread across three worlds:

(a) countries with inflation and Central Banks introducing policies to control it;

(b) countries with Central Banks remaining inactive (in other cases out of control); and

(c) China.

Our view is that thematic Investors should favor (a) and (c), where currencies should also appreciate versus the US dollar, bearing the burden of hyper-Keynesian concept.

The China growth narrative will be critical; it will slow down, but not be derailed in our view. Chinese policy makers will have to manage China’s transition towards a more balanced and equal society, avert a hard landing and curb investors’ moral hazard in over indebted areas such as the real estate market. While such deleveraging goes ahead, fiscal and monetary policy should become moderately supportive.

The impact of a Chinese slowdown should remain contained overall, although spill overs on select metal/commodity exporters and trade partners may occur. Discrimination regarding emerging markets (EM) will be key. - The asset class of preference is equities. general purpose technologies, innovation and multiplicity assets should work well this cycle. We continue to be overweight on Global Equities again in 2022. We projected path has the S&P 500 ending 2022 at about 4950 with 16% EPS growth.

- There will be tightening measures in 2022 that we think real rates outside of China will lag this cycle. We forecast real rates of -0.14% in Europe and -0.53% in the U.S. respectively, in 2022. Housing will be a major beneficiary.

We are in a global tightening cycle, but the enormous liquidity stock will keep financial situations from getting too tight. Unlike the onset of the taper tantrum in 2013 (when the short-end of the curve was mispriced), we would now hedge the long-end of the interest rate curve. - We still see both strong demand and uneven supply, albeit better than in 2021, for commodities again in 2022. We still favor select commodities linked to the global energy transition. We still like longer-dated Oil.

Exhibit 1:

2022 Could Be Good Year Due To Excellent Gains In 2021

This based on S&P 500 price return since 1981. Data as at November 24, 2021. Source: Bloomberg.

Both structural and cyclical risks are increasing: for instance, on the structural issue, we think that the risk of ‘irrelevance’ from disintermediation is mounting. General purpose technologies and innovation is ubiquitous across multiple industries, and it is leading to disruptors displacing incumbents. Remember the average company in the S&P 500, one of the most blue chip of equity indexes, now lasts just 12 years as an index member; as compared to an average of 61 years in 1958. This thematic work at Zinqular suggests that the pace of innovation will continue to speed up. Central to this increase, is the proliferation of global data that can be shared, analyzed, and interpreted (including providing insights). Notwithstanding, global data is likely to almost triple (3x) every two years.

Exhibit 2:

We Positioned Certain Portfolio More to Real Assets; Quantitative Easing (QE) & Increased General-Purpose Technologies & Innovation Led to Surge in Financial Assets.

This comprises of assets of Households, Nonprofits, and Non-Financial Corporations. Data as at July, 2021. Source: Federal Reserve, Bureau of Economic Analysis, Haver Analytics.

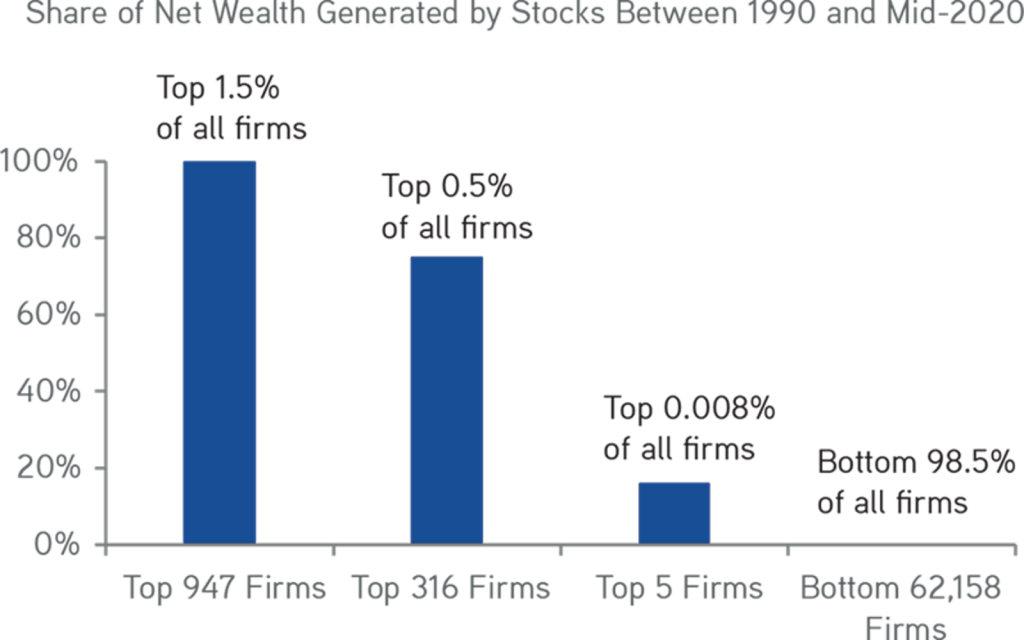

Exhibit 3:

Since 1990, A Tiny 1.5% Of All Stocks Generated Huge Net Wealth In The Global Equity Markets. We Continue To Be Bullish On Innovation & General-Purpose Technologies Equities & Assets.

Note: Net wealth accounts for wealth generated above the performance from one-month Treasury bill. Data as at July, 2020. Source: H Bessembinder, Arizona State University 2020.

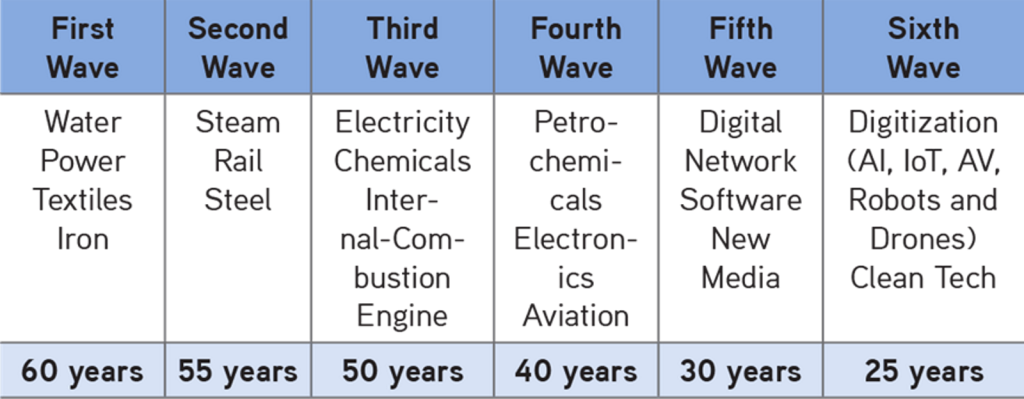

Exhibit 4:

We Are In The Sixth Wave Of Creative Destruction (/Incl. Innovation & General-Purpose Technologies)

Data as at 2021. Source: Edelsen Institute, Detlef Reis.

Therefore, we view emerging industries such as AI, renewables, 5G/6G+, life sciences and digitalization including technologies connected to more sustainable logistics & supply chains, financial services, bionic humans, and blockchain are all chipping away at incumbent processes and/or offerings. The industry change is happening faster than many think. Past experience, though, suggests few incumbent CEOs will take up the creative destruction required to maintain their firms’ leadership positions in their industries. Amazingly, this is occurring with government intervention that has driven down the cost of capital for new entrants/disruptors to record low levels. Therefore, it is business as usual for long-term and thematic investors.

Exhibit 5:

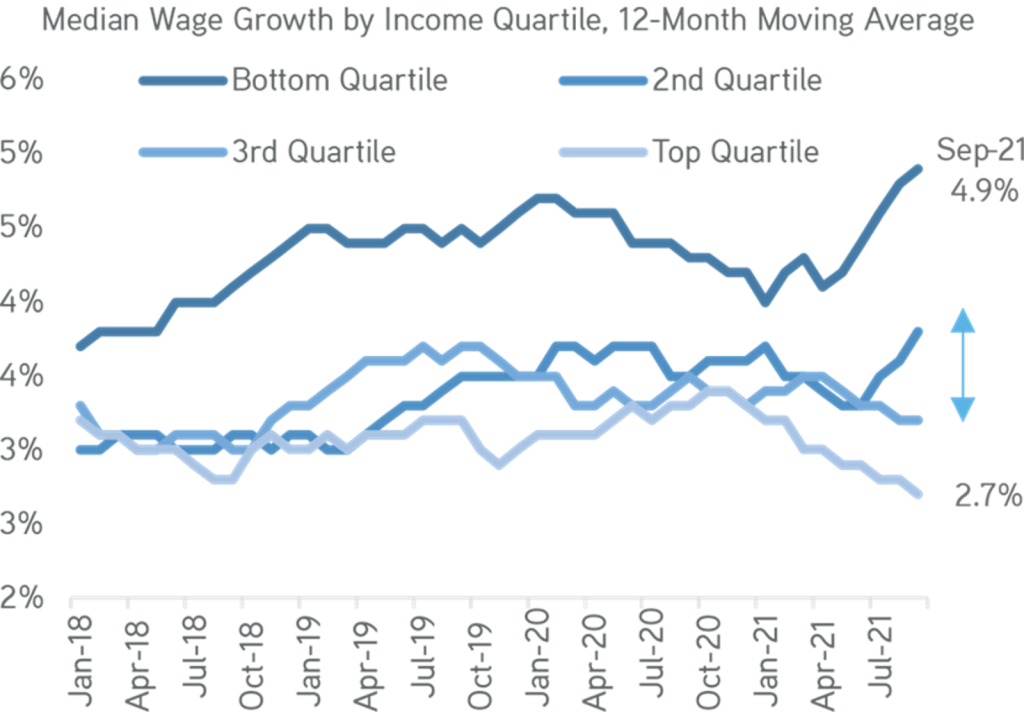

Wage Pressures Are Noticeable At The Lower Segment Of The Income Scale

Data as at November, 2021. Source: Atlanta Fed, Haver Analytics, Zinqular Insights & Research Hub analysis.

Exhibit 6:

Across Major Developed Markets Are Labor Scarcity Issues

Data as at November 12, 2021. Source: Indeed Hiring Lab, Haver Analytics.

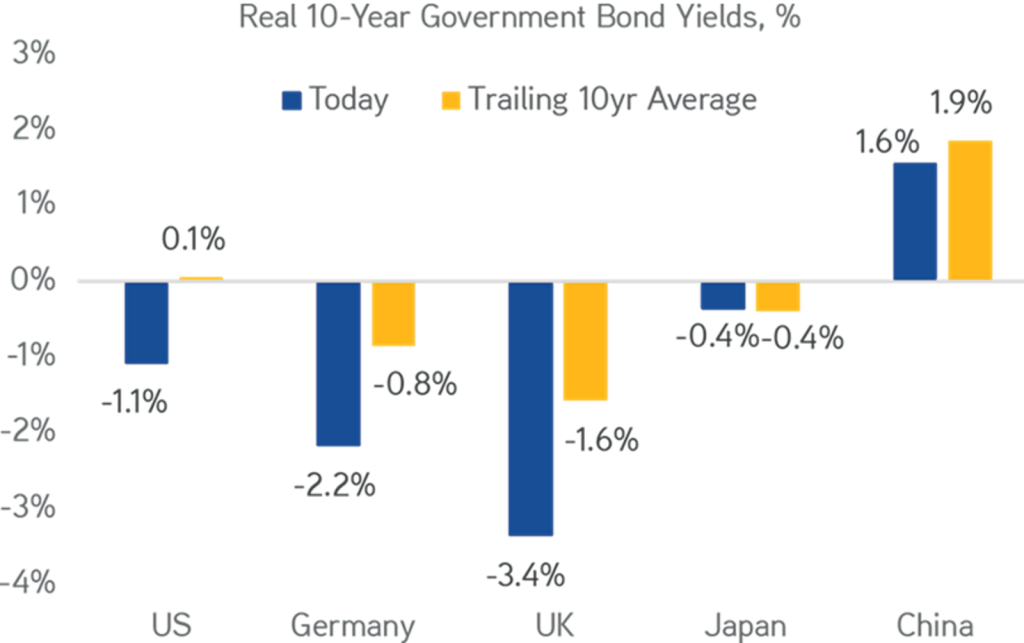

There are certainly inflationary pressures to consider on the cyclical side of the risk ledger. We are using a 5.5 percent inflation rate for the U.S. in 2022, and on a global basis, we are generally above consensus. Our thinking is that governments and other agencies will come around to our view that many aspects of the current inflationary situation will not be transitory, particularly as it relates to labor costs (Exhibits 5 and 6). In other words, inflation is going to land at a higher rate than it did in the past decades. Despite our view that global monetary policy accommodation will begin to shift in 2022, we also think that real rates will drag this cycle in the developed markets (Exhibit 7).

Exhibit 7:

Real Yields Remains Much Lower this Cycle Outside of China

Data as at December, 2021. Source: Bloomberg.

Exhibit 8:

Across Industries U.S. Inflation Is Wide-Ranging

Data as at November 15, 2021. Source: Zillow, Manheim, Bureau of Labor Statistics, Haver, Bloomberg, Zinqular Insights & Research Hub analysis.

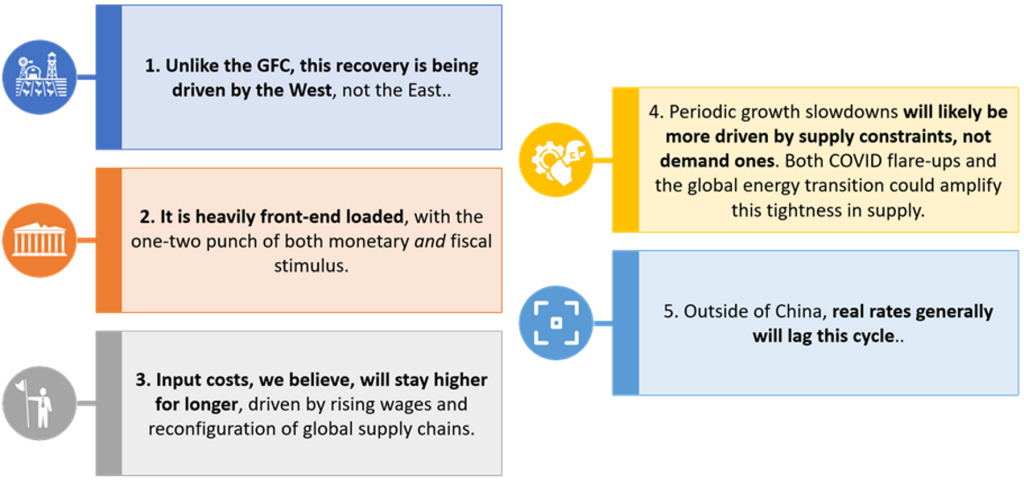

At this stage, we believe that the current restart will be best remembered for its reflationary nature. In our view, there is excessive money in the economy for the current growth trajectory we are forecasting. In addition, there are too few people available to work for key industries in developed markets like the United States. Lately, the recovery has been V-shaped, while monetary policy – until recently – has been L-shaped. So, we search for an economic backdrop that is wildly different than what unfolded after the 2008 downturn. Underlining our convictions are the following five points:

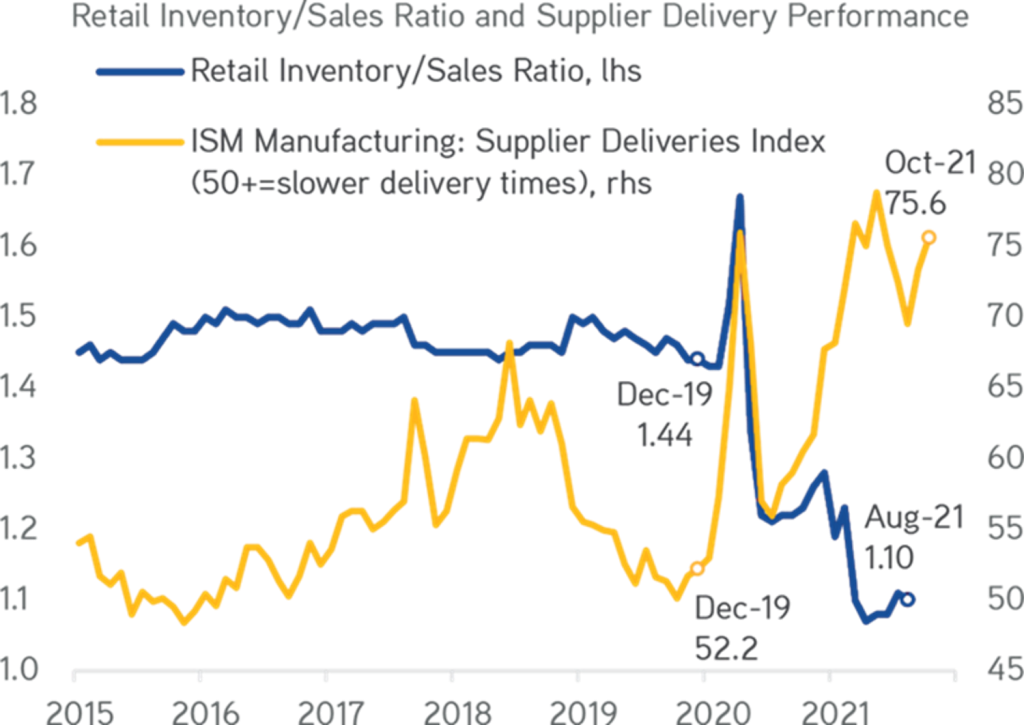

Exhibit 9:

Low U.S. Inventories Augurs Well For Growth & Pricing

Data as at November, 2021. Source: Census Bureau, Institute for Supply Management, Haver Analytics.

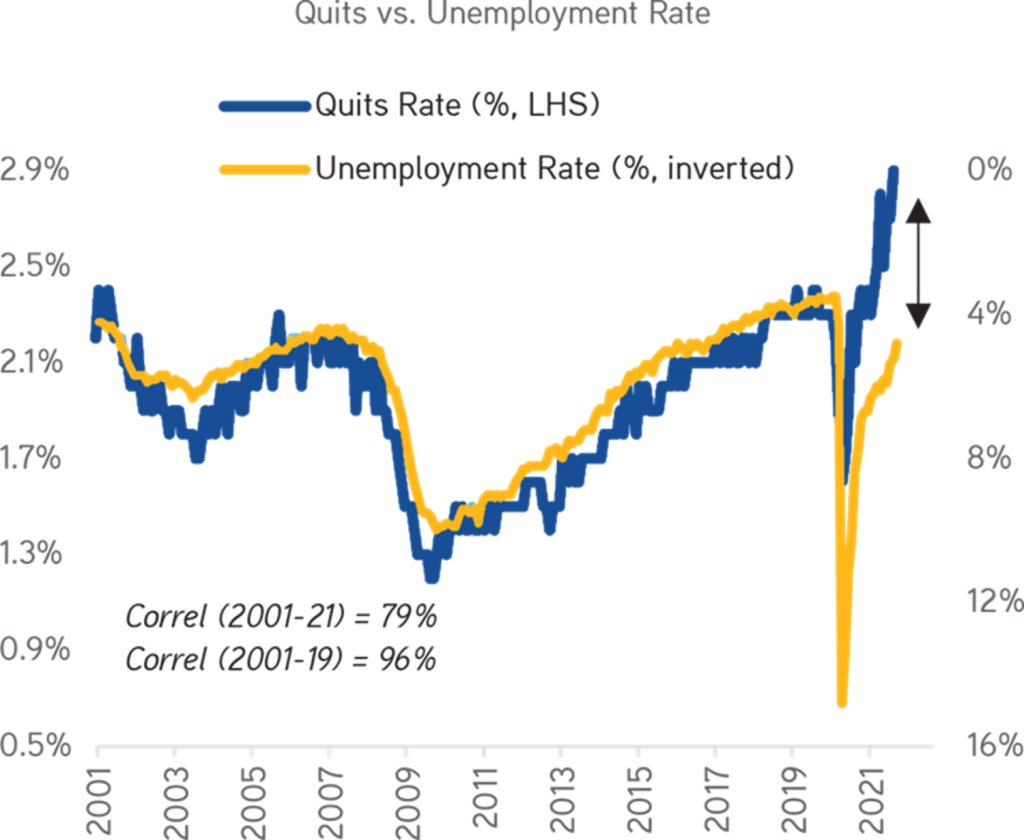

Exhibit 10:

The Great Resignation Of Workers Would Lead To 1% Unemployment

Data as at November 2021. Source: BLS JOLTS Survey, Haver Analytics, Zinqular Insights & Research Hub analysis.

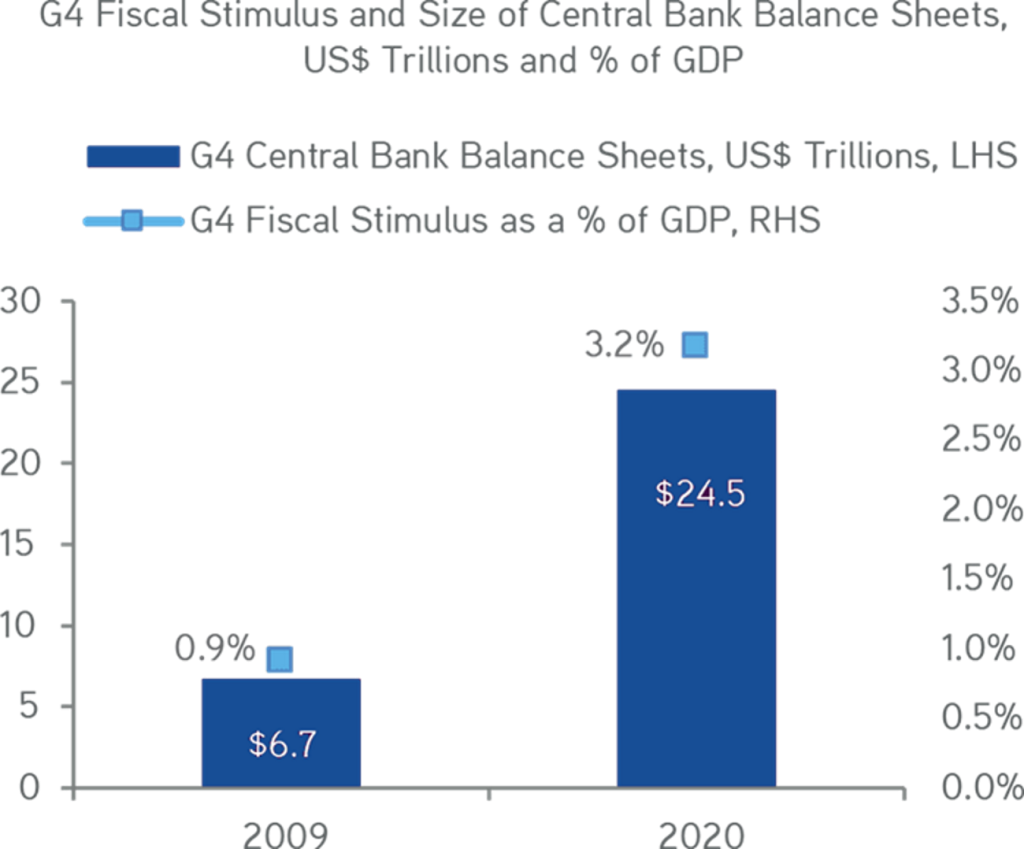

Exhibit 11:

Compared To History, There Is Huge Upfront Stimulus Spend By Gov’t & Central Banks This Cycle Due COVID-19

Data as at November, 2021. Source: Bloomberg, Morgan Stanley.

Key Investment Convictions for 2022

In our “excelling beyond the new era” thesis, we suggest six macro forecasts worthy of investor focus in 2022. These themes are based Zinqular internal data that gives the better visibility on the outlook in the next cycles.

Regardless of which viewpoint you embrace, there is no doubt that we are living in times that require both a sound understanding of the past and a heightened conviction about where we are headed in the future. The good news for Zinqular and its partners is that we are building a demonstratable narrative that “beat others at their game.”

1 We Are Bullish on ESG Themes: Climate change and the transition to cleaner energy, which based on our data could be a four trillion dollars per year global investment opportunity, are clear areas of focus for many thematic investors. This transition will compromise multiple industries as companies and consumers embrace more sustainable products, more energy efficient real estate, and more innovative transportation. We also continue to prioritize opportunities that benefit from pandemic-related structural tailwinds across areas like education/work-force development, waste management, public and private health, and industrial technology.

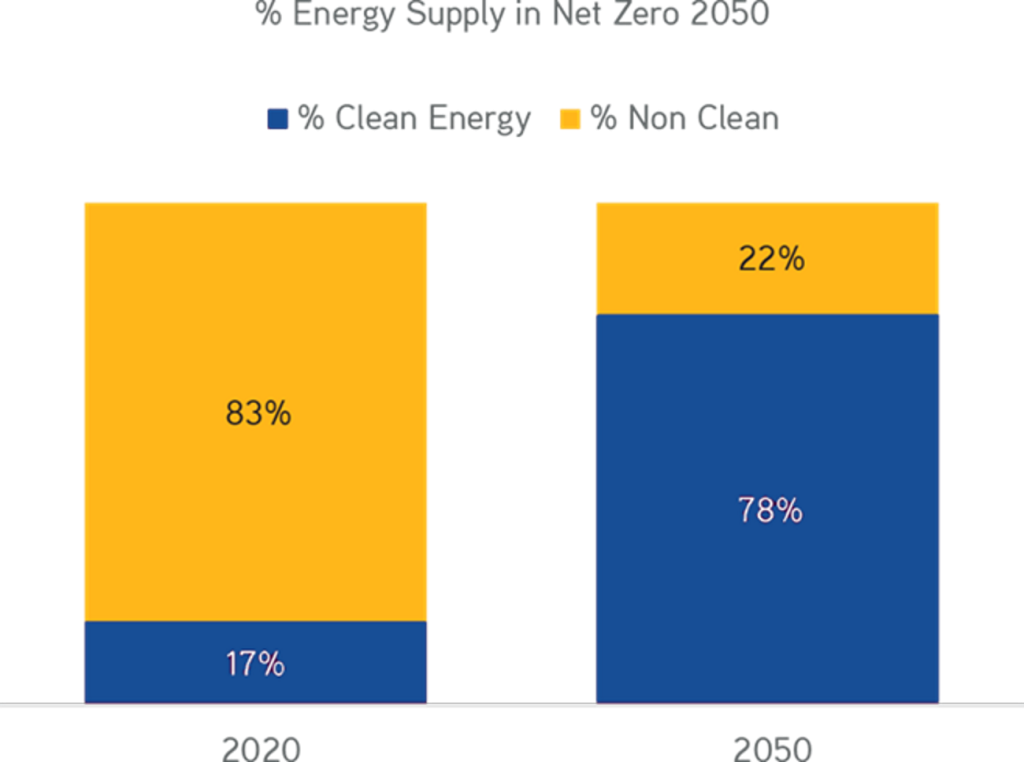

Energy transition is certainly a “Colossal Theme” and part of Zinqular investment strategy.Environmental considerations represent a major investment opportunity, specifically amidst growing concerns about supply chain resiliency. This colossal theme is broad-based, in a way that we think that almost all aspects of ESG are worth considering, including climate action (e.g., energy transition including solar, wind, batteries and storage [metals for batteries e.g., Cobalt, lithium, Copper, etc.], EV, distributed generation, energy efficiency, etc.). We also think that ensuring resiliency and sustainability of supply chains (e.g., power transmission, distribution, charging stations, etc.) could fuel a capex super‐cycle. Notwithstanding, we believe that there is an opportunity to help reduce carbon footprints of many old economy sectors as well, including traditional commodity producers and manufacturers, many of which are currently being starved of capital, despite the stark reality that they still play critical roles in the greening of the global economy. Remember that today, less than 20% of the total global energy supply is linked to clean energy sources (Exhibit 13). As part of the energy transition, we are also seeing a growing number of global businesses shedding complex portions of their overall corporate footprints to reduce sustainability challenges and/or conflicts. As part of this transition, we also expect to see consumer patterns change, including championing products that are more environmentally friendly. The capital markets too will play a role, as companies with cleaner carbon footprints may be able to finance themselves more cheaply on a relative basis.

Exhibit 12:

Huge Efforts From Stakeholders To Focus On ESG

Data as at December, 2020. Source: BP Statistical Energy Review 2020 and 2015, BLS, World Energy Consumption database 1820-2018 (2020 revision) Paolo Malanima.

Exhibit 13:

Yet Net Zero Is Difficult To Achieve (While Net Negative Is Impossible…)

Data as at August 2021. Source: International Energy Agency (2021), Net Zero by 2050, IEA, Paris: Net Zero by 2050 Scenario – Data product – IEA. License: Creative Commons Attribution CC BY-NC-SA 3.0 IGO.

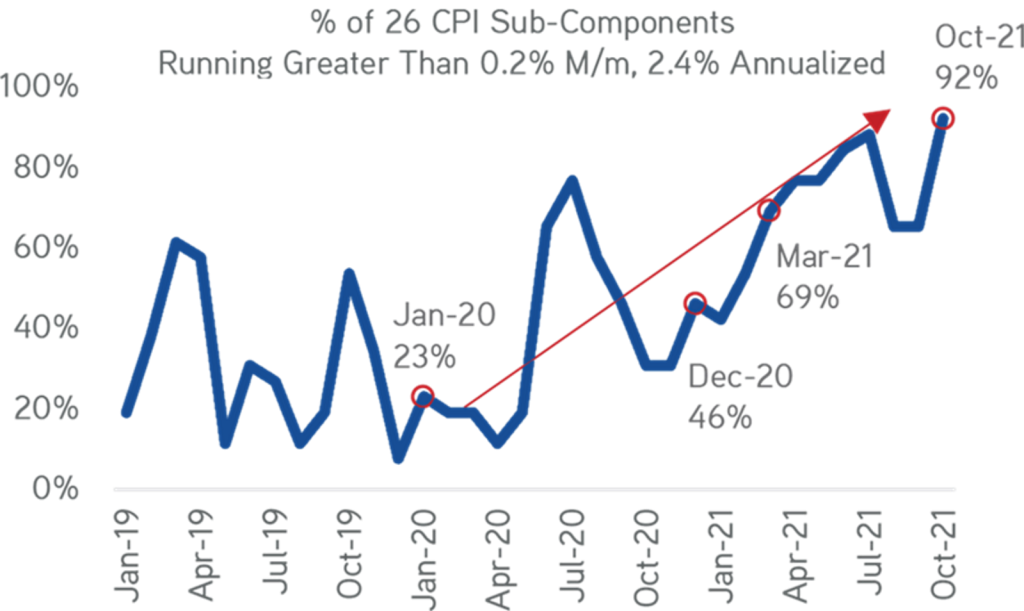

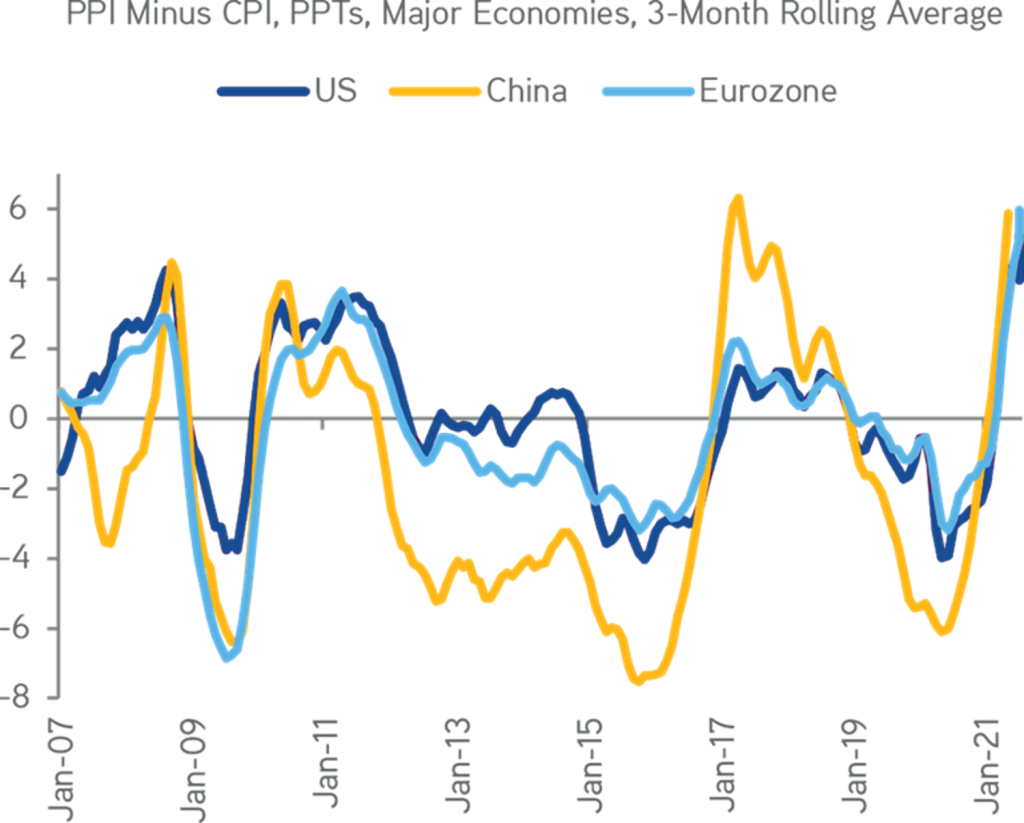

2 Keep Buying Companies with Pricing Power (Price Makers) & Ignore Price Takers. This is a mega theme for this cycle, as we believe that we have now entered a world where input costs, including wages and select commodity prices, are increasing at a faster pace than consumer prices. The macroeconomic inflation landscape we envision is not ‘transitory’.

All told, 24 of the 26 inputs in the October CPI were running above the Fed’s long-term target for inflation (Exhibit 8). We do see supply chain pressures easing, but not to the degree or at the speed that some optimistic investors now anticipate. Maybe more importantly, though, is that the shortage of skilled labor has emerged as a structural headwind in many parts of the world, the U.S. in particular. Consistent with this backdrop, input costs, as measured by the PPI, are rising faster than output costs, as measured by the CPI (Exhibit 14a).

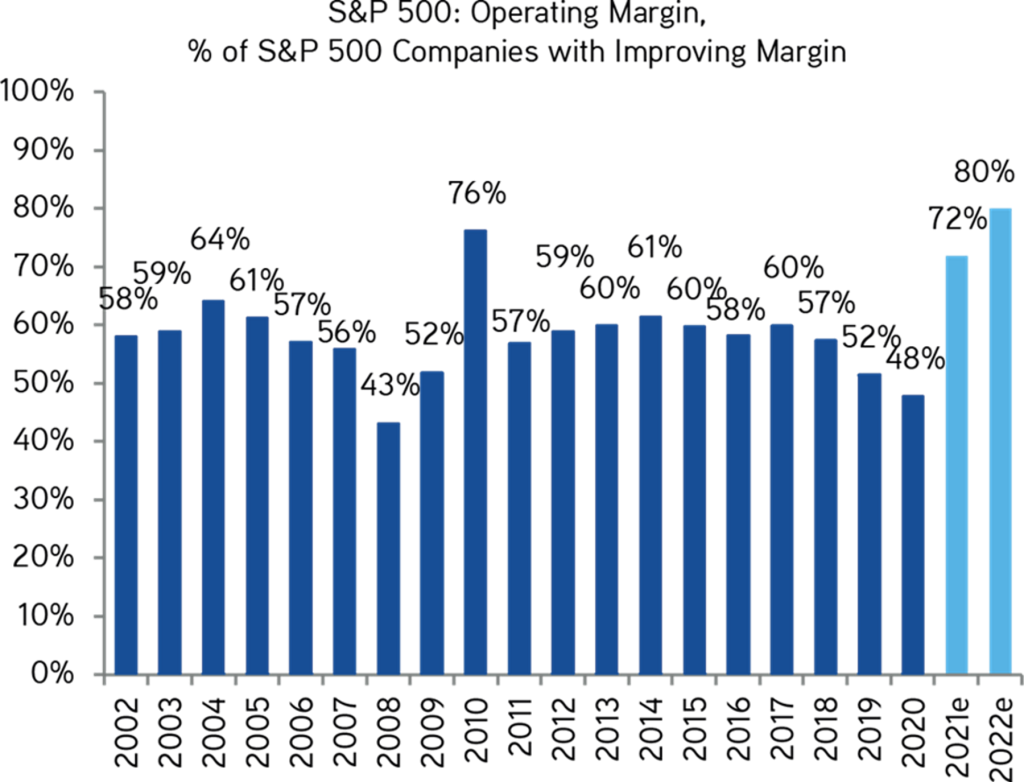

This type of environment heavily favors companies with pricing power. Therefore, we think that companies with pricing power, or what we call price makers, will be re-rated upward at the same time that price takers will be de-rated. Not surprisingly, this macro backdrop will create more volatility, as margin estimates are too optimistic and rate of change on economic growth slows. Just keep in mind that the consensus now suggests that fully 80% of the companies in the S&P 500 will deliver improving margins (Exhibit 14b).

Exhibit 14a:

We Suggest Owning Pricing Power Narratives Due To Surging Input Costs

Data as at October, 2021. Source: Bloomberg.

Exhibit 14b:

Consensus Margin Expectations Appear At Extremes, Particularly Relative To History

Data as at October 28, 2021. Source: Factset.

3 We are Bullish on Collateral-Based Cash Flows. Asset-Based Finance, Infrastructure, and many parts of Real Estate should perform well in the faster nominal GDP environment we are envisioning. The value of the sound collateral that backs the cash flows can further enhance performance, particularly if investments have strong pricing power characteristics and are linked to some of our key themes (e.g., nesting, growth in data, resiliency). This remains a table pounder for us, especially given the unusual backdrop of rising cyclical inflation, more stimulus, and higher commodity prices.

Given the unusual backdrop of rising cyclical inflation, more stimulus, and higher commodity prices, we believe that demand for collateral-based cash flows is poised to speed more than many investors now think. Not surprisingly, the sharp drop in rates following the onset of the pandemic has only accelerated this phenomenon.

Exhibit 15:

Returns Surge On Apartment Real Estate, Reflects Outsized Rent Growth; 2021 Rent Growth Is Almost A Third Of CPI

Data as at November, 2021. Source: National Council of Real Estate Investment Fiduciaries.

4. Innovation/Digitalization/General-Purpose Technologies: In accordance with our view that we are in the next innovation and general-purpose technologies boom, we think that the pace of disruption accelerates, particularly as it relates to technological change across multiple industries. At the same time, though, the competitive landscape is changing rapidly, and as we indicated earlier, traditional incumbents, especially in financial services, will be challenged.

Over short few cycles, the investment into blockchain themes have jumped six times to $21 billion (according Crunchbase). Blockchain will mature within “this new era” and will power services beyond the “normal”. For instance, financial services beyond the normal will include in the area of infrastructure, compliance and analytics.

Specifically, we think that blockchain technologies could lead to a shift from centralization to decentralization across many established sectors, including creative arts, music and healthcare royalties as well as loans, custody, and insurance. This shift is a big deal, and we think it warrants investors’ focus (refer to Exhibit 18a, 18b).

Exhibit 16:

Massive Rollup Of Datacenter; AI, Data & Insights; Cloud Native IT & Networks; And Beyond Connectivity Themes Makes Us Bullish On Communications Infrastructure, Particularly Last Mile Financings & Investments

Data as at December, 2020. Source: Company reports, Mappiah Consulting, Deutsche Bank Communications Infrastructure.

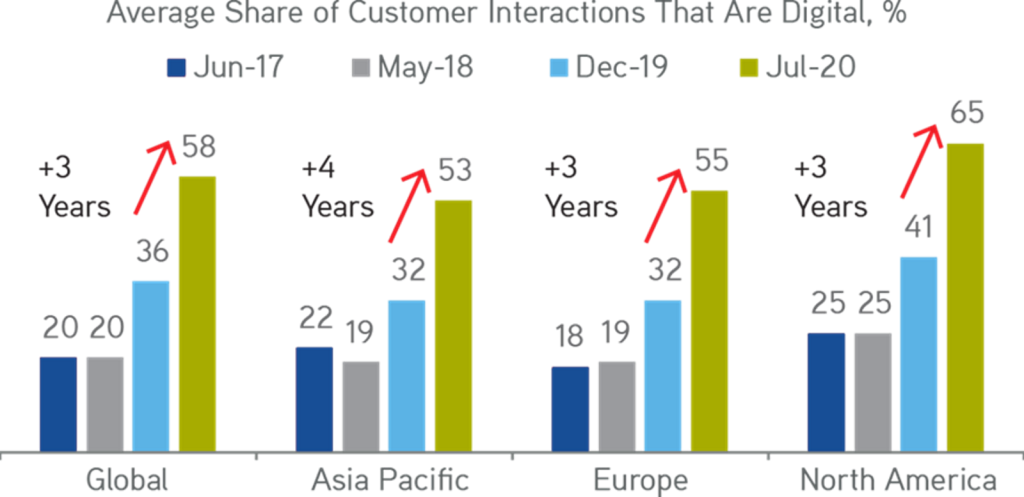

Exhibit 17:

COVID-19 Has Fast-Tracked Digitalization Themes; Now A Key Future Business Priorities

Note: McKinsey survey of 899 C-level execs and senior managers across all industries. Data as at September 2020. Source: McKinsey.

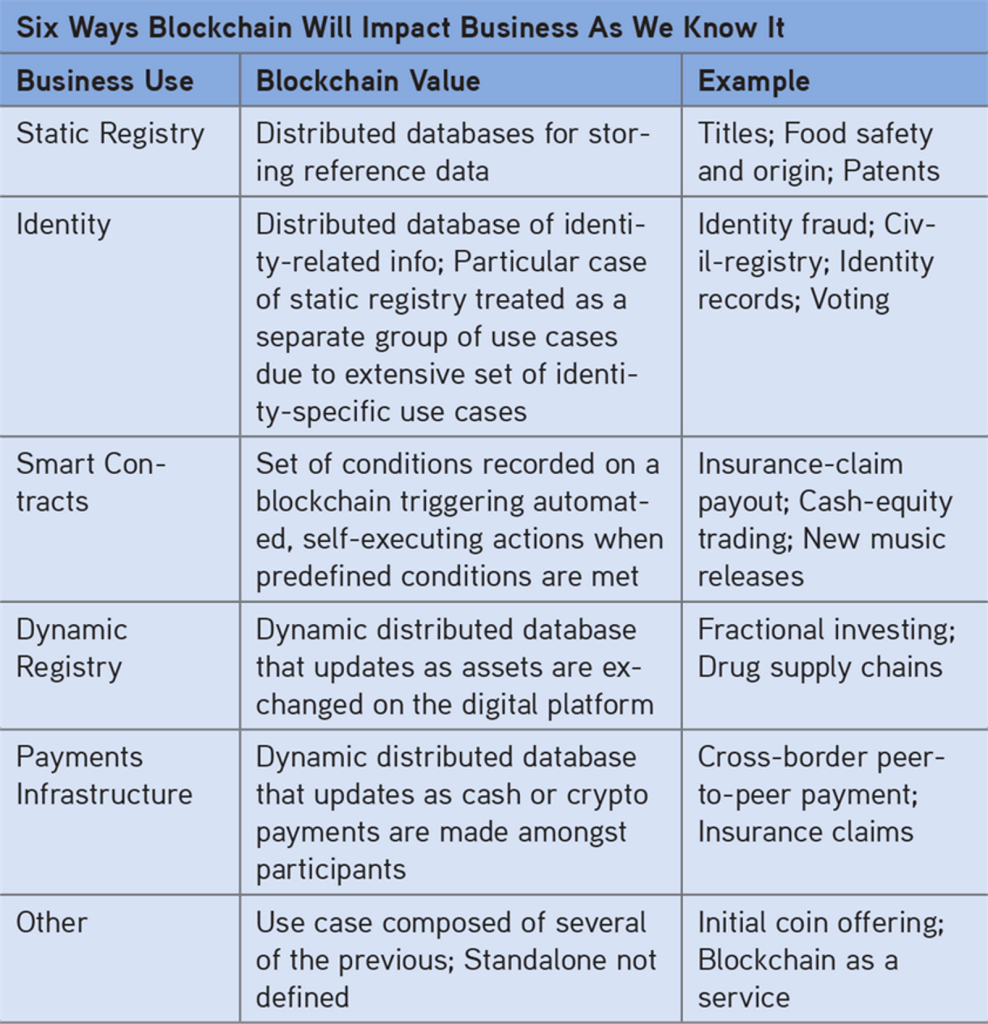

Exhibit 18a:

Blockchain Will Have High Impact On Financial Services And Beyond

Data as at June 19, 2018. Source: McKinsey.

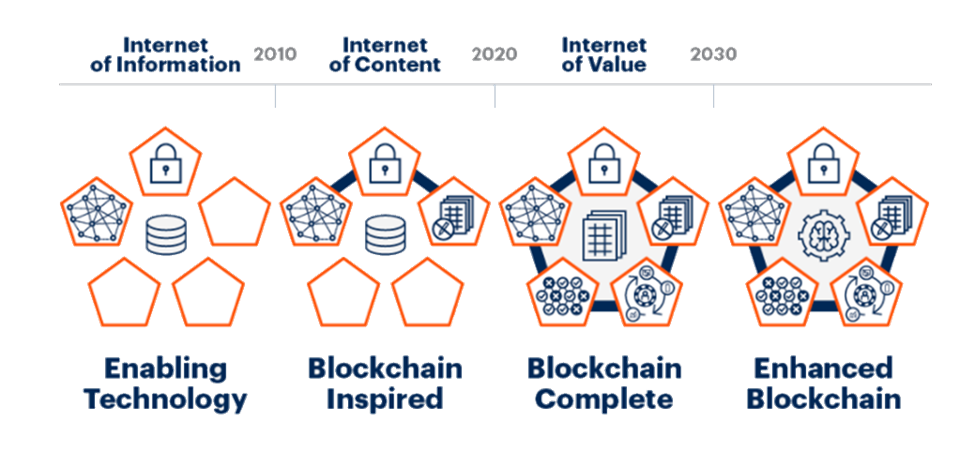

Exhibit 18b:

Blockchain Maturity Within This “New Era”

Data as December 2021, Source: Gartner

5. Global Rise of Millennials & Savings Bull Market: Our data shows that in the United States, there are at least 72 million millennials that are now at an age where they are buying houses, spending on their families, and shifting their consumer preferences. Moreover, in Asia there are now over 830 million millennials; their changing behavior at a time of huge technological transformation will have significant implications for all aspects of the global economy. If we are right (which we believe we are), then our nesting theme has more room to run. The millennial consumer also reinforces the ESG and sustainability trends mentioned earlier.

In Asia, for instance, 830+ million millennials intend to build a safety net via increased savings for their families. Nesting, retirement products, and financial planning should all benefit. Meanwhile, in the developed markets, quantitative easing has ‘stolen’ from older savers, who now are being forced to run with higher savings rates. QE has also lowered the real return on all investments, which means more must be tucked away to protect purchasing power. It also means the value of the illiquidity premium has increased. As we detail below, low rates are likely to persist for some time, which means, for instance, that more large blocks of life insurance books will be brought to market for sale. This backdrop favors scale players that can leverage technology, sourcing, and portfolio construction to deliver better investment management results.

Finally, we are on the cusp of a major intergenerational wealth transfer, one that could dwarf what the financial planning community has enjoyed so far.

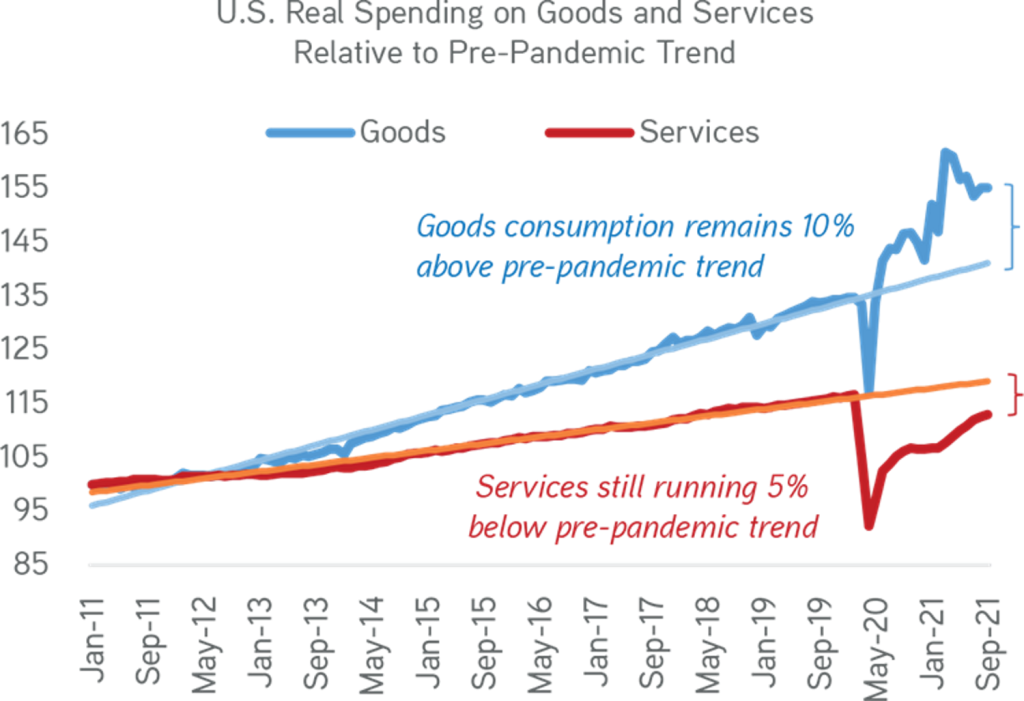

Exhibit 19:

About 70% Of Total Consumer Spending Are Recovering

Data as at November 30, 2021. Source: Bureau of Economic Analysis, Census Bureau, Zinqular Insights & Research Hub analysis.

Exhibit 20:

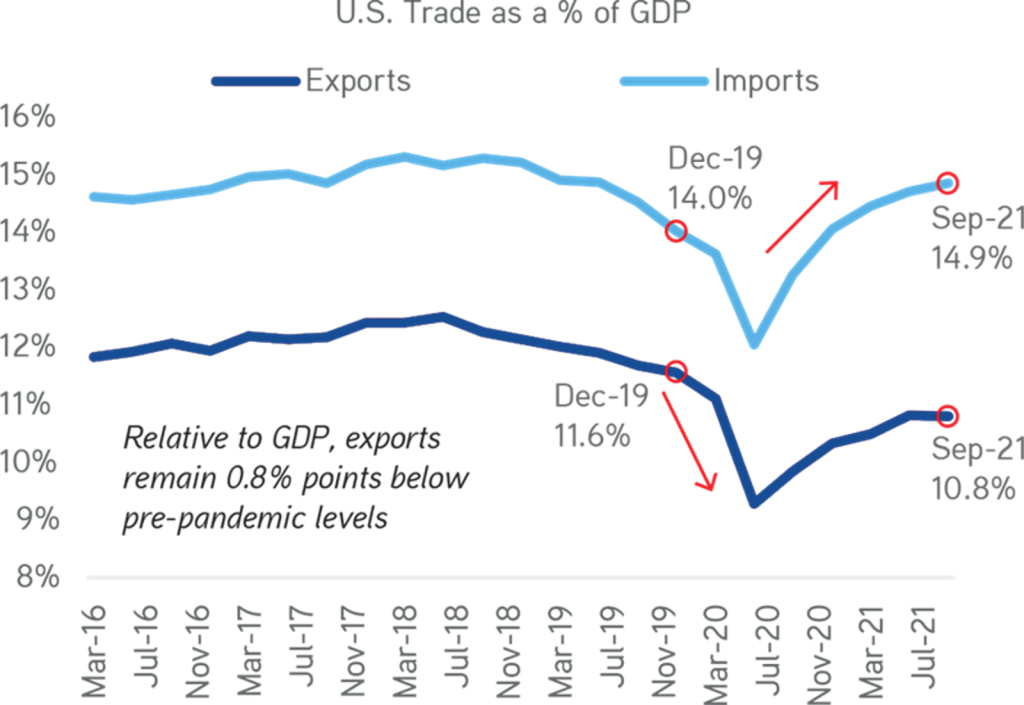

Foreign Tourism Will Be An Important Driver On The Services Side. U.S. Exports Are Still In Early-Stage Recovery.

Data as at December, 2021. Source: Bureau of Economic Analysis, Census Bureau, Zinqular Insights & Research Hub analysis.

Exhibit 21:

Excess Household Savings Approx. 18% Of Annual Retail Sales In China

Data as at December, 2021. Source: Wind, Zinqular Insights & Research Hub analysis.

Exhibit 22:

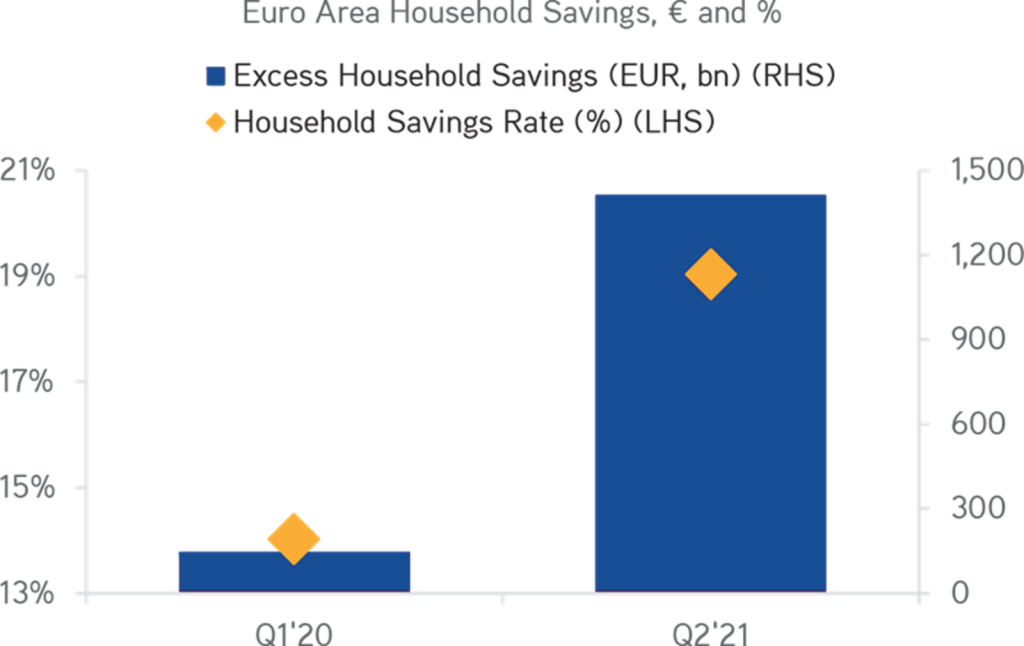

Our Expectation Is Continuation Of Household Consumption Due To Large Amounts Of Savings Accumulated During The Pandemic

Data as at August, 2021. Source: Statistical Office of the European Communities, European Central Bank, Haver Analytics.

6 We are taking sizable positions in Multiplicity & selling Simplicity. In our view, we believe portfolio managers will need to be more thematic about where an industry is headed. Can we buy down a multiple through tuck-in acquisitions; should we take the business in a new direction; and/or is this a good business but being run by a management team that lacks vision? We have argued that corporate carve-outs are amongst the most attractive ways to find devalued and underappreciated companies in bifurcated markets — markets that seem to eschew multiplicity in favor of simplicity at almost all costs.

From our point of view, we still think that the opportunity set to acquire high-quality carve-outs across PE, Infrastructure, and Energy remains outsized. Specifically for investors who are willing to take some small development, operational, and/or financing risks, there is the potential to earn outsized returns relative to when the story becomes more simplified in the public markets. Importantly, though, we are not advocating buying what appear to be ‘cheap’ assets in industries that face potential secular headwinds. Rather, we are advocating getting behind situations where active corporate management can unlock value that the public markets may be missing. We also see many opportunities where a slice of the capital structure just does not fit nicely into a specific allocation bucket for institutional investors (e.g., a complicated convertible bond, or a bond with equity warrants). As such, the incremental total return pick-up for investors who are willing to do additional work to understand the real opportunity set is really quite meaningful in both absolute and relative terms.

In this new era, we are shifting focus beyond just undervalued ‘diamonds in the rough‘ to include the occasional ’hidden gem‘ trading at a fraction of its intrinsic value.

Staying Invested: Our Favorites

At Zinqular our thematic framework increasingly drives our thinking around efficient capital deployment, monetization, and asset allocation. Consistent to our view, we want to tag what we Favor andwhat we Avoid that reflect our views as to where we believe portfolio managers and asset allocators should be leaning in and out. They are summarized below:

FAVOR> Portfolio Resilience. In 2022, we still choose Global Equities relative to sovereign debt. It certainly big appeal in this cycle for asset allocators. Across Global Equities, we favor a balanced exposure of Growth and Value (i.e., are long on general-purpose technologies, innovation, and multiplicity), and we are generally unaffected by size outside of equities disliked for e.g., large mega-cap tech and speculative growth names with no line of sight towards profitability.

We are overweight Europe, Japan, small- to mid-cap stocks in the U.S., and select Emerging Markets. These will be star performers in 2022. We are taking a double barrel approach to style selection, suggesting allocators construct portfolios with both Value and Growth at this point in the cycle.

FAVOR> We prefer higher-than-normal size of investments linked to pricing power and collateral-based cash flows. This is consistent with our focus on owning pricing power narratives during an era of rising inflation. Therefore, we suggest overweight positions in Infrastructure, Real Estate (e.g., Housing, Warehouses, etc.), and Asset-Based Finance.

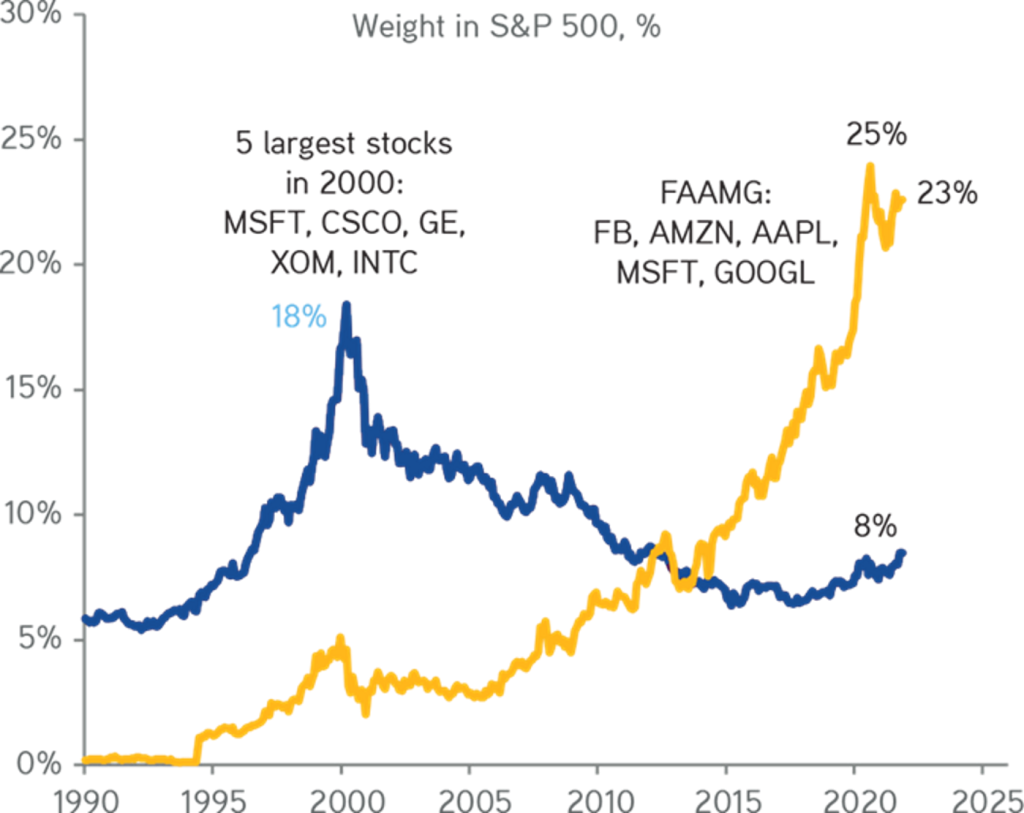

FAVOR> We are long on general-purpose technologies, innovation, particularly in the private markets. We continuously lean into general-purpose technologies cycle that has the potential to provide outsized returns to investors who can commit capital wisely behind mega-themes that are reshaping the global capital markets. Just consider that only 1.5% of the total companies in global stock markets over the last 30 years created 100% of the net wealth in stock market gains (Exhibit 3). Interestingly, many of the most promising companies are actually still private. Therefore, we suggest allocating some slug of capital to leaders in regulation technologies (Regtech), insurance technologies (Insuretech), blockchain, life sciences, payments, and software spaces.

FAVOR> Leaning into “quality but beaten down assets”. There is so much liquidity in the world, in a way that portfolio managers spend some time going where others are not. Currently, we see opportunities in Chinese technology companies, beaten-down conglomerates, Energy, European banks, UK Tech companies and China High Yield debt (USD). Not surprisingly, we also find public ‘break-up’ stories that are trading at attractive sum-of-the-parts multiples, or Real Estate/Infrastructure that is trading well below replacement costs as compelling investment opportunities to pursue.

FAVOR> Overweight Flexibility of Opportunistic Credit. In Liquid Credit, we choose Bank Loans to High Yield; which gives us the ability to switch across multiple asset classes as opportunities becomes available. In addition, we prefer structures in Credit where portfolio managers can lock in fixed rate liabilities and manage the asset side of the balance sheet to capture both higher rates and portfolio construction to enhance returns.

FAVOR> We are drawn to select Commodities; especially those that power energy transition themes e.g., aluminum, cobalt, copper, lithium, etc.. We still favor oil and gas at several spots on the forward curve. We also bullish on derivative plays connected to global energy transition and services linked to this business movement such as carbon capture technologies, and carbon credits.

FAVOR> We are drawn to Capital solutions. Providing customized capital solutions, e.g., convertible preferred shares or PIK/Equity structures, to private companies in innovation or general-purpose technology sectors appeals to us. Some early-stage companies are generating revenue which means investor(s) can move up in the capital structure at a time of lofty valuations and potentially still participate in some upside sharing if valuations hold and earnings come through. To our advantage, many traditional banks appear less interested in extending capital to these segments of the market and/or that large allocators may not have interest for this type of security.

AVOID| Companies with limited pricing power (i.e., Price takers). The market situation is going to lead to multiple and earnings de-ratings for firms that have high leverage levels and the inability to pass through costs, including labor. For instance, we think that consumer product companies with unhedged input costs will likely be miserable. The same narrative could play out for companies with large lower-wage workforces and limited pricing power, such as second-tier retailers and certain healthcare services. Our worry also plays out to companies that could have difficulty transferring higher input costs to a small and powerful base of buyers.

AVOID| Long Duration Bonds. This year we think higher inflation make the long-end of the curve particularly unattractive. As we show in Exhibit 56, the market has now priced in the risk of the Fed moving three times in 2022 (we concur). At the same time, the consensus is that the long-end of the curve will be essentially flat 10-years from now on a forward basis (Exhibit 97). We think that the forecast for the long-end is too pessimistic. We also note that when the taper tantrum occurred, by comparison, the market was pricing a 10-year forward of more than four percent.

AVOID| Popular stocks & Big cap technology stocks with super rich valuations. In connection with strategy, we still see many of the most popular growth stocks, including some of the unprofitable momentum ones, not doing as well. The law of large numbers, increased regulatory scrutiny (anti-trust, data, etc.), and higher multiples in certain instances could all soon begin to act as potential headwinds. We think, tightening financial conditions too should bring scrutiny to some of the unprofitable, momentum names in 2022.

AVOID| Select EM Currencies. Headwinds such as COVID variants, investor sentiment, huge deficits, elections and rising inflation could make certain EM currencies particularly vulnerable as global tightening starts and may end ahead of schedule. For the fourth year in a row, we continue to think that Turkey represents an unwelcome macro destination for capital. The country’s policies are out of step with the global reflation theme we see unfolding. As a result, we think that both the currency and the stock market will continue to struggle. On Mexico, we are increasingly unsettled by recent administration moves, including its relationship with the central bank.

Exhibit 23:

The 5 Largest Stocks In 2000 Vs 2020 Now 8% Of S&P 500; Keeping Equity Market Leadership Is Difficult

Data as at November 12, 2021. Source: Goldman Sachs Global Investment Research.

Exhibit 24:

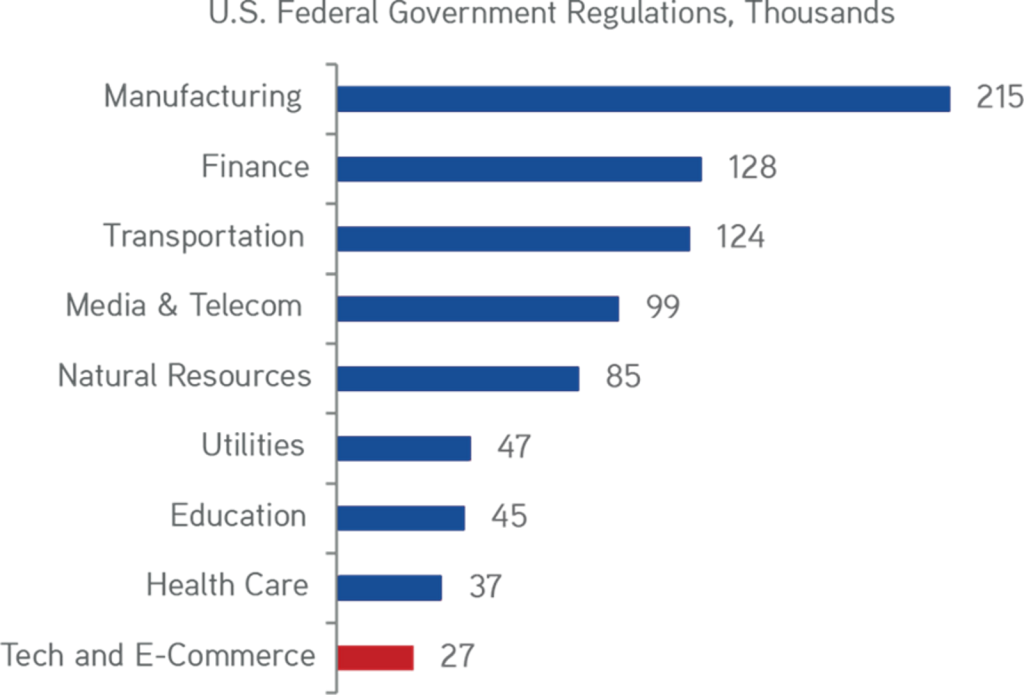

Technology Still One Of Least Regulated Industries, Albeit Monopolistic. We Believe This Reality May Change Soon

Data as at April 2018. Source: BofAML.

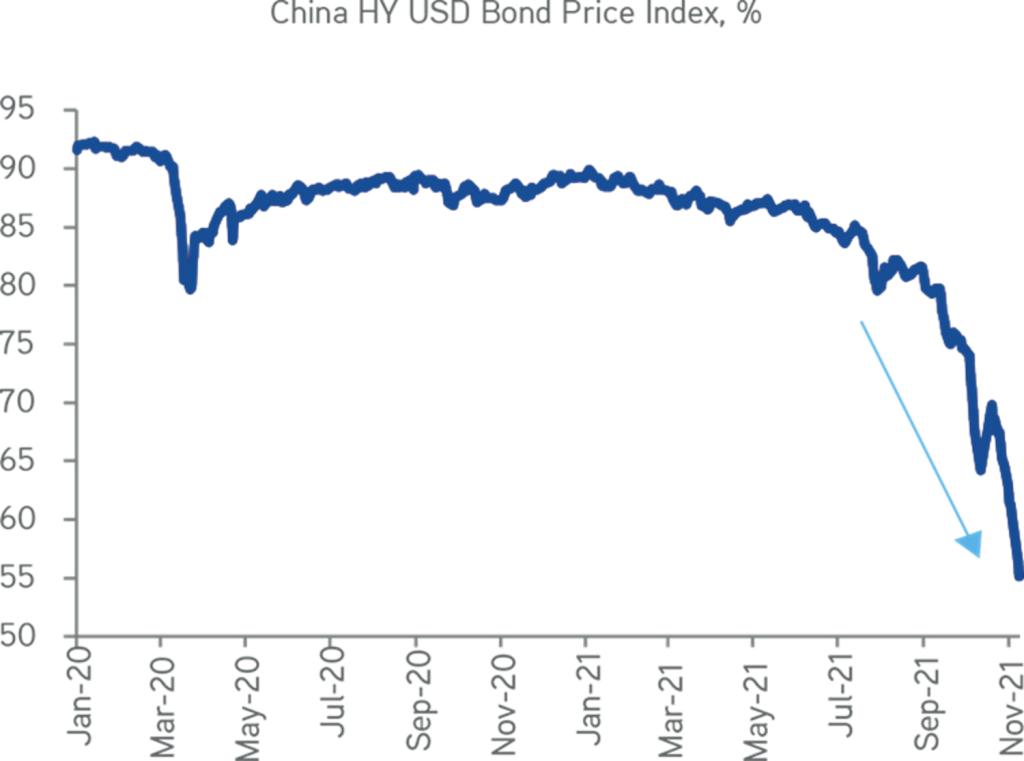

Exhibit 25:

We Think China Distressed High Yield Could be Good Investment Opportunity

Data as at December, 2021. Source. Bloomberg.

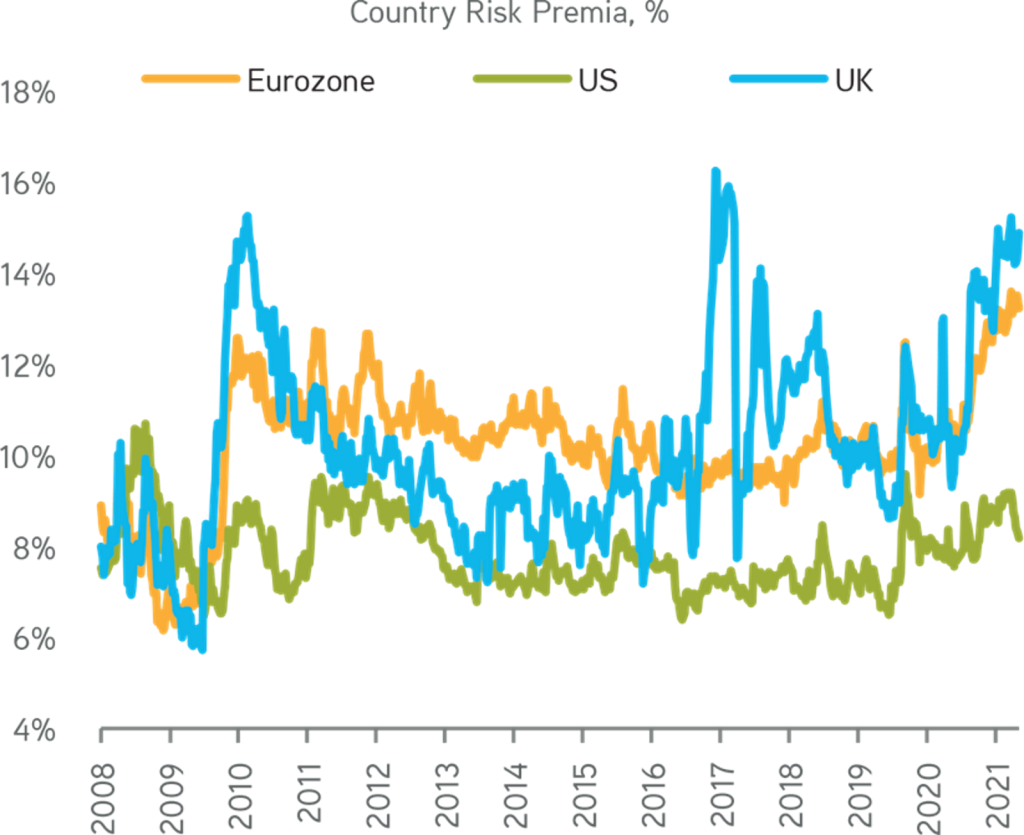

Exhibit 26:

The Eurozone Risk Premia Looks Higher Compared to the US

Note: Europe is the average of Eurozone and the UK. Data as at November, 2021. Source: Bloomberg.

Regarding what keep us worried, we have our attention on the possibility of emergence of new COVID variants. Our view is this is still a global health concern. We think the excess stimulus and rapidly evolving positive science will keep recent mutations from permanently causing havoc to the economic recovery.

Next, our list of worry really involves the interplay between interest rates and financial conditions. What should portfolio managers focus on? Without a doubt, there is now a greater risk of faster than expected tightening of financial conditions in 2022. The financial tightening scenario means growth would slow more than anticipated. In addition, though nominal rates might actually not move much from current levels, real rates would increase as future inflation expectations nose dive. This would lead to a broad-based and rapid tightening of global financial conditions. Thereby making it bearish for most risk assets scenarios.

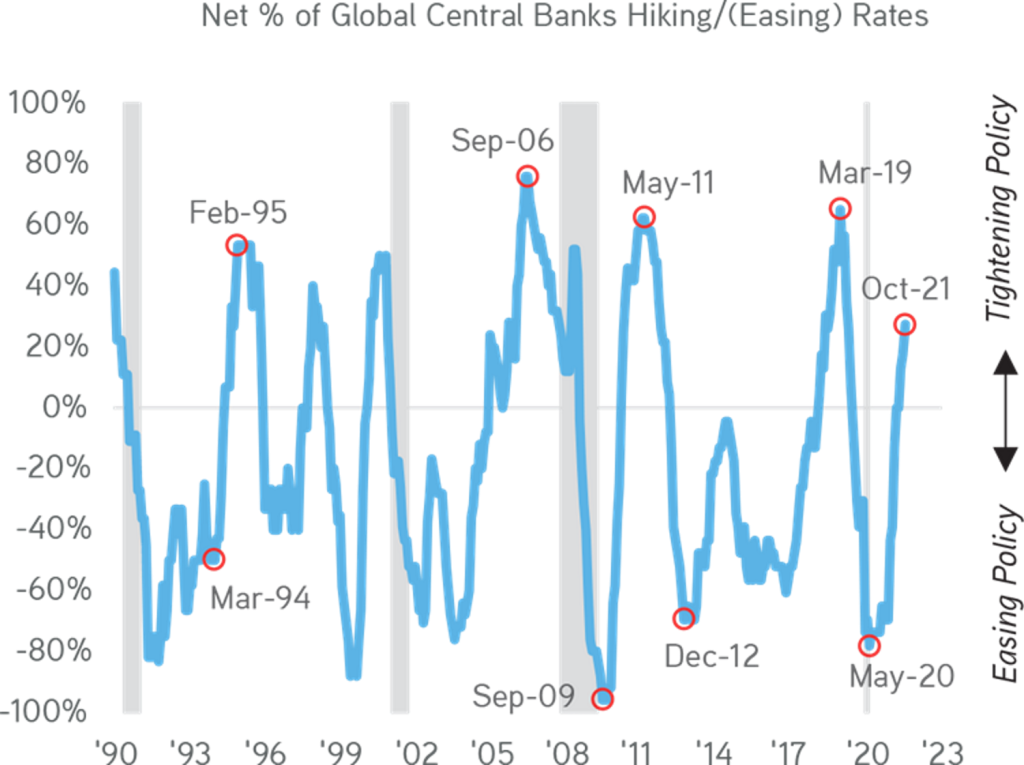

Exhibit 27:

Financial Situations Will Tighten In A Mid-Cycle Scenario

Data as at November 3, 2021. Source: Respective Central Banks, Haver Analytics.

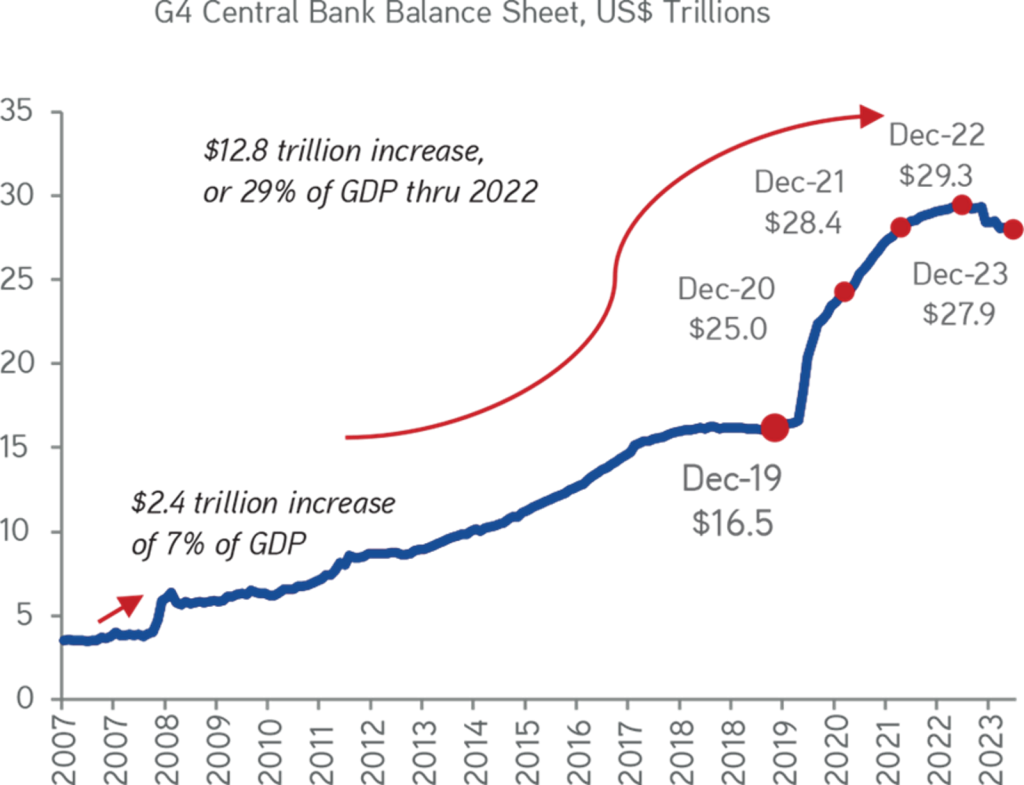

Exhibit 28:

Liquidity In The Economy Will Offset The Reversal In Flow Of Our 2022 Forecast

Data as at November 15, 2021. Source: Fed, Bloomberg, Morgan Stanley estimates.

Another scenario (though unlikely) is that nominal yields could rise sharply, at the same time real yields do not move up at all. In this scenario, investors would have lost confidence in the central banks’ ability to control inflation. If this occurs, both Equities and Bonds would de-rate significantly up in value, with Commodities being the relative beneficiary.

We enter 2022 with a generally positive view of the world. Sure, we expect a lot more volatility in 2022, as both the recovery and central bank policies are not in sync across the various regions where Zinqular does business. Also, the pandemic is not over; it just continues to reinvent itself. Therefore, in 2022 we think that there is over 50% possibility that we are tradeable 12% plus correction.

Therefore, we are still pro-risk in our asset allocation grounded on the following assumption: This year financial conditions may not stricter and tighter enough to permanently neutralize the huge size of absolute liquidity that is still in the economy (Exhibit 28). In addition, real rates outside of China is still quite low in absolute terms that any tightening start from stupendously low base relative to the past (Exhibit 7).

Let say if central banks start to taper more quickly (suggesting record fall of COVID cases in early 2022), the balance sheets of the G4, for instance, are already in excess of $12 trillion versus its peak last cycle – and you may recall it took four years before the Fed’s balance sheet began to shrink after it announced tapering. China may ease in H1/2022. We also think the ECB will be more accommodative for longer.